Answered step by step

Verified Expert Solution

Question

1 Approved Answer

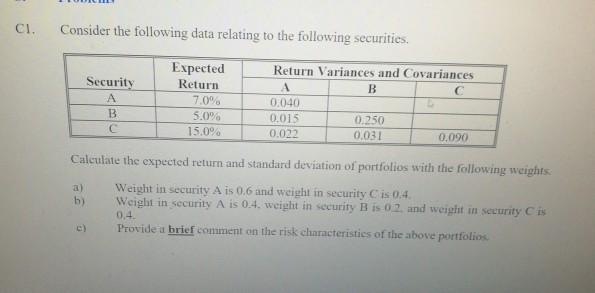

Cl. Consider the following data relating to the following securities. Expected Return Return Variances and Covariances Security 7.0% 5.0% 15.000 | 0.022 0.040 0.015 .231-0.090

Cl. Consider the following data relating to the following securities. Expected Return Return Variances and Covariances Security 7.0% 5.0% 15.000 | 0.022 0.040 0.015 .231-0.090 0.250 Calculate the expected return and standard deviation of portfolios with the following weights a) Weight in security A is 0.6 and weight in security C is 0.4 b) Weight in security A is 0.4, weight in security iB is 0.2, and weight in security Cs 0.4. Provide a brief comment on the risk characteristics of the above portfolios. c)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Empire In Pawn Being Lectures And Essays On Indian Colonial And Domestic Finance Preference Free Trade Etc

Authors: A. J. (Alexander Johnstone) Wilson

1st Edition

1290631565, 9781290631563