based on the information provided, make a retirement analysis much like this example given below.

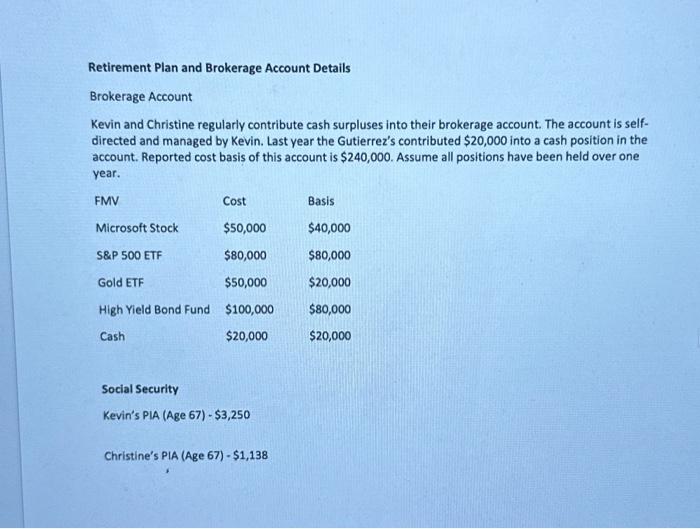

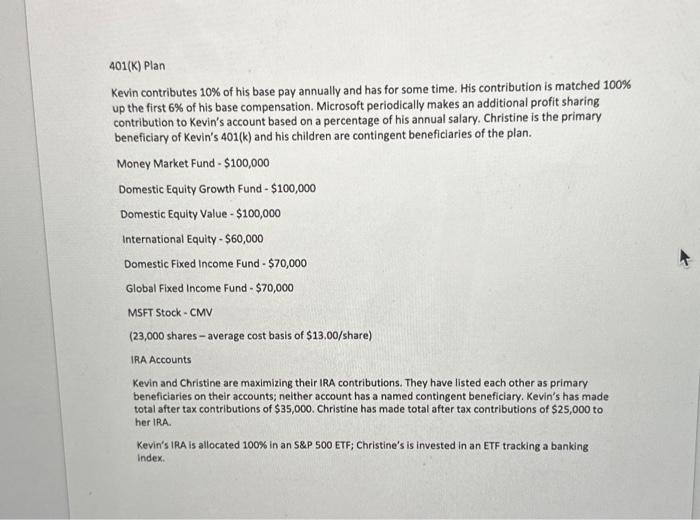

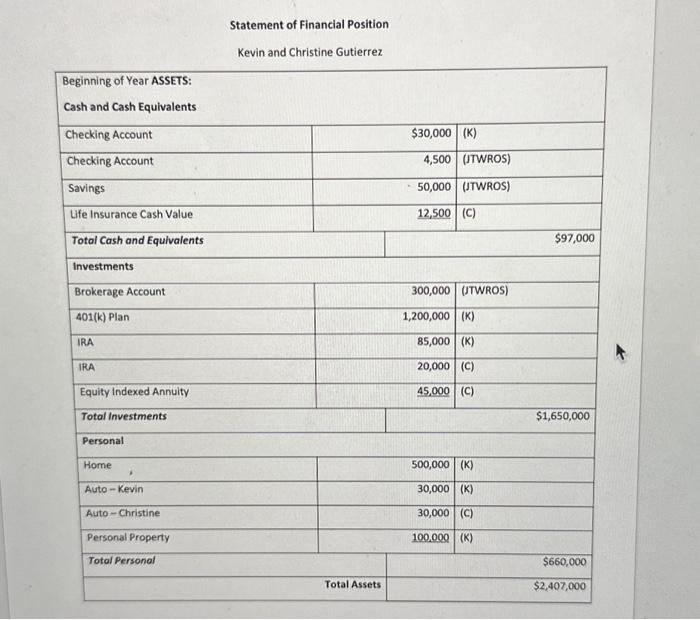

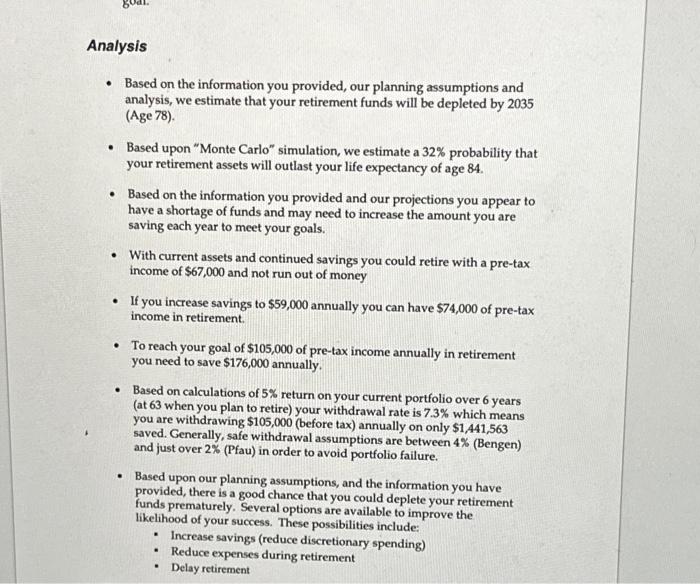

Retirement Plan and Brokerage Account Details Brokerage Account Kevin and Christine regularly contribute cash surpluses into their brokerage account. The account is selfdirected and managed by Kevin. Last year the Gutierrez's contributed $20,000 into a cash position in the account. Reported cost basis of this account is $240,000. Assume all positions have been held over one year. Social Security Kevin's PIA (Age 67) - $3,250 Christine's PIA (Age 67) - \$1,138 Statement of Financial Position 401(K) Plan Kevin contributes 10% of his base pay annually and has for some time. His contribution is matched 100% up the first 6% of his base compensation. Microsoft periodically makes an additional profit sharing contribution to Kevin's account based on a percentage of his annual salary. Christine is the primary beneficiary of Kevin's 401(k) and his children are contingent beneficiaries of the plan. Money Market Fund - $100,000 Domestic Equity Growth Fund - $100,000 Domestic Equity Value - $100,000 International Equity - $60,000 Domestic Fixed income Fund - $70,000 Global Fixed Income Fund - $70,000 MSFT Stock - CMV (23,000 shares - average cost basis of $13.00/ share) IRA Accounts Kevin and Christine are maximizing their IRA contributions. They have listed each other as primary beneficiaries on their accounts; neither account has a named contingent beneficiary. Kevin's has made total after tax contributions of $35,000. Christine has made total after tax contributions of $25,000 to her IRA. Kevin's IRA is allocated 100\% in an S\&P 500 ETF; Christine's is invested in an ETF tracking a banking index. - Based on the information you provided, our planning assumptions and analysis, we estimate that your retirement funds will be depleted by 2035 (Age 78). - Based upon "Monte Carlo" simulation, we estimate a 32% probability that your retirement assets will outlast your life expectancy of age 84. - Based on the information you provided and our projections you appear to have a shortage of funds and may need to increase the amount you are saving each year to meet your goals. - With current assets and continued savings you could retire with a pre-tax income of $67,000 and not run out of money - If you increase savings to $59,000 annually you can have $74,000 of pre-tax income in retirement. - To reach your goal of $105,000 of pre-tax income annually in retirement you need to save $176,000 annually. - Based on calculations of 5% return on your current portfolio over 6 years (at 63 when you plan to retire) your withdrawal rate is 7.3% which means you are withdrawing $105,000 (before tax) annually on only $1,441,563 saved. Generally, safe withdrawal assumptions are between 4% (Bengen) and just over 2% (Pfau) in order to avoid portfolio failure. - Based upon our planning assumptions, and the information you have provided, there is a good chance that you could deplete your retirement funds prematurely. Several options are available to improve the likelihood of your success. These