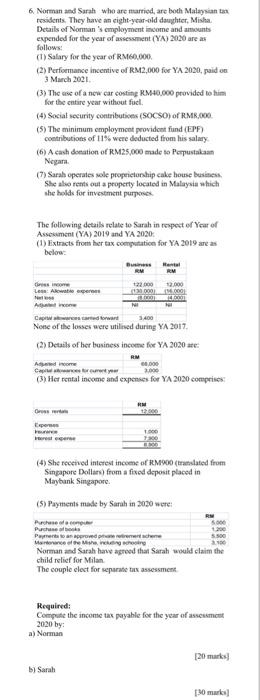

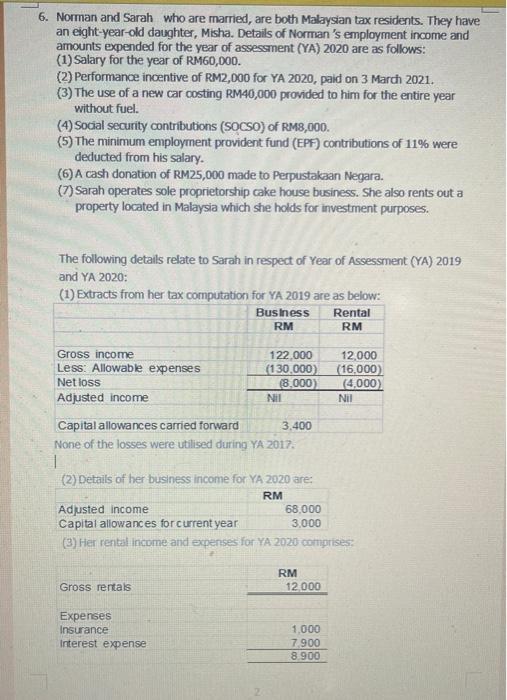

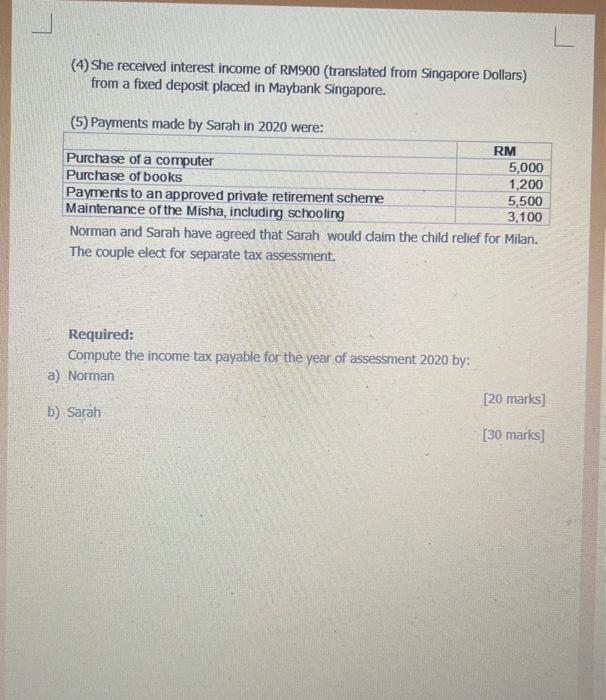

6 Norman and Sarah who are married are both Malaysian residents. They have an eight-year-old daughter, Misha Details of Norman's employment income and amounts expended for the year of assessment (YA) 2020 areas follows: (1) Salary for the year of RM60,000 (2) Performance incentive of RM2,000 for YA 2030 paid on 3 March 2001 (3) The use of a new car costing RM40.000 provided to him for the entire year without fuel (4) Social security contributions (SOCSO) of RMR.000 (5) The minimum employment provident fund (EPF) contributions of 11% were deducted from his salary (6) A cash donation of RM25,000 made to Perpustakaan Negara . (7) Sarah operates sole proprietorship cake house business She also rents out a property located in Malaysia which she holds for investment purposes The following details relate to Sarah in respect of Year of Assessment (YA) 2019 and YA 2020 (1) Extracts from her tax computation for YA 2019 areas below B Harta RM 122.000 2.000 L: Alert (0.00 A NI Capww.cated and None of the losses were utilised during YA 2017, 3.400 (2) Details of her business income for YA 2020 se: Am 60.00 2.000 Capwerew (5) Her rental income and expenses for YA 2020 comprises Orere pers rester (4) She received interest income of RM900 (translated from Singapore Dollars) from a fixed deposit placed in Maybank Singapore (5) Payments made by Sarah in 2030 were Pucho Purrento an appropriatermeer March Norman and Sarah have agreed that Sarah would claim the The couple clect for separate tax assessment child relief for Milan Required: Compute the income tax payable for they 2020 by he year of women a) Norman 20 marks) by Sarah [30 mars 6. Norman and Sarah who are married, are both Malaysian tax residents. They have an eight-year-old daughter, Misha. Details of Norman's employment income and amounts expended for the year of assessment (YA) 2020 are as follows: (1) Salary for the year of RM60,000. (2) Performance incentive of RM2,000 for YA 2020, paid on 3 March 2021. (3) The use of a new car costing RM40,000 provided to him for the entire year without fuel. (4) Social security contributions (SOCSO) of RM8,000. (5) The minimum employment provident fund (EPF) contributions of 11% were deducted from his salary. (6) A cash donation of RM25,000 made to Perpustakaan Negara. (7) Sarah operates sole proprietorship cake house business. She also rents out a property located in Malaysia which she holds for investment purposes. The following details relate to Sarah in respect of Year of Assessment (YA) 2019 and YA 2020: (1) Extracts from her tax computation for YA 2019 are as below: Business Rental RM RM Gross income Less: Allowable expenses Net loss Adjusted income 122.000 (130.000) (8.000) NII 12,000 (16,000) (4,000) NII Capital allowances carried forward 3.400 None of the losses were utilised during YA 2017. (2) Details of her business income for YA 2020 are: Adjusted income Capital allowances for current year (3) Her rental income and expenses for YA 2020 comprises: RM 68.000 3000 RM 12000 Gross rentals Expenses Insurance Interest expense 1.000 7.900 8.900 L (4) She received interest income of RM900 (translated from Singapore Dollars) from a fixed deposit placed in Maybank Singapore. (5) Payments made by Sarah in 2020 were: RM Purchase of a computer 5,000 Purchase of books 1,200 Payments to an approved private retirement scheme 5,500 Maintenance of the Misha, including schooling 3.100 Norman and Sarah have agreed that Sarah would daim the child relief for Milan. The couple elect for separate tax assessment. Required: Compute the income tax payable for the year