Answered step by step

Verified Expert Solution

Question

1 Approved Answer

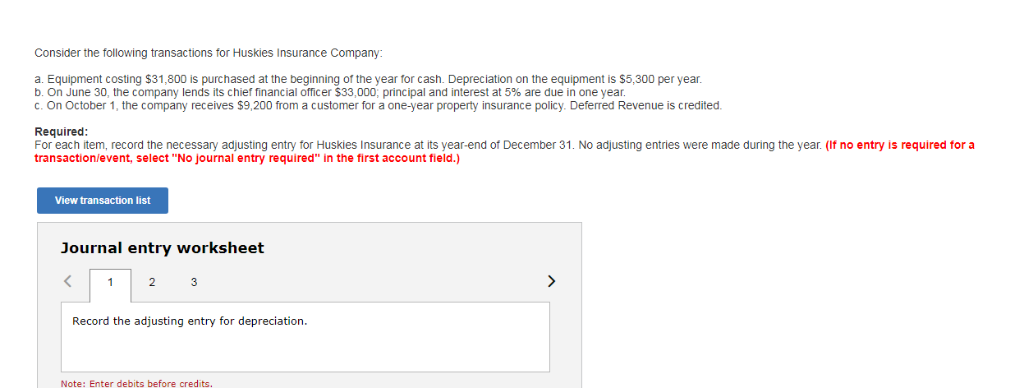

Consider the following transactions for Huskies Insurance Company: Equipment costing $31,800 b. On June 30, the company lends its chief financial officer $33,000 principal and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Operational Auditing

Authors: David G Komatz

1st Edition

B09K24NM14, 979-8751454357