possibilities include: - Increase savings (reduce discretionary spending) - Reduce expenses during retirement - Delay retirement Economic Environment Kevin will likely not receive any additional raises with Microsoft. He anticipates his compensation will remain constant through his age 65 ; and that he could potentially be offered a retirement package before then. Kevin and Christine have made the following assumptions in their personal financial plan: They are open to suggestions from a qualified professional if their assumptions are not appropriate. Long Term Inflation Rate 2.0% Large Cap Equities will have greater than a 6% return over time Kevin and Christine believe federal marginal tax rates will likely increase over time. Their highest marginal tax rate is currently 30% and they are subject to a flat 4.95% state income tax. Interest rates on mortgages are currently 4.10% on a 30 year note, and 3.45% on a 15 -year note. Rates are expected to increase. Insurance and Risk Management Data Life Insurance - Kevin has a group term life insurance policy of twice his base salary ($280,000). The beneficiary is Christine and contingent beneficiaries are Tony and Amanda per stipes. - Christine has a whole life insurance policy with a $50,000 death benefit. She purchased the policy when Ryan was born; it currently has a cash value of $12,500 with no remaining surrender charge. The policy has a guaranteed minimum rate of 3.0%. Premiums are $1,000 annually; Ryan is the sole beneficiary of this policy. Long Term Care Insurance - Kevin and Christine do not currently have long term care insurance. They recently received an insurance quote qualified long term care insurance. The aggregate premium on policies for Kevin and Christine was $300 a month for Kevin and $200 month for Christine, or $6,000 annually. Kevin and Christine Gutierrez Kevin and Christine are prospects you met last month. They were introduced through one of your top clients, and you believe they would make fantastic clients. Kevin is nearing retirement at Microsoft and is well regarded within the company. His opinion is valued and he would be a strong center of influence to your client base. Christine works part time in a local doctor's office and truly enjoys her work. Kevin's mother, Gloria, has recently moved into the home. Christine and Kevin expressed a fantastic disposition and indicated they have been married for the past decade. They both have children from previous marriages and are interested in a long term financial planning relationship. Background Kevin Gutierrez - 61 Kevin is a Sr. Vice President of sales at Microsoft. He heads a department of 30 and is integral in the development of smart phone technology. He has been with Microsoft for the past 15 years, and in that time has received numerous advancements. He would like to end his career with the company. Kevin enjoys spending time with Christine and has a strained relationship with children from his first marriage, Tony and Amanda. Kevin's father died from a heart attack at 50, and from that experience Kevin maintains a healthy diet and weight. Kevin is an aggressive investor who believes in Microsoft over the long term. Christine Gutierrez - 50 Christine works as a medical assistant at a