CANNOT FIGURE OUT PART C !! NEED HELP PLEASE!

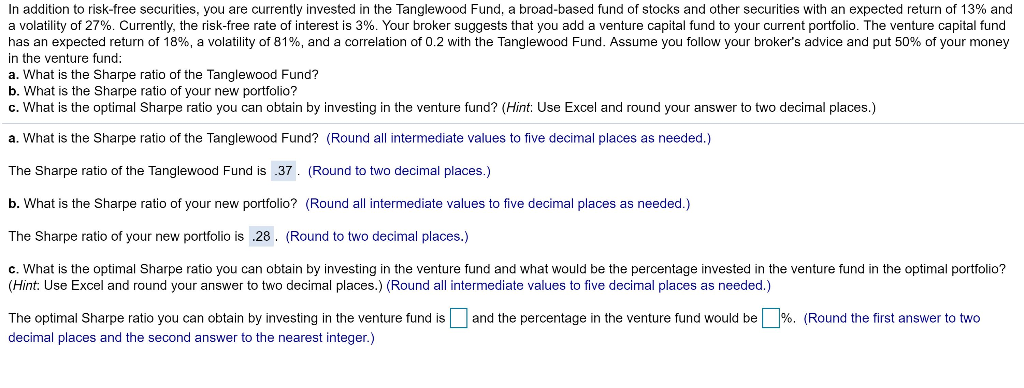

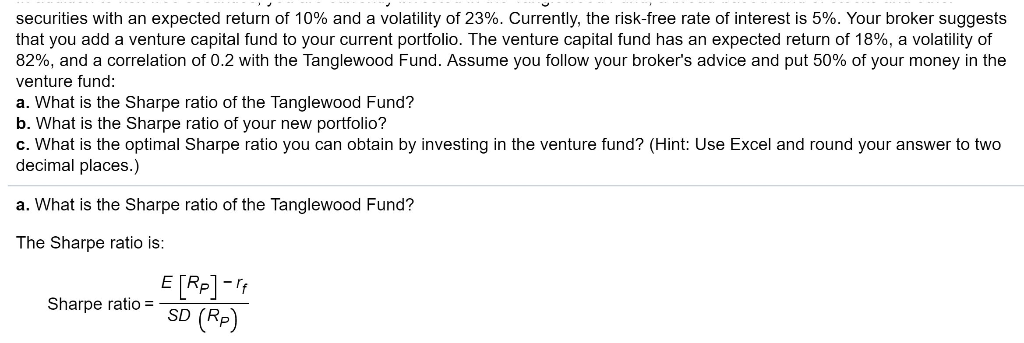

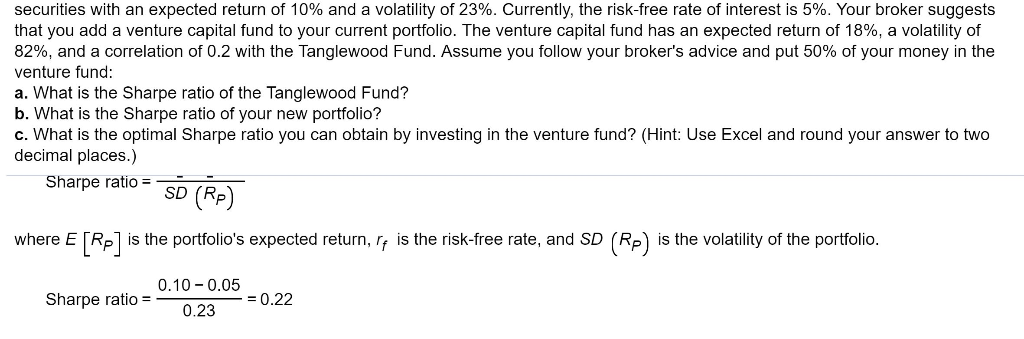

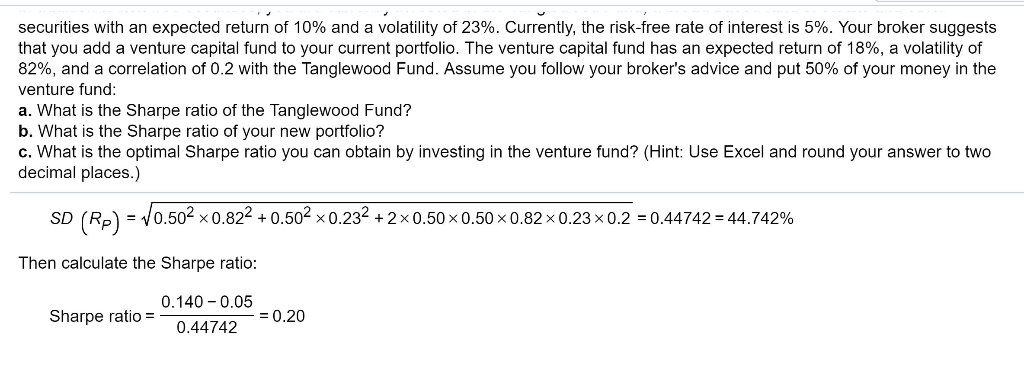

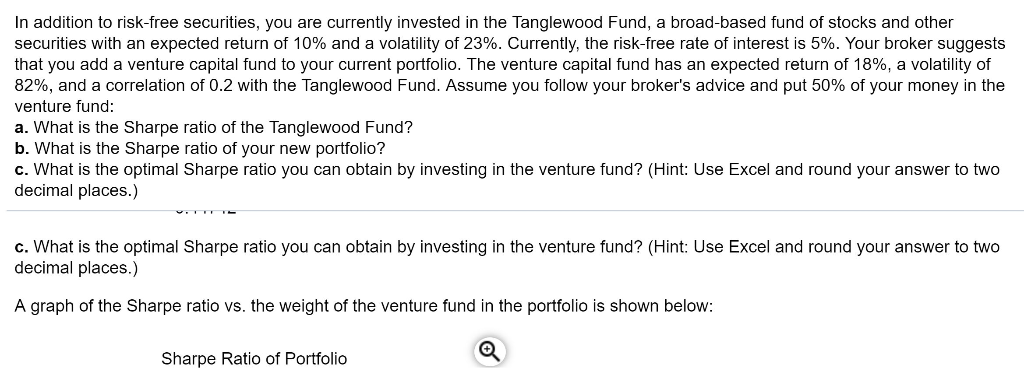

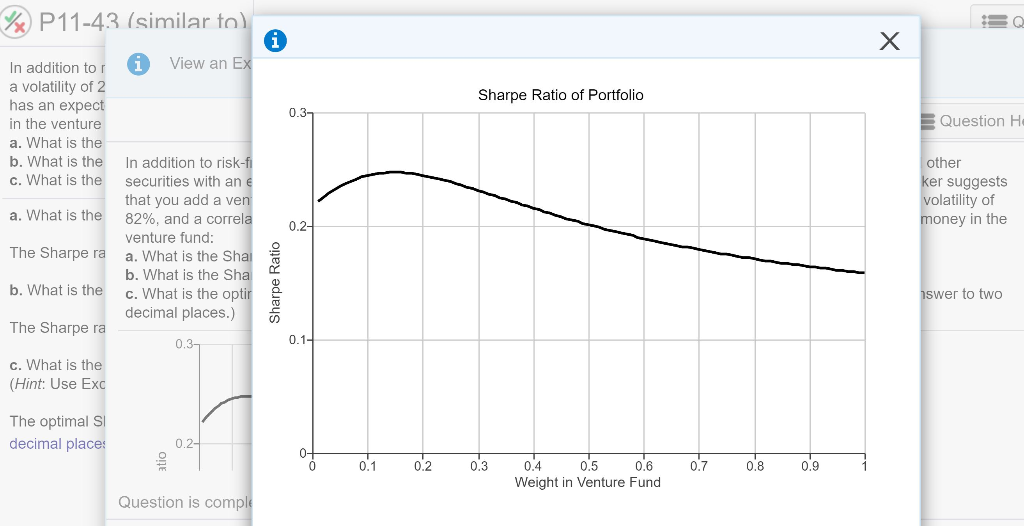

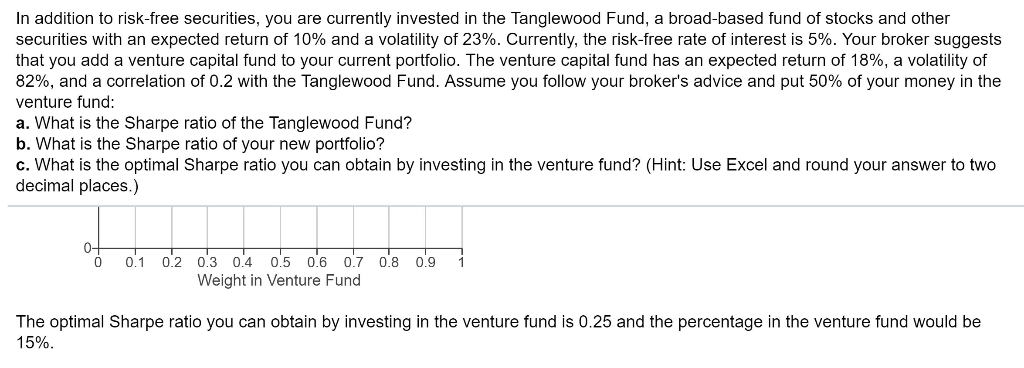

In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund of stocks and other securities with an expected return of 13% and volatility of 27%. Currently, the risk-free rate of interest is 3%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 81%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) a. What is the Sharpe ratio of the Tanglewood Fund? (Round all intermediate values to five decimal places as needed.) The Sharpe ratio of the Tanglewood Fund is .37 (Round to two decimal places.) b. What is the Sharpe ratio of your new portfolio? (Round all intermediate values to five decimal places as needed.) The Sharpe ratio of your new portfolio is .28. (Round to two decimal places.) fund and what What is the optimal Sharpe ratio you can obtain by investing (Hint: Use Excel and round your answer to two decimal places.) (Round all intermediate values to five decimal places as needed.) vent percentage invested in the venture fund optimal portfc and the percentage in the venture fund would be %. (Round the first answer to two The optimal Sharpe ratio you can obtain by investing in the venture fund is decimal places and the second answer to the nearest integer.) securities with an expected return of 10% and a volatility of 23%. Currently, the risk-free rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) a. What is the Sharpe ratio of the Tanglewood Fund? The Sharpe ratio is: E [RP]- (Rp) Sharpe