Answered step by step

Verified Expert Solution

Question

1 Approved Answer

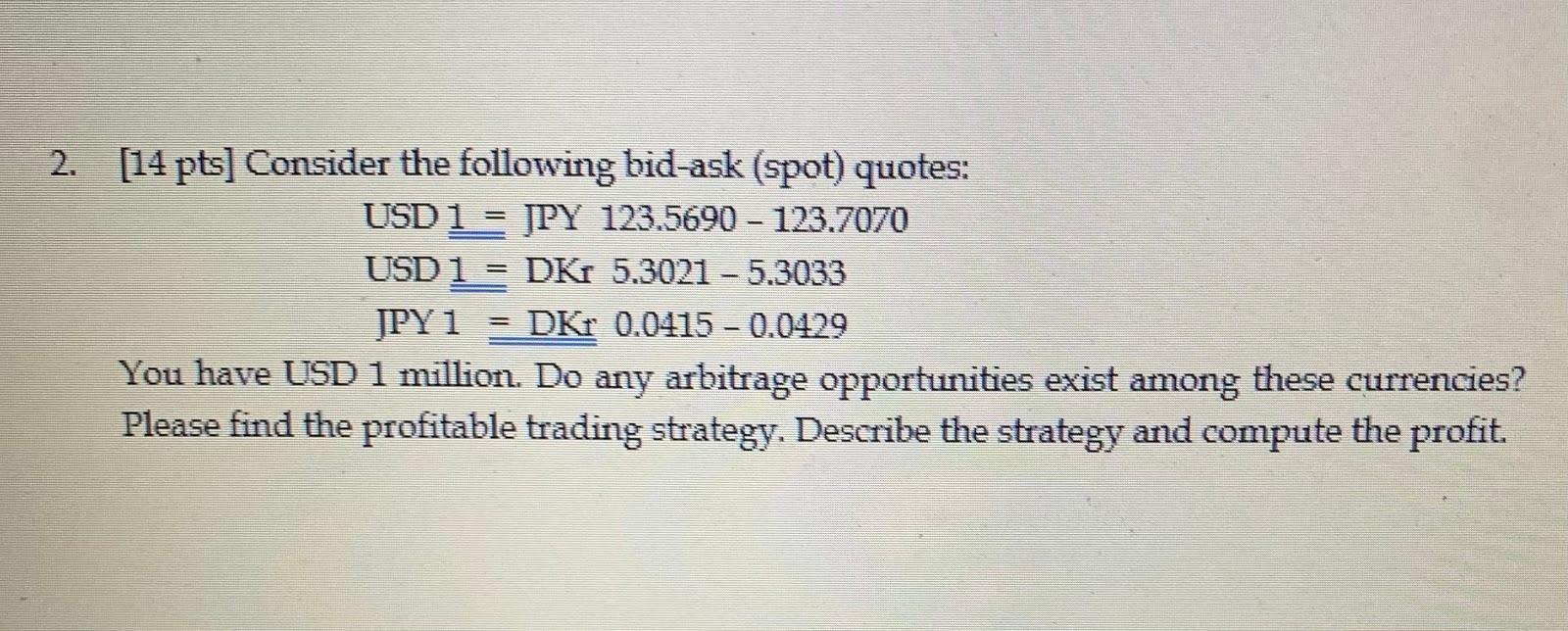

2. [14 pts] Consider the following bid-ask (spot) quotes: USD 1 = JPY 123.5690 123.7070 USD1 = DK 5.3021 - 5.3033 JPY 1 DK 0.0415

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Unlocking The Door To Real Estate Success Achieving Passive Income

Authors: Benjamin Stone

1st Edition

979-8856252278