Question

Consider a riskless spread with a long position in the August 160 call and a short position in the October 160 call. Determine the appropriate

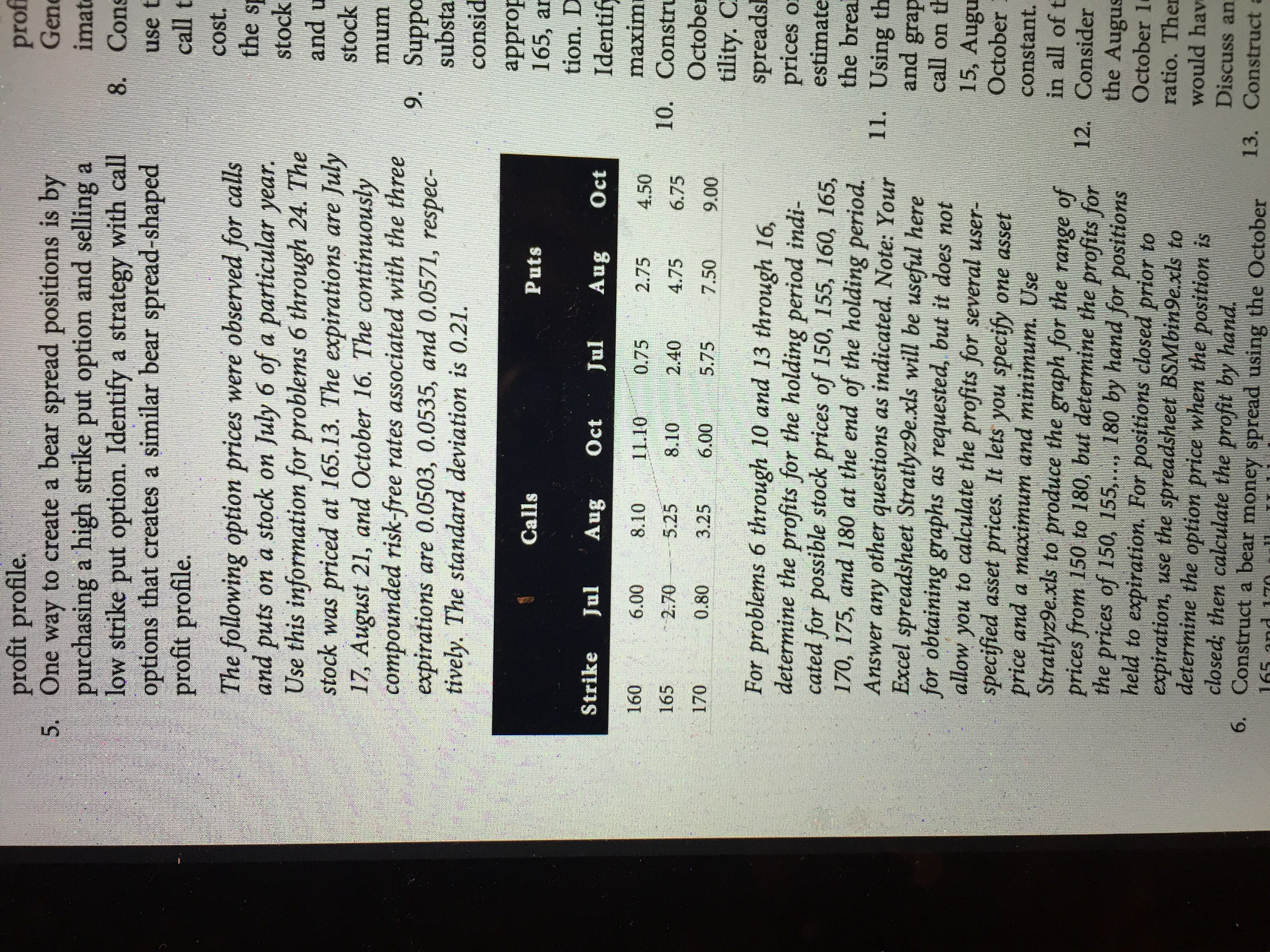

Consider a riskless spread with a long position in the August 160 call and a short position in the October 160 call. Determine the appropriate hedge ratio. Then show how a $1 stock price increase would have a neutral effect on the spread value. Discuss any limitations of this procedure.

Consider a riskless spread with a long position in the August 160 call and a short position in the October 160 call. Determine the appropriate hedge ratio. Then show how a $1 stock price increase would have a neutral effect on the spread value. Discuss any limitations of this procedure.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Environmental And Sustainable Finance

Authors: Vikash Ramiah, Greg N. Gregoriou

1st Edition

012803615X, 978-0128036150