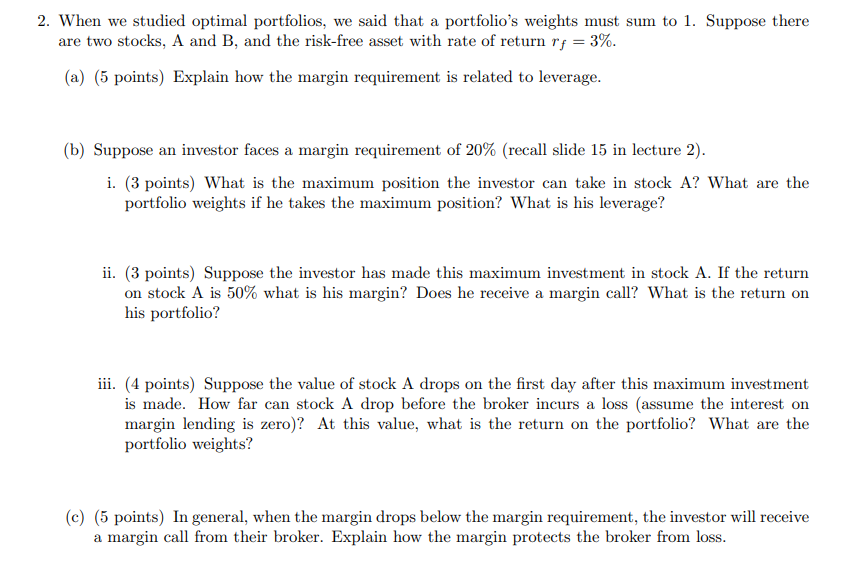

2. When we studied optimal portfolios, we said that a portfolio's weights must sum to 1. Suppose there are two stocks, A and B, and the risk-free asset with rate of return ry = 3%. (a) (5 points) Explain how the margin requirement is related to leverage. (b) Suppose an investor faces a margin requirement of 20% (recall slide 15 in lecture 2). i. (3 points) What is the maximum position the investor can take in stock A? What are the portfolio weights if he takes the maximum position? What is his leverage? ii. (3 points) Suppose the investor has made this maximum investment in stock A. If the return on stock A is 50% what is his margin? Does he receive a margin call? What is the return on his portfolio? iii. (4 points) Suppose the value of stock A drops on the first day after this maximum investment is made. How far can stock A drop before the broker incurs a loss (assume the interest on margin lending is zero)? At this value, what is the return on the portfolio? What are the portfolio weights? (c) (5 points) In general, when the margin drops below the margin requirement, the investor will receive a margin call from their broker. Explain how the margin protects the broker from loss. 2. When we studied optimal portfolios, we said that a portfolio's weights must sum to 1. Suppose there are two stocks, A and B, and the risk-free asset with rate of return ry = 3%. (a) (5 points) Explain how the margin requirement is related to leverage. (b) Suppose an investor faces a margin requirement of 20% (recall slide 15 in lecture 2). i. (3 points) What is the maximum position the investor can take in stock A? What are the portfolio weights if he takes the maximum position? What is his leverage? ii. (3 points) Suppose the investor has made this maximum investment in stock A. If the return on stock A is 50% what is his margin? Does he receive a margin call? What is the return on his portfolio? iii. (4 points) Suppose the value of stock A drops on the first day after this maximum investment is made. How far can stock A drop before the broker incurs a loss (assume the interest on margin lending is zero)? At this value, what is the return on the portfolio? What are the portfolio weights? (c) (5 points) In general, when the margin drops below the margin requirement, the investor will receive a margin call from their broker. Explain how the margin protects the broker from loss