Answered step by step

Verified Expert Solution

Question

1 Approved Answer

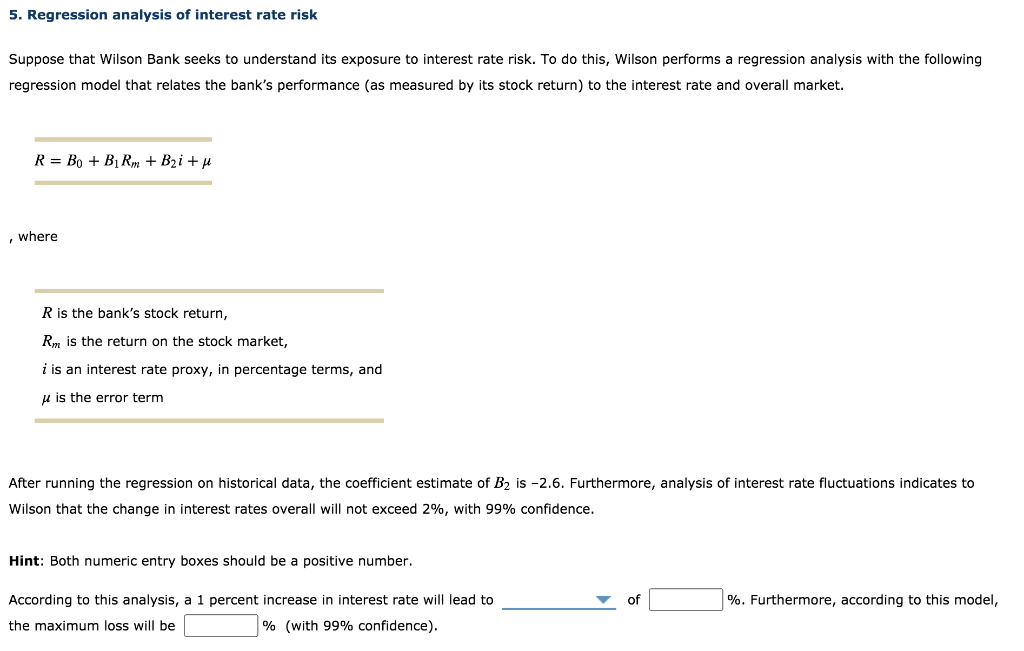

5. Regression analysis of interest rate risk Suppose that Wilson Bank seeks to understand its exposure to interest rate risk. To do this, Wilson performs

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money Talks Explaining How Money Really Works

Authors: Nina Bandelj ,Frederick F. Wherry ,Viviana A. Zelizer

1st Edition

0691202893, 978-0691202891