Question

Account 12/31/2014 Balance (projected) 12/31/2013 Balance (audited) 12/31/2012 Balance (audited) Sales $ 25,354,128 $ 22,122,039 $ 23,346,943 Total Assets $ 19,885,320 $ 17,336,809 $ 18,204,143

| Account | 12/31/2014 Balance (projected) | 12/31/2013 Balance (audited) | 12/31/2012 Balance (audited) |

| Sales | $ 25,354,128 | $ 22,122,039 | $ 23,346,943 |

| Total Assets | $ 19,885,320 | $ 17,336,809 | $ 18,204,143 |

| Gross Profit | $ 12,409,357 | $ 10,819,457 | $ 11,236,851 |

| Pre-Tax Income | $ 6,423,040 | $ 5,615,674 | $ 5,881,853 |

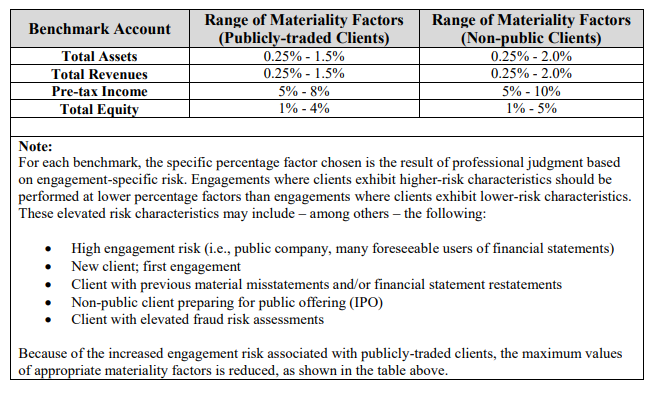

Upon determining the appropriate benchmark, the auditor considers the percentage to apply to that benchmark. The percentage is, in part, based on the benchmark that is chosen. For example, the percentage used if total assets is chosen as the benchmark will be smaller than the percentage used if the auditor chooses pretax income. It is expected that between 5% and 10% will be the percentage applied to a pretax income benchmark. However, when the client is publicly traded, the suggested percentage is 5%. When either total assets or total revenues is selected as the benchmark, the percentage applied should be between 0.25% and 2%. A percentage between 1% and 5% is acceptable when total equity is selected as the benchmark. Within these percentage ranges, the percentage applied depends in part on the riskiness of the clients financial reporting, with higher percentages being applied when lower risk exists and lower percentages applied when higher risk exists

Question:

Which would you pick as benchmark, and why? What is the benchmark percentage?

Benchmark Account Total Assets Total Revenues Pre-tax Income Total Equity Range of Materiality Factors (Publicly-traded Clients) 0.25% - 1.5% 0.25% - 1.5% 5%-8% 1% -4% Range of Materiality Factors (Non-public Clients) 0.25% - 2.0% 0.25% - 2.0% 5% - 10% 1% - 5% Note: For each benchmark, the specific percentage factor chosen is the result of professional judgment based on engagement-specific risk. Engagements where clients exhibit higher-risk characteristics should be performed at lower percentage factors than engagements where clients exhibit lower-risk characteristics. These elevated risk characteristics may include - among others the following: High engagement risk (i.e., public company, many foreseeable users of financial statements) New client; first engagement Client with previous material misstatements and/or financial statement restatements Non-public client preparing for public offering (IPO) Client with elevated fraud risk assessments Because of the increased engagement risk associated with publicly-traded clients, the maximum values of appropriate materiality factors is reduced, as shown in the table aboveStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Secure And Audit Oracle 10g And 11g

Authors: Ron Ben-Natan, Brian E. White, Paul R. Garvey

1st Edition

1420084127, 978-1420084122