Answered step by step

Verified Expert Solution

Question

1 Approved Answer

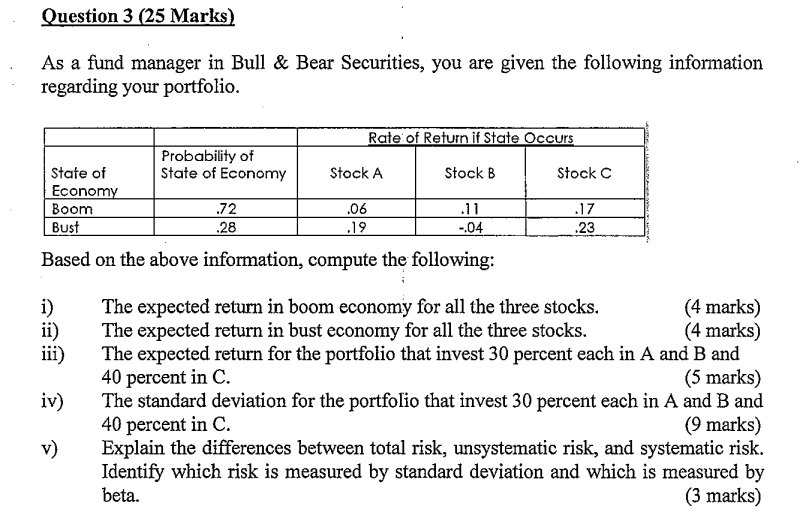

As a fund manager in Bull & Bear Securities, you are given the following information regarding your portfolio. Based on the above information, compute the

As a fund manager in Bull \& Bear Securities, you are given the following information regarding your portfolio. Based on the above information, compute the following: i) The expected return in boom economy for all the three stocks. (4 marks) ii) The expected return in bust economy for all the three stocks. (4 marks) iii) The expected return for the portfolio that invest 30 percent each in A and B and 40 percent in C. (5 marks) iv) The standard deviation for the portfolio that invest 30 percent each in A and B and 40 percent in C. ( 9 marks) v) Explain the differences between total risk, unsystematic risk, and systematic risk. Identify which risk is measured by standard deviation and which is measured by beta

As a fund manager in Bull \& Bear Securities, you are given the following information regarding your portfolio. Based on the above information, compute the following: i) The expected return in boom economy for all the three stocks. (4 marks) ii) The expected return in bust economy for all the three stocks. (4 marks) iii) The expected return for the portfolio that invest 30 percent each in A and B and 40 percent in C. (5 marks) iv) The standard deviation for the portfolio that invest 30 percent each in A and B and 40 percent in C. ( 9 marks) v) Explain the differences between total risk, unsystematic risk, and systematic risk. Identify which risk is measured by standard deviation and which is measured by beta Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrency Trading Guide For Beginners

Authors: Miquel Vidal ,Joan Garcia Guerrero

1st Edition

979-8705488575