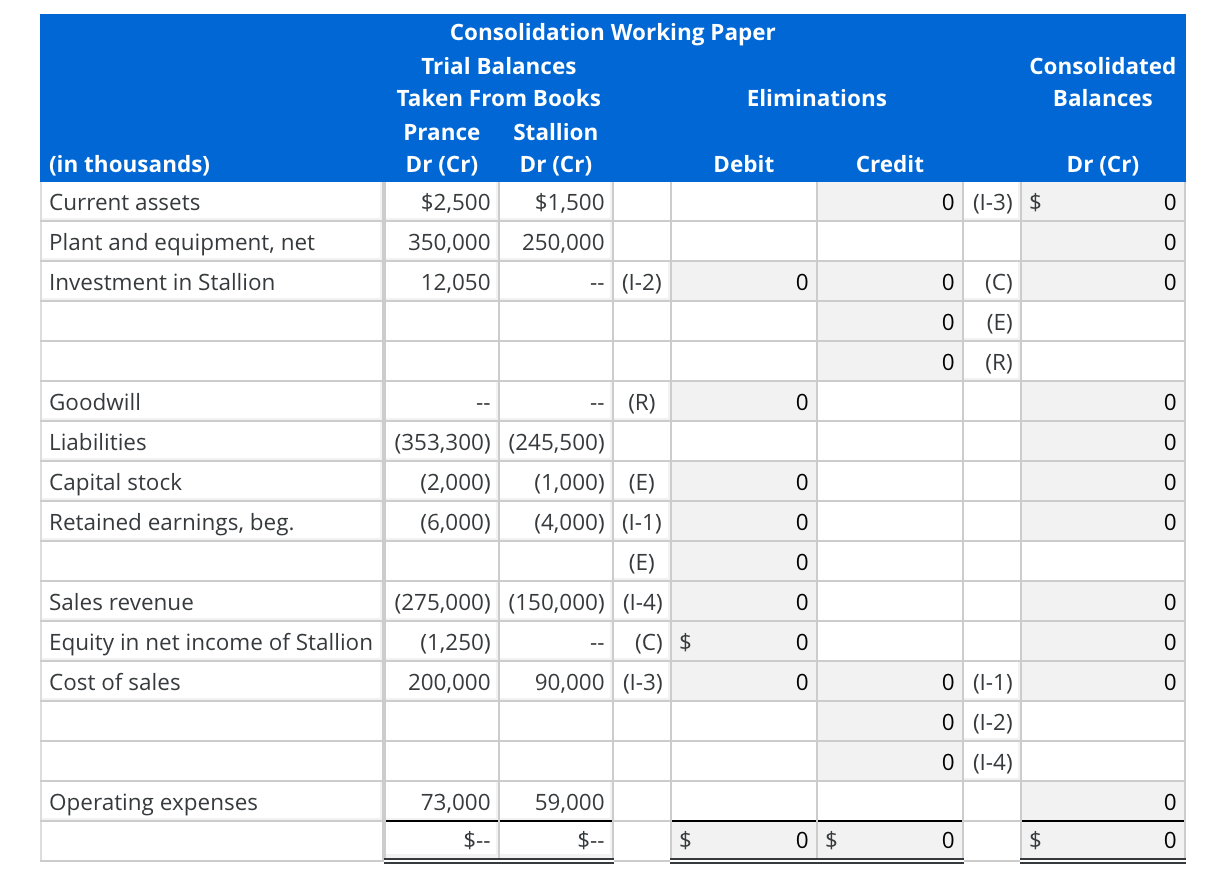

Consolidation Working Paper Eliminations, Intercompany Merchandise Sales

Prance Athleticwear Company owns all of the voting stock of Stallion Shoes. Acquisition cost was $7 million in excess of Stallions book value of $3 million, and the excess was attributed entirely to goodwill. As of the beginning of the current year, goodwill is impaired by $500,000. Goodwill is not impaired in the current year. Following is information on intercompany merchandise transactions between Prance and Stallion for the current year:

