Answered step by step

Verified Expert Solution

Question

1 Approved Answer

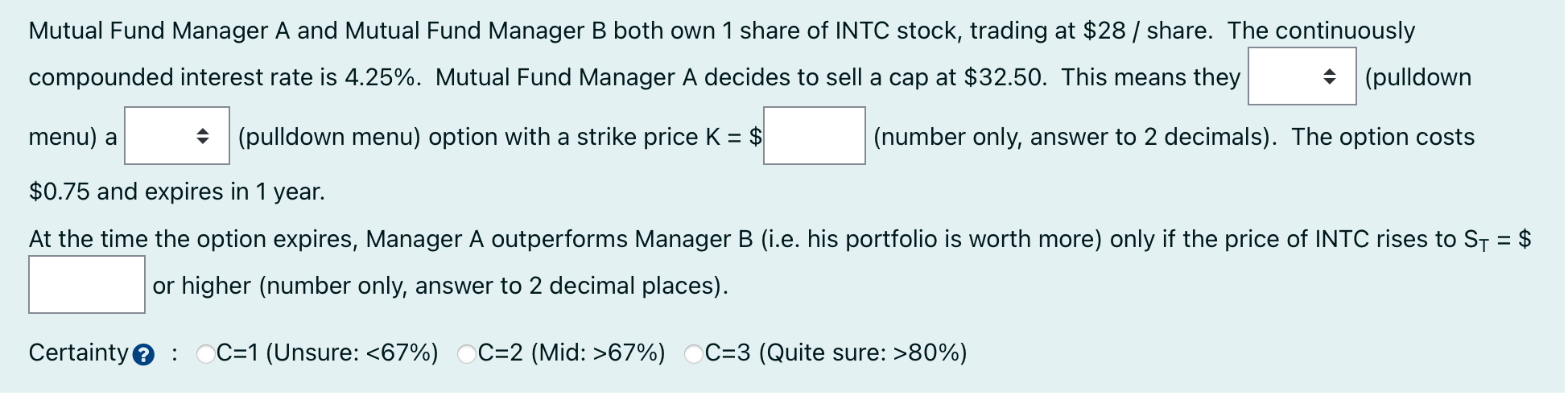

choose from sell/buy, put/call Mutual Fund Manager A and Mutual Fund Manager B both own 1 share of INTC stock, trading at $28/ share. The

choose from sell/buy, put/call

choose from sell/buy, put/call

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Pricing Models In Continuous Time And Kalman Filtering

Authors: B.Philipp Kellerhals

1st Edition

3540423648, 3662219018, 9783540423645, 9783662219010