of assessment 2020 by: a) Norman [20 marks] b) Sarah [30 marks] 6 Norman and Sarah who are married are both Malaysian residents. They have an eight-year-old daughter, Misha Details of Norman's employment income and amounts expended for the year of assessment (YA) 2020 areas follows: (1) Salary for the year of RM60,000 (2) Performance incentive of RM2,000 for YA 2030 paid on 3 March 2001 (3) The use of a new car costing RM40.000 provided to him for the entire year without fuel (4) Social security contributions (SOCSO) of RMR.000 (5) The minimum employment provident fund (EPF) contributions of 11% were deducted from his salary (6) A cash donation of RM25,000 made to Perpustakaan Negara . (7) Sarah operates sole proprietorship cake house business She also rents out a property located in Malaysia which she holds for investment purposes The following details relate to Sarah in respect of Year of Assessment (YA) 2019 and YA 2020 (1) Extracts from her tax computation for YA 2019 areas below B Harta RM 122.000 2.000 L: Alert (0.00 A NI Capww.cated and None of the losses were utilised during YA 2017, 3.400 (2) Details of her business income for YA 2020 se: Am 60.00 2.000 Capwerew (5) Her rental income and expenses for YA 2020 comprises Orere pers rester (4) She received interest income of RM900 (translated from Singapore Dollars) from a fixed deposit placed in Maybank Singapore (5) Payments made by Sarah in 2030 were Pucho Purrento an appropriatermeer March Norman and Sarah have agreed that Sarah would claim the The couple clect for separate tax assessment child relief for Milan Required: Compute the income tax payable for they 2020 by he year of women a) Norman 20 marks) by Sarah [30 mars 6. Norman and Sarah who are married, are both Malaysian tax residents. They have an eight-year-old daughter, Misha. Details of Norman's employment income and amounts expended for the year of assessment (YA) 2020 are as follows: (1) Salary for the year of RM60,000. (2) Performance incentive of RM2,000 for YA 2020, paid on 3 March 2021. (3) The use of a new car costing RM40,000 provided to him for the entire year without fuel. (4) Social security contributions (SOCSO) of RM8,000. (5) The minimum employment provident fund (EPF) contributions of 11% were deducted from his salary. (6) A cash donation of RM25,000 made to Perpustakaan Negara. (7) Sarah operates sole proprietorship cake house business. She also rents out a property located in Malaysia which she holds for investment purposes. The following details relate to Sarah in respect of Year of Assessment (YA) 2019 and YA 2020: (1) Extracts from her tax computation for YA 2019 are as below: Business Rental RM RM Gross income Less: Allowable expenses Net loss Adjusted income 122.000 (130.000) (8.000) NII 12,000 (16,000) (4,000) NII Capital allowances carried forward 3.400 None of the losses were utilised during YA 2017. (2) Details of her business income for YA 2020 are: Adjusted income Capital allowances for current year (3) Her rental income and expenses for YA 2020 comprises: RM 68.000 3000 RM 12000 Gross rentals Expenses Insurance Interest expense 1.000 7.900 8.900 L (4) She received interest income of RM900 (translated from Singapore Dollars) from a fixed deposit placed in Maybank Singapore. (5) Payments made by Sarah in 2020 were: RM Purchase of a computer 5,000 Purchase of books 1,200 Payments to an approved private retirement scheme 5,500 Maintenance of the Misha, including schooling 3.100 Norman and Sarah have agreed that Sarah would daim the child relief for Milan. The couple elect for separate tax assessment. Required: Compute the income tax payable for the year of assessment 2020 by: a) Norman [20 marks] b) Sarah [30 marks]