Answered step by step

Verified Expert Solution

Question

1 Approved Answer

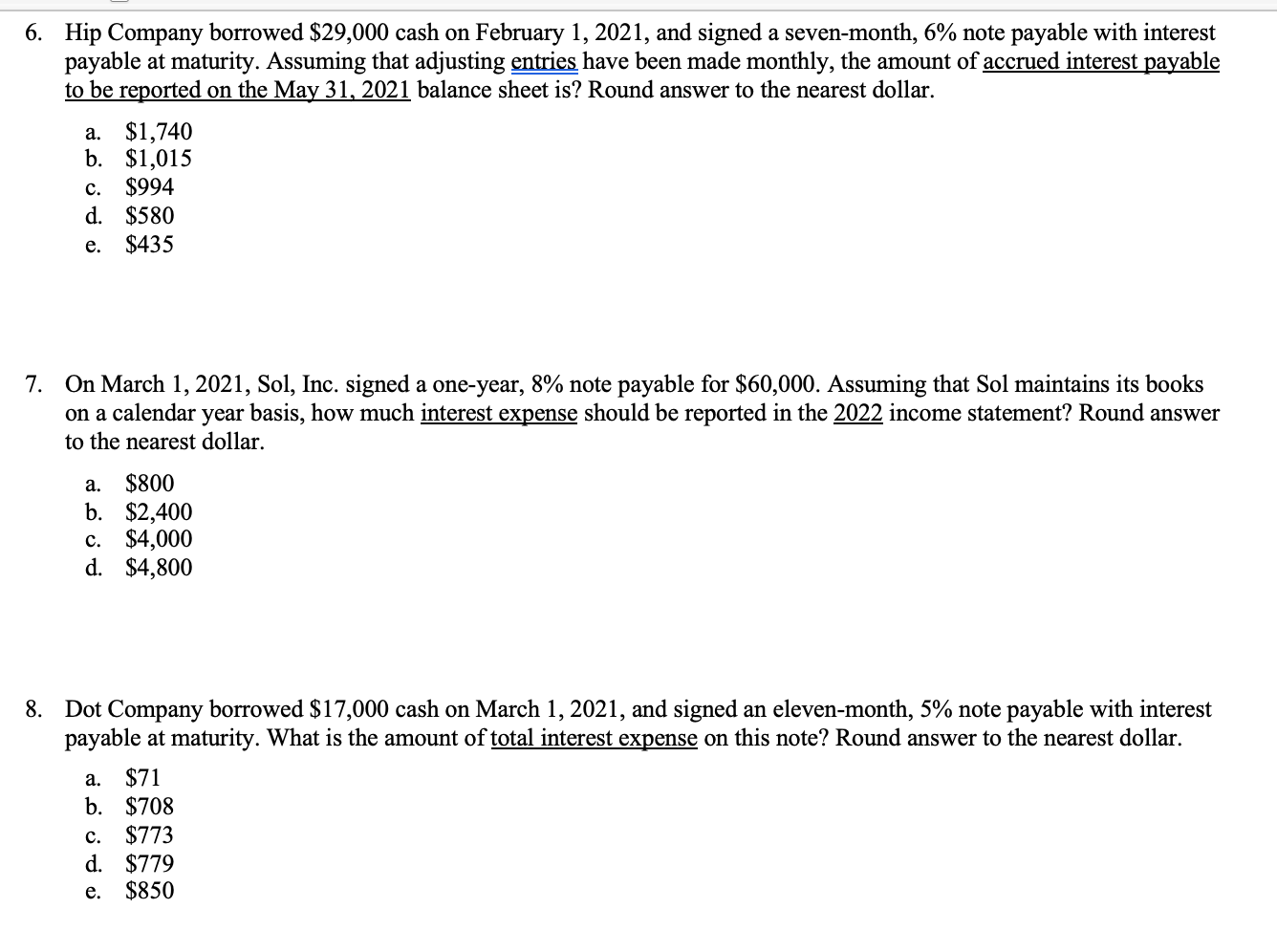

6. Hip Company borrowed $29,000 cash on February 1, 2021, and signed a seven-month, 6% note payable with interest payable at maturity. Assuming that adjusting

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Law And Order Review 1993 An Audit Of Crime Policing And Criminal Justice Issues

Authors: John Benyon

1st Edition

1874493901, 978-1874493907