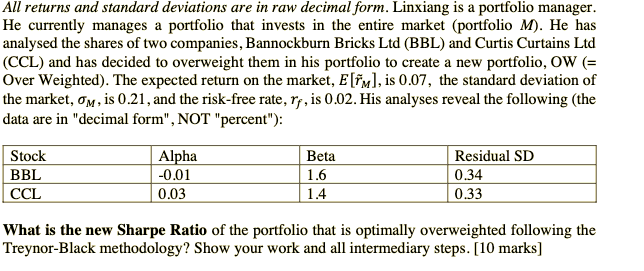

All returns and standard deviations are in raw decimal form. Linxiang is a portfolio manager. He currently manages a portfolio that invests in the

All returns and standard deviations are in raw decimal form. Linxiang is a portfolio manager. He currently manages a portfolio that invests in the entire market (portfolio M). He has analysed the shares of two companies, Bannockburn Bricks Ltd (BBL) and Curtis Curtains Ltd (CCL) and has decided to overweight them in his portfolio to create a new portfolio, OW (= Over Weighted). The expected return on the market, E[FM], is 0.07, the standard deviation of the market, M, is 0.21, and the risk-free rate, ry, is 0.02. His analyses reveal the following (the data are in "decimal form", NOT "percent"): Stock BBL CCL Alpha -0.01 0.03 Beta 1.6 1.4 Residual SD 0.34 0.33 What is the new Sharpe Ratio of the portfolio that is optimally overweighted following the Treynor-Black methodology? Show your work and all intermediary steps. [10 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To calculate the new Sharpe Ratio of the portfolio that is optimally overweighted following the TreynorBlack methodology we need to go through the fol...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Lawrence J. Gitman, Chad J. Zutter

13th Edition

9780132738729, 136119468, 132738724, 978-0136119463