ratio SD securities with an expected return of 10% and a volatility of 23%. Currently, the risk-free rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) Sharpe ratio (RP) SD where E Rp is the volatility of the portfolio (RP) is the portfolio's expected return, rf is the risk-free rate, and SD 0.10 0.05 = 0.22 Sharpe ratio= 0.23 securities with an expected return of 10% and a volatility of 23%. Currently, the risk-freee rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) b. What is the Sharpe ratio of your new portfolio? First calculate the volatility of the new portfolio. The volatility is the square root of the variance: (Rp)= (R2) +2 x x xx2 x Cov SD (R) (RR2) x Var x Var - and 2, respectively, Var (R, and Var (R2 are the variances of assets 1 and 2 where x, and x2 are the weights for assets securities with an expected return of 10% and a volatility of 23%. Currently, the risk-free rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) First calculate the volatility of the new portfolio. The volatility is the square root of the variance: (R) x (Rp) SD x Var (R2) +2xX1 X X2 x Cov (R1 R2) x Var and Var (R2 and 2, respectively, Var (R) where x and x2 are the weights for assets are the variances of assets 1 and 2, respectively, and Cov (R1,R2) is the covariance between assets 1 and 2 securities with an expected return of 10% and a volatility of 23%. Currently, the risk-free rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) (RP 0.502 x 0.822 0.502 x0.23 2 x 0.50 x 0.50 x 0.82 x 0.23 x 0.2 0.44742 = 44.742% SD + Then calculate the Sharpe ratio: 0.140 0.05 =0.20 Sharpe ratio = 0.44742 In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund of stocks and other securities with an expected return of 10% and a volatility