local doctor's office on a part time basis; three days a week. She is considering working full time after Ryan has moved away from the home. Christine enjoys traveling and cooking and has a strong relationship with Ryan. Christine is uncertain about Gloria moving into the home. Both of Christine's parents are healthy and live in a retirement community in Texas. Christine is a risk tolerant investor and prefers to have at least three months of living expenses available in cash. Gloria Gutierrez -82 Gloria is Kevin's mother and recently moved into Christine and Kevin's home. Gloria is no longer able to drive and relies on Christine and Kevin for most of her daily activities; Gloria's annual living expenses average $2,000 a month. She receives social security retirement of $800 a month, and has a savings account of $310,000 from the sale of her home. Gloria is in fair health, with early signs of osteoporosis. Disability Insurance - Kevin has a group long term disability policy that provides him with 60% of his base salary and pays for the longer of five years or until he reaches age 65 . The premium is paid completely by his employer and policy has a six month waiting period. - Kevin has chosen not to participate in his short-term disability policy. The policy would provide 75% of Kevin's base compensation for the first six months of a disability. Short-term coverage would be subject to a three-week waiting period and cost approximately $22 a month. - Christine does not have any disability coverage Medical Insurance - Kevin and Christine are covered under Kevin's group insurance plan. The plan allows coverage within a preferred provider network, all of Christine and Kevin's doctors are within this network. The plan assesses a $50 co-pay per visit and covers 100% of in-network doctor costs. The plan only pays 50% of out of network costs and is subject to a $10,000 annual out of pocket family maximum. Kevin pays $100 a month for his portion of health insurance premiums. - Gloria is currently enrolled in Medicare part A, B and has opted into a local part D coverage plan. Homeowners Coverage - Coverage: $350,000 with a replacement value endorsement on personal property. The home has antique hardwood floors and the replacement cost of the home is $600,000. The policy has a deductible of $5,000 and a premium of $3,000 annually. Automobile Coverage - Kevin's Honda Accord and Christine's Ford Explorer both carry collision and other than collision (comprehensive) coverage. Kevin and Christine have impeccable driving records and carry state minimum liability insurance limits. The policies each carry a $500 deductible and have aggregate annual premiums of $1,500;$750 each. - $25,000 Bodily injury-one person - $50,000 Bodily injury-all persons $30,000 Property damage Equity Indexed Annuity - Christine owns a deferred equity indexed annuity, Last year, the contract value was $45,000. The annuity has an annual guaranteed rate of 1%. Annual performance is calculated on a weekly measure of the S\&P 500 performance and capped at a 0.23% weekly crediting rate. The annuity contract is non-qualified and was purchased three years ago for $40,000. The contract has a surrender charge of 4% remaining. The surrender charge reduces by 