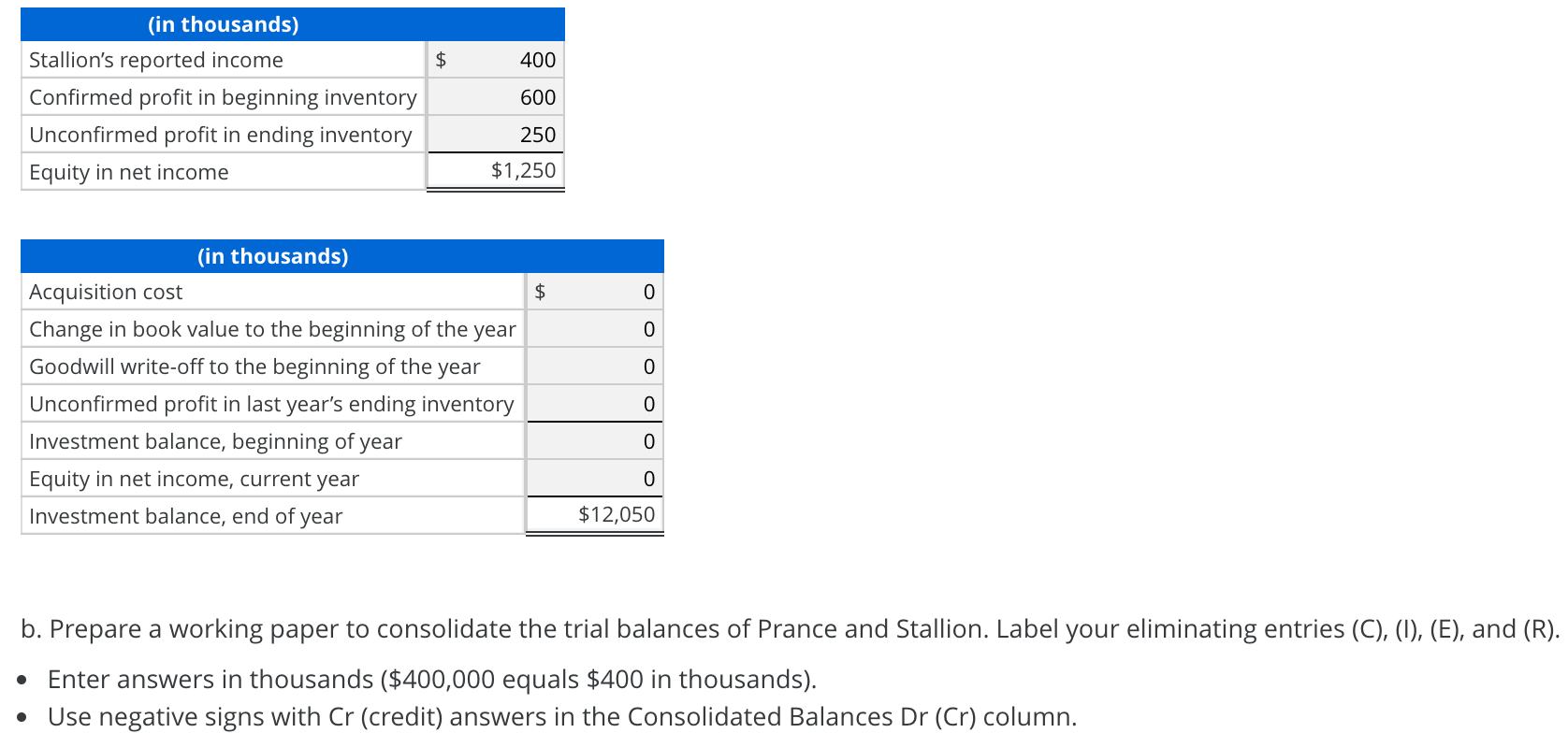

Intercompany profit in Prances beginning inventory, purchased from Stallion, is $300,000.

Intercompany profit in Stallions beginning inventory, purchased from Prance, is $400,000.

Intercompany profit in Prances ending inventory, purchased from Stallion, is $200,000.

Intercompany profit in Stallions ending inventory, purchased from Prance, is $250,000.

Total sales from Stallion to Prance, at the price charged to Prance, were $7 million.

Total sales from Prance to Stallion, at the price charged to Stallion, were $5 million.

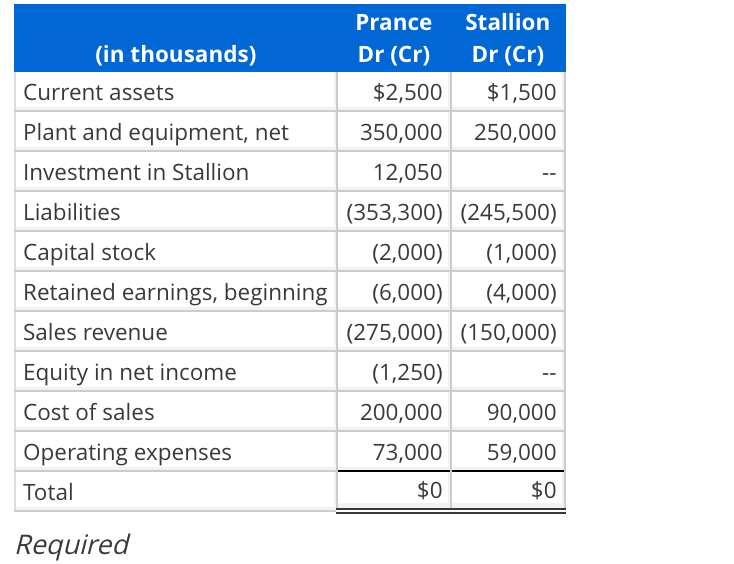

Prance uses the complete equity method to account for its investment in Stallion on its own books. The separate trial balances for Prance and Stallion at the end of the current year are below.

a. Prepare a schedule calculating equity in net income for the current year, appearing on Prances separate books ($1,250,000) and the end-of-year balance for Investment in Stallion, appearing on Prances separate books ($12,050,000).

