Answered step by step

Verified Expert Solution

Question

1 Approved Answer

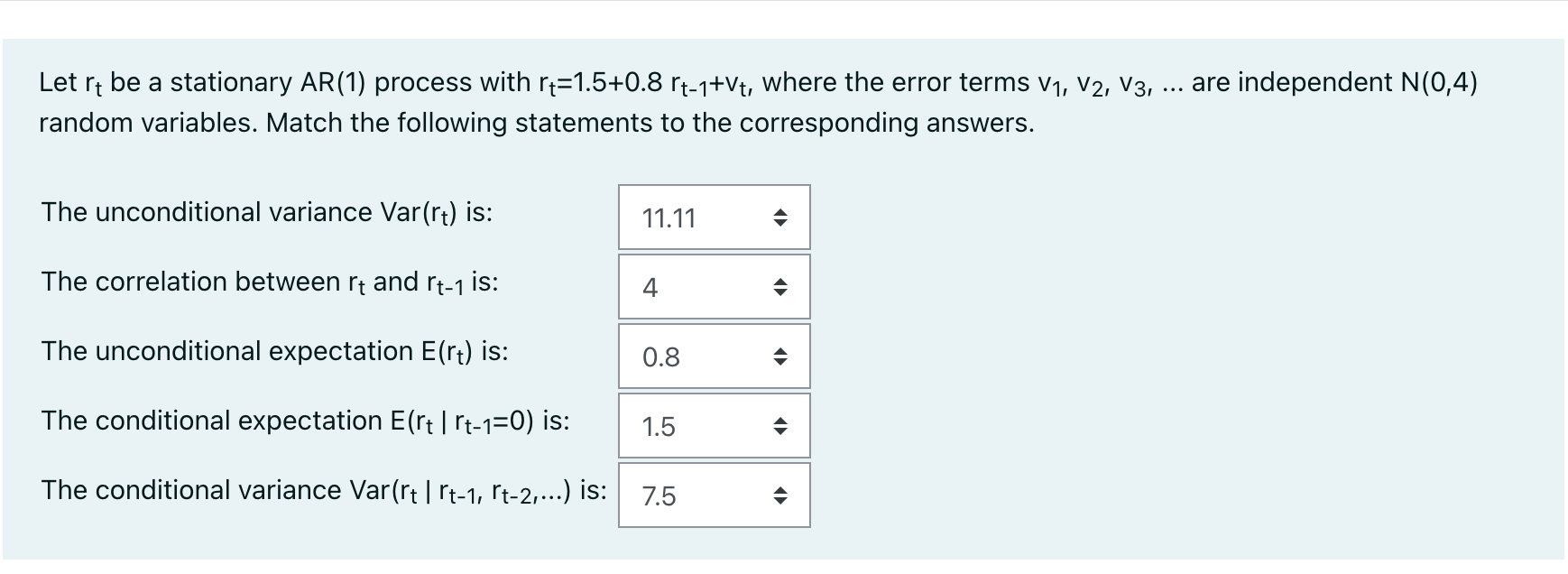

are independent N(0,4) Let rt be a stationary AR (1) process with rt=1.5+0.8 rt-1+Vt, where the error terms V1, V2, V3, random variables. Match the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Crypto Currency Trading The Topics Of Bitcoin And Cryptocurrency

Authors: Bell Bavaro

1st Edition

979-8354124695