Answered step by step

Verified Expert Solution

Question

1 Approved Answer

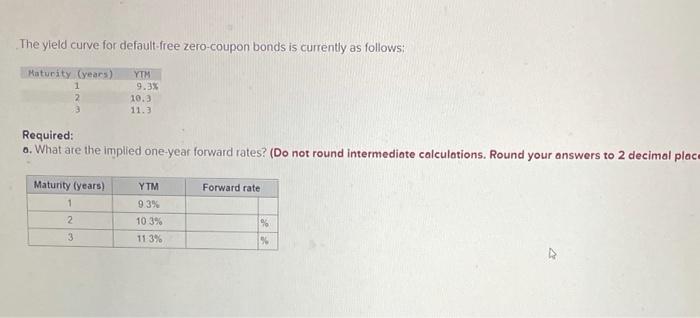

4 please help The yleld curve for default-free zero-coupon bonds is currently as follows: Required: 0. What are the implied one-year forward rates? (Do not

4 please help

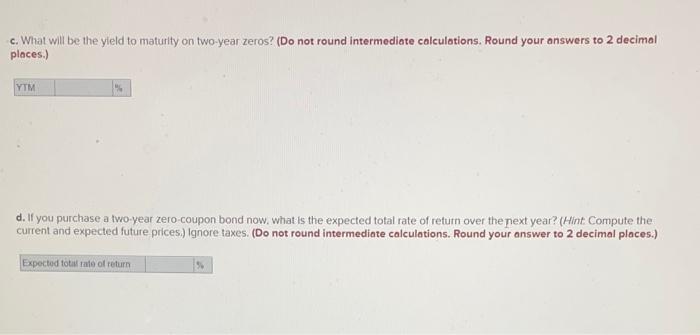

The yleld curve for default-free zero-coupon bonds is currently as follows: Required: 0. What are the implied one-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal pla c. What will be the yleld to maturity on two-year zeros? (Do not round intermediate calculations. Round your answers to 2 decimal places.) d. If you purchase a two-year zero-coupon bond now, what is the expected total rate of return over the next year? ( H int. Compute the current and expected future prices.) Ignore taxes. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Urban Public Finance

Authors: D. Wildasin

1st Edition

0415851882, 978-0415851886