1% annually, Tony (17) and Amanda (24) Tony and Amanda have a distant relationship with their father. They harbor resentment from his divorce and do not actively participate in his life, but do call to talk to their grandmother. Kevin would like to reestablish a connection with his children. Tony's mother claims him as a dependent; Tony's mother and Amanda both work in retail and earn approximately $40,000 annually. Kevin is interested in helping pay for Tony's education at a state school in IL. He would like to see costs and how he can do this. Ryan Smith - 24 Ryan recently moved back home after being unable to find employment. He has a MS in fine arts from Maryland State. He is currently working part time at Starbucks earning approximately $100 a week and is hunting for a full time job. Kevin and Christine are willing to help Ryan pay for health coverage; he has a chronic back injury. Kevin and Christine provide more than half of Ryan's support. When Ryan was 19 he was convicted of a felony drug conviction and received a suspended sentence. Ryan was allowed to attend college. He still meets regularly with his probation officer. Kevin and Christine are concerned about Ryan's relapsing and ability to manage money. Case Narrative Christine and Kevin met fifteen years ago at a church singles function. After dating for five years, they married and moved into Kevin's home, which is located in IL. Ryan and Gloria have both recently moved into the home and Christine has found herself responsible for most of the caretaking duties. Neither Ryan nor Gloria is paying rent, and in your first meeting with these prospects Christine expressed she was becoming frustrated with her new caretaking responsibilities. Tony and Amanda have not spoken with Kevin directly in the past few years, and Ryan moving into the home has not relieved stress in the Gutierrez family. Kevin has included his children in some of his planning decisions; but is unsure if he will continue to list them as beneficiaries on retirement accounts. Christine does not have a relationship with Tony or Amanda but is interested in getting to know them. Currently they have no estate planning documents in place. Kevin's reasoning behind this is that if he were to die his wife would get everything and vice versa. Under the rare chance that they should both die at the same time they believe their families will do what's right. Financial Planning Objectives In your first meeting with the client; the Gutierrez's expressed the following financial planning objectives. They are listed in order of priority to the family. - Relieve the caretaker burden currently placed on Christine - Consider purchasing a vacation condo in Maui to enjoy today and during retirement. The condo costs $400,000 in today's dollars; Kevin would like to put at least 25% down on this purchase. Christine is not fully on board with a second home. - Both spouses retire at Kevin's age 65 able to spend approximately 70% of what they do today - Revisit the allocation of their investment portfolios - Review their estate plan and ensure Christine would be able to maintain her standard of living if Kevin died today - They are open to other suggestions (recommendations) that they may be missing or haven't thought of yet