Answered step by step

Verified Expert Solution

Question

1 Approved Answer

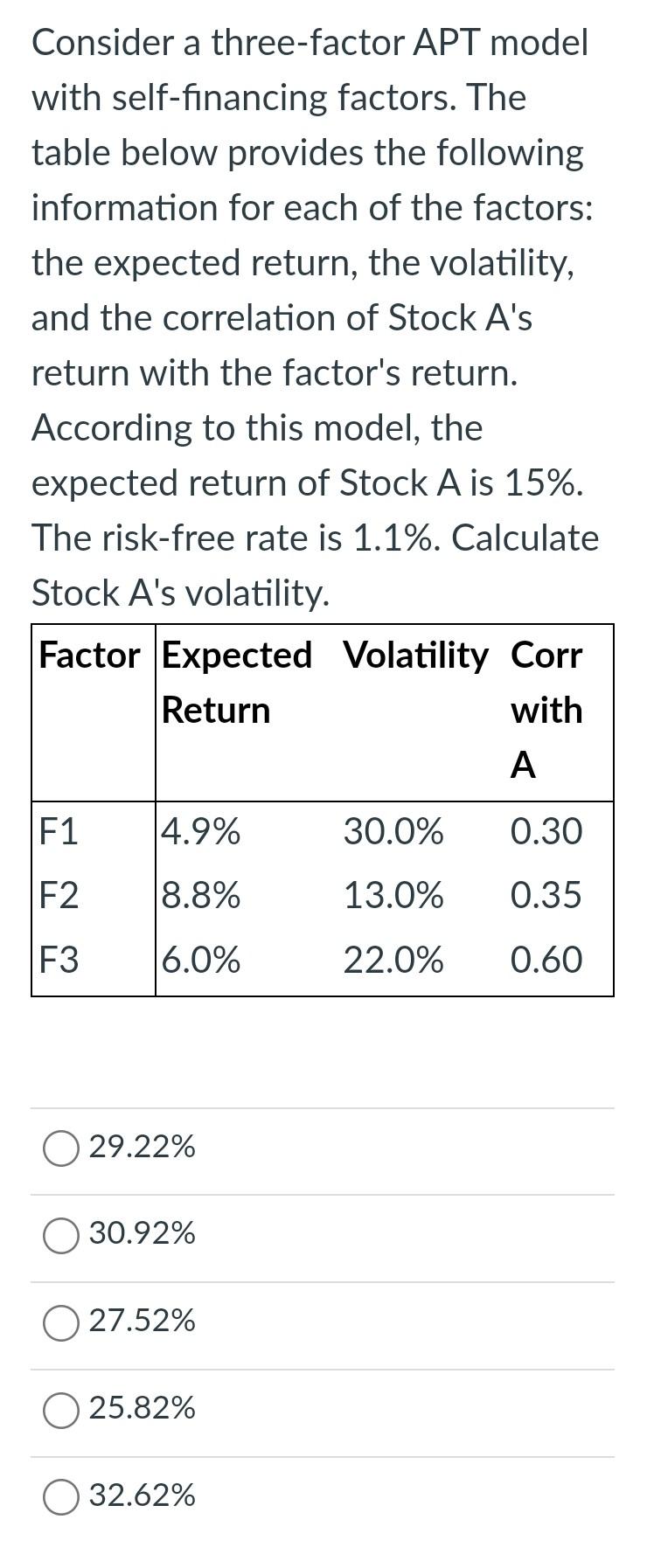

Consider a three-factor APT model with self-financing factors. The table below provides the following information for each of the factors: the expected return, the volatility,

Consider a three-factor APT model with self-financing factors. The table below provides the following information for each of the factors: the expected return, the volatility, and the correlation of Stock A's return with the factor's return. According to this model, the expected return of Stock A is 15%. The risk-free rate is 1.1%. Calculate Stock A's volatility. Factor Expected Volatility Corr Return with A F1 4.9% 30.0% 0.30 F2 8.8% 13.0% 0.35 F3 6.0% 22.0% 0.60 29.22% 30.92% 0 27.52% 25.82% 32.62%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Business Of Finance

Authors: Withers Hartley 1867 1950

1st Edition

1313069299, 9781313069298