Answered step by step

Verified Expert Solution

Question

1 Approved Answer

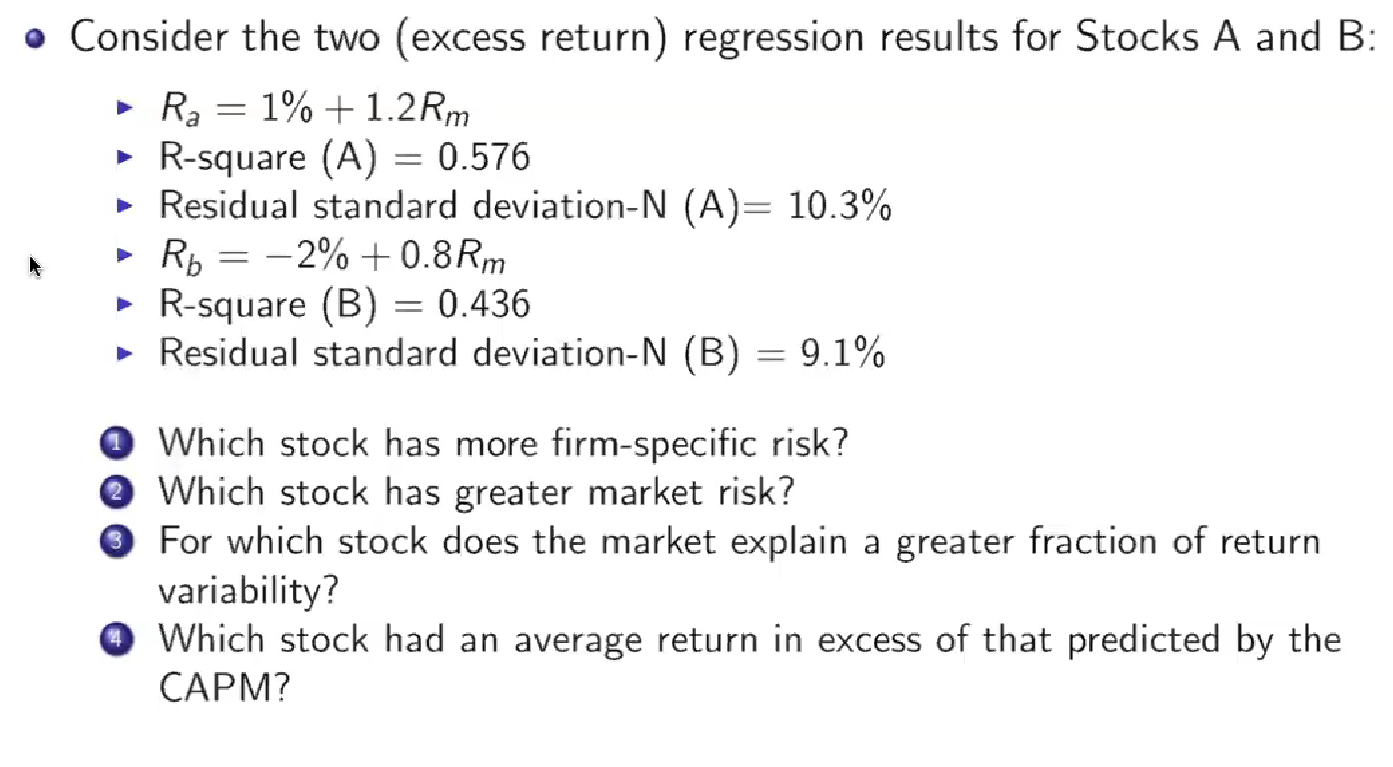

Consider the two (excess return) regression results for Stocks A and B: - Ra=1%+1.2Rm - R-square (A)=0.576 - Residual standard deviation- N(A)=10.3% - Rb=2%+0.8Rm -

Consider the two (excess return) regression results for Stocks A and B: - Ra=1%+1.2Rm - R-square (A)=0.576 - Residual standard deviation- N(A)=10.3% - Rb=2%+0.8Rm - R-square (B)=0.436 - Residual standard deviation-N (B)=9.1% Which stock has more firm-specific risk? Which stock has greater market risk? For which stock does the market explain a greater fraction of return variability? Which stock had an average return in excess of that predicted by the CAPM

Consider the two (excess return) regression results for Stocks A and B: - Ra=1%+1.2Rm - R-square (A)=0.576 - Residual standard deviation- N(A)=10.3% - Rb=2%+0.8Rm - R-square (B)=0.436 - Residual standard deviation-N (B)=9.1% Which stock has more firm-specific risk? Which stock has greater market risk? For which stock does the market explain a greater fraction of return variability? Which stock had an average return in excess of that predicted by the CAPM Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Personal Finance Beginning Your Financial Journey

Authors: Lance Palmer, John E. Grable

2nd Edition

1119797063, 978-1119797067