Answered step by step

Verified Expert Solution

Question

1 Approved Answer

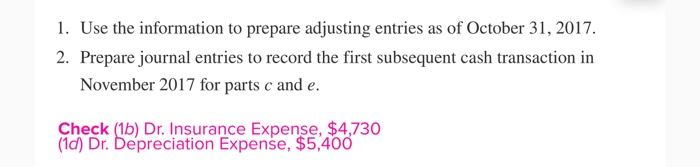

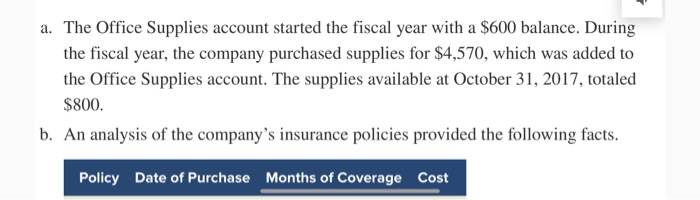

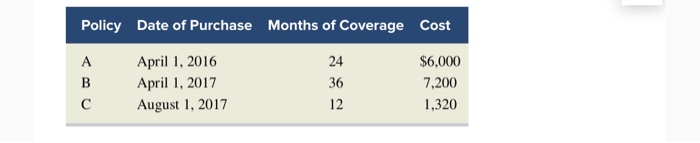

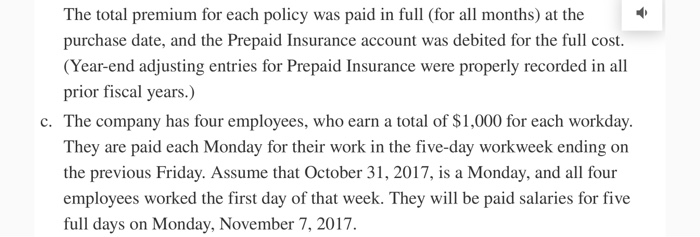

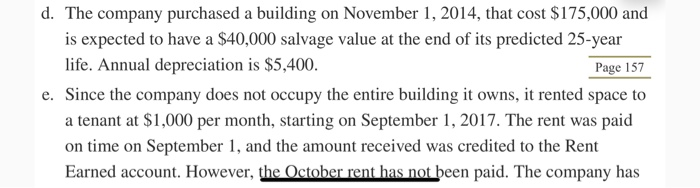

1. Use the information to prepare adjusting entries as of October 31, 2017. 2. Prepare journal entries to record the first subsequent cash transaction in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Towards A Strategic Human Resource Management Roles Of HR Audit And Org Culture

Authors: Adel Al Samman

1st Edition

3330653051, 978-3330653054