Answered step by step

Verified Expert Solution

Question

1 Approved Answer

3. Consider the following data: Expected Return Standard Deviation Russell Fund Windsor Fund S&P Fund 16% 14% 12% 12% 10% 8% The correlation between

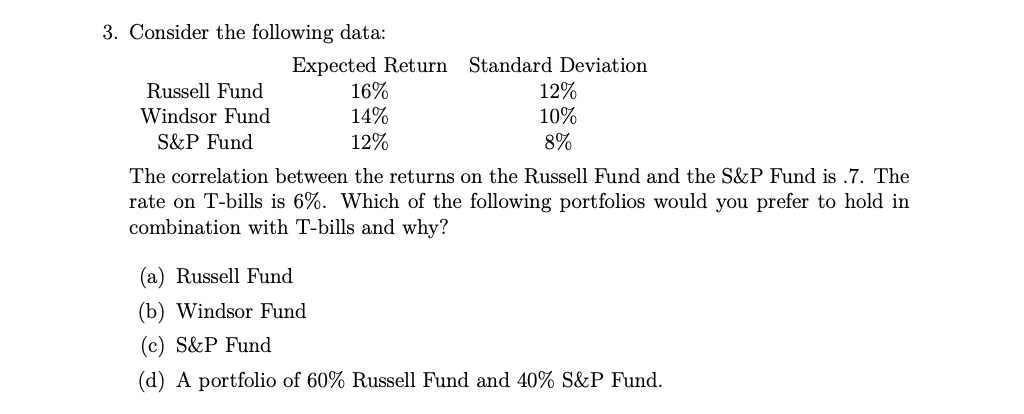

3. Consider the following data: Expected Return Standard Deviation Russell Fund Windsor Fund S&P Fund 16% 14% 12% 12% 10% 8% The correlation between the returns on the Russell Fund and the S&P Fund is .7. The rate on T-bills is 6%. Which of the following portfolios would you prefer to hold in combination with T-bills and why? (a) Russell Fund (b) Windsor Fund (c) S&P Fund (d) A portfolio of 60% Russell Fund and 40% S&P Fund.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To determine which portfolio to hold in combination with Tbills we compare the Sharpe Ratios The Sha...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Finance The Logic and Practice of Financial Management

Authors: Arthur J. Keown, John D. Martin, J. William Petty

8th edition

132994879, 978-0132994873