of 23%. Currently, the risk-free rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) A graph of the Sharpe ratio vs. the weight of the venture fund in the portfolio is shown below: Sharpe Ratio of Portfolio P11-43 (similar fo). i View an Ex X In addition tor a volatility of 2 has an expect Sharpe Ratio of Portfolio 0.3 Question H in the venture a. What is the b. What is the In addition to risk-f securities with an e that you add a ven 82%, and a correla venture fund: a. What is the Sha b. What is the Sha c. What is the optir decimal places.) other ker suggests volatility of money in the c. What is the a. What is the 0.2 The Sharpe ra b. What is the swer to two The Sharpe ra 0.1 0.3 c. What is the (Hint: Use Exc The optimal S decimal place 0.2- 0+ 0.7 0.9 0.1 0.2 0.3 0.5 Weight in Venture Fund 04 0.6 Question is compl Sharpe Ratio In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund of stocks and other securities with an expected return of 10% and a volatility of 23%. Currently, the risk-free rate of interest is 5%. Your broker suggests that you add a venture capital fund to your current portfolio. The venture capital fund has an expected return of 18%, a volatility of 82%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's advice and put 50% of your money in the venture fund: a. What is the Sharpe ratio of the Tanglewood Fund? b. What is the Sharpe ratio of your new portfolio? c. What is the optimal Sharpe ratio you can obtain by investing in the venture fund? (Hint: Use Excel and round your answer to two decimal places.) 0- 0:2 0.3 04 0.5 0.6 0.7 0.8 0.9 Weight in Venture Fund 0.1 The optimal Sharpe ratio you can obtain by investing in the venture fund is 0.25 and the percentage in the venture fund would be 15%