Answered step by step

Verified Expert Solution

Question

1 Approved Answer

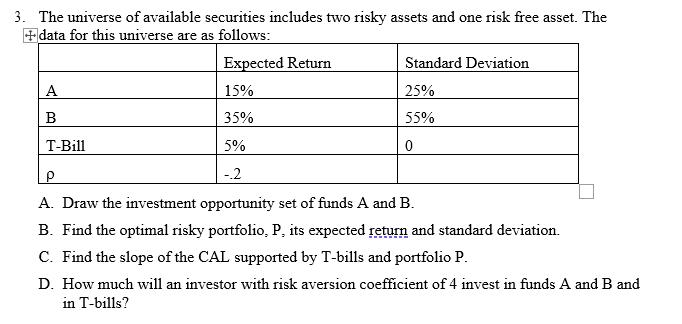

3. The universe of available securities includes two risky assets and one risk free asset. The +data for this universe are as follows: A

3. The universe of available securities includes two risky assets and one risk free asset. The +data for this universe are as follows: A B T-Bill P Expected Return Standard Deviation 15% 25% 35% 55% 5% 0 -.2 A. Draw the investment opportunity set of funds A and B. B. Find the optimal risky portfolio, P, its expected return and standard deviation. C. Find the slope of the CAL supported by T-bills and portfolio P. D. How much will an investor with risk aversion coefficient of 4 invest in funds A and B and in T-bills?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISE Investments

Authors: Zvi Bodie, Alex Kane, Alan Marcus

12th International Edition

1260571157, 978-1260571158