Answered step by step

Verified Expert Solution

Question

1 Approved Answer

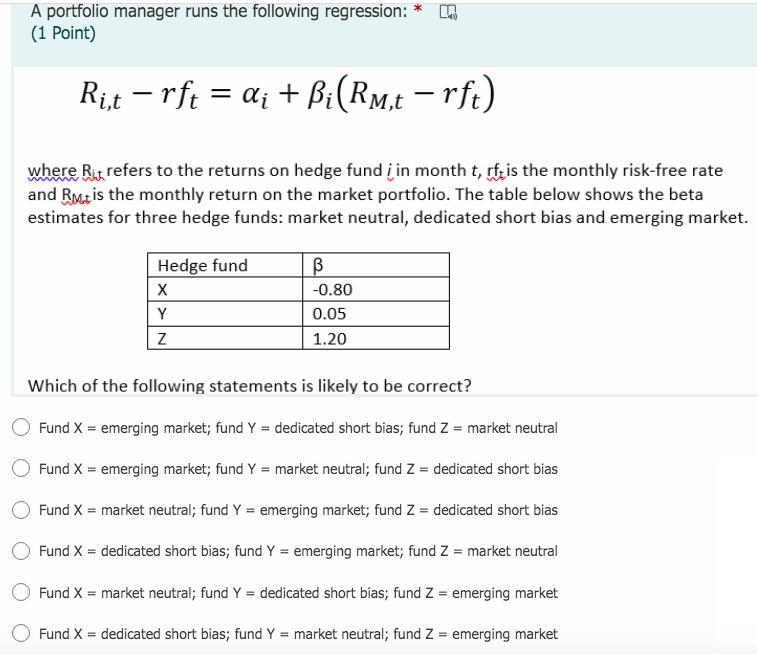

A portfolio manager runs the following regression: (1 Point) Ri,t = rft = i + Bi(Rm,t rft) * where Rit refers to the returns

A portfolio manager runs the following regression: (1 Point) Ri,t = rft = i + Bi(Rm,t rft) * where Rit refers to the returns on hedge fund i in month t, rf is the monthly risk-free rate and Rt is the monthly return on the market portfolio. The table below shows the beta estimates for three hedge funds: market neutral, dedicated short bias and emerging market. Hedge fund X Y Z -0.80 0.05 1.20 Which of the following statements is likely to be correct? Fund X = emerging market; fund Y = dedicated short bias; fund Z = market neutral Fund X = emerging market; fund Y = market neutral; fund Z = dedicated short bias Fund X = market neutral; fund Y = emerging market; fund Z = dedicated short bias Fund X = dedicated short bias; fund Y = emerging market; fund Z = market neutral Fund X = market neutral; fund Y = dedicated short bias; fund Z= emerging market Fund X = dedicated short bias; fund Y = market neutral; fund Z = emerging market

Step by Step Solution

★★★★★

3.43 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

Answer If beta is positive but very low the hedge fund is known as market neutral fu...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703