- Enter answers in thousands ($400,000 equals $400 in thousands).

- Use negative signs with answers that reduce net income and the investment balance.

-

(in thousands) Current assets Plant and equipment, net Investment in Stallion Liabilities Capital stock Retained earnings, beginning Sales revenue Prance Stallion Dr (Cr) Dr (Cr) $2,500 $1,500 350,000 250,000 12,050 (353,300) (245,500) (2,000) (1,000) (6,000) (4,000) (275,000) (150,000) (1,250) 200,000 90,000 73,000 59,000 $0 $0 Equity in net income Cost of sales Operating expenses Total Required $ (in thousands) Stallion's reported income Confirmed profit in beginning inventory Unconfirmed profit in ending inventory Equity in net income 400 600 250 $1,250 0 (in thousands) Acquisition cost Change in book value to the beginning of the year Goodwill write-off to the beginning of the year Unconfirmed profit in last year's ending inventory ding inventory Investment balance, beginning of year Equity in net income, current year Investment balance, end of year $12,050 b. Prepare a working paper to consolidate the trial balances of Prance and Stallion. Label your eliminating entries (C), (1), (E), and (R). Enter answers in thousands ($400,000 equals $400 in thousands). Use negative signs with Cr (credit) answers in the Consolidated Balances Dr (Cr) column. Consolidated Balances Consolidation Working Paper Trial Balances Taken from Books Eliminations Prance Stallion Dr (Cr) Dr (Cr) Debit Credit $2,500 $1,500 350,000 250,000 12,050 -- (1-2) 0 Dr (Cr) (in thousands) Current assets Plant and equipment, net Investment in Stallion 0 (1-3) $ 0 0 0 (C) (E) (R) Goodwill -- Liabilities Capital stock Retained earnings, beg. (R) (353,300) (245,500) (2,000) (1,000) (E) (6,000) (4,000) (1-1) (E) (275,000) (150,000) (1-4) (1,250) -- (C) $ 200,000 90,000 (1-3) Sales revenue Equity in net income of Stallion Cost of sales 0 0 0 0 (1-1) (1-2) (1-4) Operating expenses 73,000 59,000 $-- $-- HA 0 $ 0 $ (in thousands) Current assets Plant and equipment, net Investment in Stallion Liabilities Capital stock Retained earnings, beginning Sales revenue Prance Stallion Dr (Cr) Dr (Cr) $2,500 $1,500 350,000 250,000 12,050 (353,300) (245,500) (2,000) (1,000) (6,000) (4,000) (275,000) (150,000) (1,250) 200,000 90,000 73,000 59,000 $0 $0 Equity in net income Cost of sales Operating expenses Total Required $ (in thousands) Stallion's reported income Confirmed profit in beginning inventory Unconfirmed profit in ending inventory Equity in net income 400 600 250 $1,250 0 (in thousands) Acquisition cost Change in book value to the beginning of the year Goodwill write-off to the beginning of the year Unconfirmed profit in last year's ending inventory ding inventory Investment balance, beginning of year Equity in net income, current year Investment balance, end of year $12,050 b. Prepare a working paper to consolidate the trial balances of Prance and Stallion. Label your eliminating entries (C), (1), (E), and (R). Enter answers in thousands ($400,000 equals $400 in thousands). Use negative signs with Cr (credit) answers in the Consolidated Balances Dr (Cr) column. Consolidated Balances Consolidation Working Paper Trial Balances Taken from Books Eliminations Prance Stallion Dr (Cr) Dr (Cr) Debit Credit $2,500 $1,500 350,000 250,000 12,050 -- (1-2) 0 Dr (Cr) (in thousands) Current assets Plant and equipment, net Investment in Stallion 0 (1-3) $ 0 0 0 (C) (E) (R) Goodwill -- Liabilities Capital stock Retained earnings, beg. (R) (353,300) (245,500) (2,000) (1,000) (E) (6,000) (4,000) (1-1) (E) (275,000) (150,000) (1-4) (1,250) -- (C) $ 200,000 90,000 (1-3) Sales revenue Equity in net income of Stallion Cost of sales 0 0 0 0 (1-1) (1-2) (1-4) Operating expenses 73,000 59,000 $-- $-- HA 0 $ 0 $