Answered step by step

Verified Expert Solution

Question

1 Approved Answer

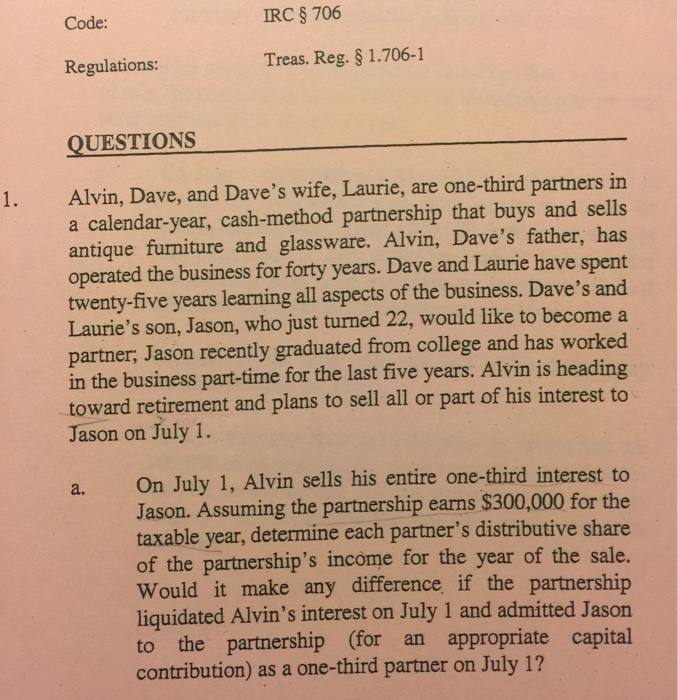

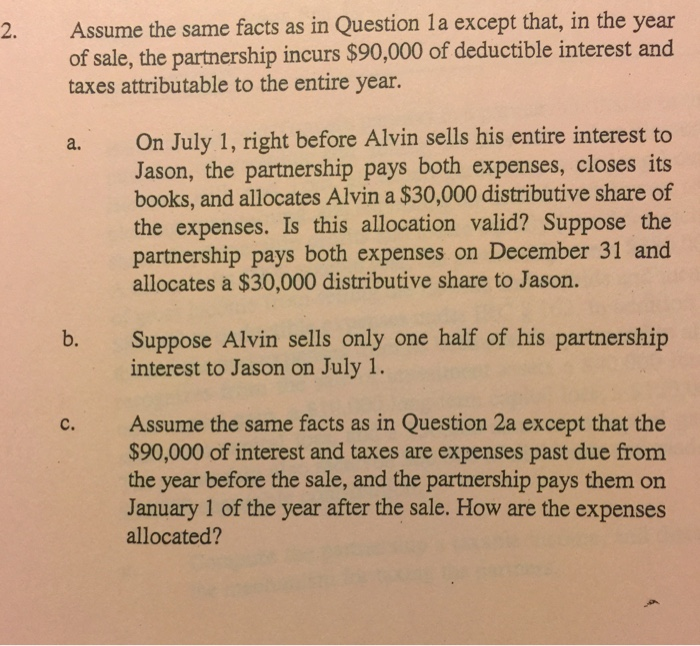

Code: IRC 8 706 Regulations: Treas. Reg. S 1.706-1 QUESTIONS Alvin, Dave, and Dave's wife, Laurie, are one-third partners in a calendar-year, cash-method partnership that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Risk In The Operation Of EDF Financed Projects

Authors: Koffi Rufin Kouame

1st Edition

6205912651, 978-6205912652