Answered step by step

Verified Expert Solution

Question

1 Approved Answer

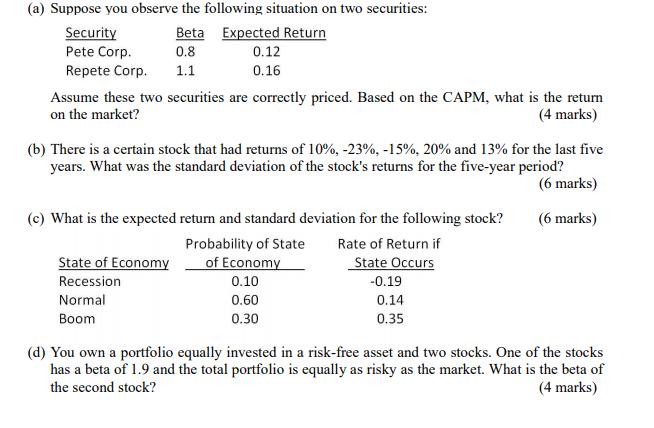

(a) Suppose you observe the following situation on two securities: Security Pete Corp. Beta 0.8 Repete Corp. 1.1 Expected Return 0.12 0.16 Assume these

(a) Suppose you observe the following situation on two securities: Security Pete Corp. Beta 0.8 Repete Corp. 1.1 Expected Return 0.12 0.16 Assume these two securities are correctly priced. Based on the CAPM, what is the return on the market? (4 marks) (b) There is a certain stock that had returns of 10%, -23%, -15%, 20% and 13% for the last five years. What was the standard deviation of the stock's returns for the five-year period? (6 marks) (c) What is the expected return and standard deviation for the following stock? (6 marks) Probability of State Rate of Return if State of Economy Recession of Economy State Occurs 0.10 Normal 0.60 Boom 0.30 -0.19 0.14 0.35 (d) You own a portfolio equally invested in a risk-free asset and two stocks. One of the stocks has a beta of 1.9 and the total portfolio is equally as risky as the market. What is the beta of the second stock? (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance Core Principles and Applications

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe, Bradford Jordan

5th edition

1259289907, 978-1259289903