Create the same information with columns representing time and rows representing spot and futures market. Explain your numbers now. Now verify that the profit obtained in both cases equals the amount of mispricing without the transaction cost.

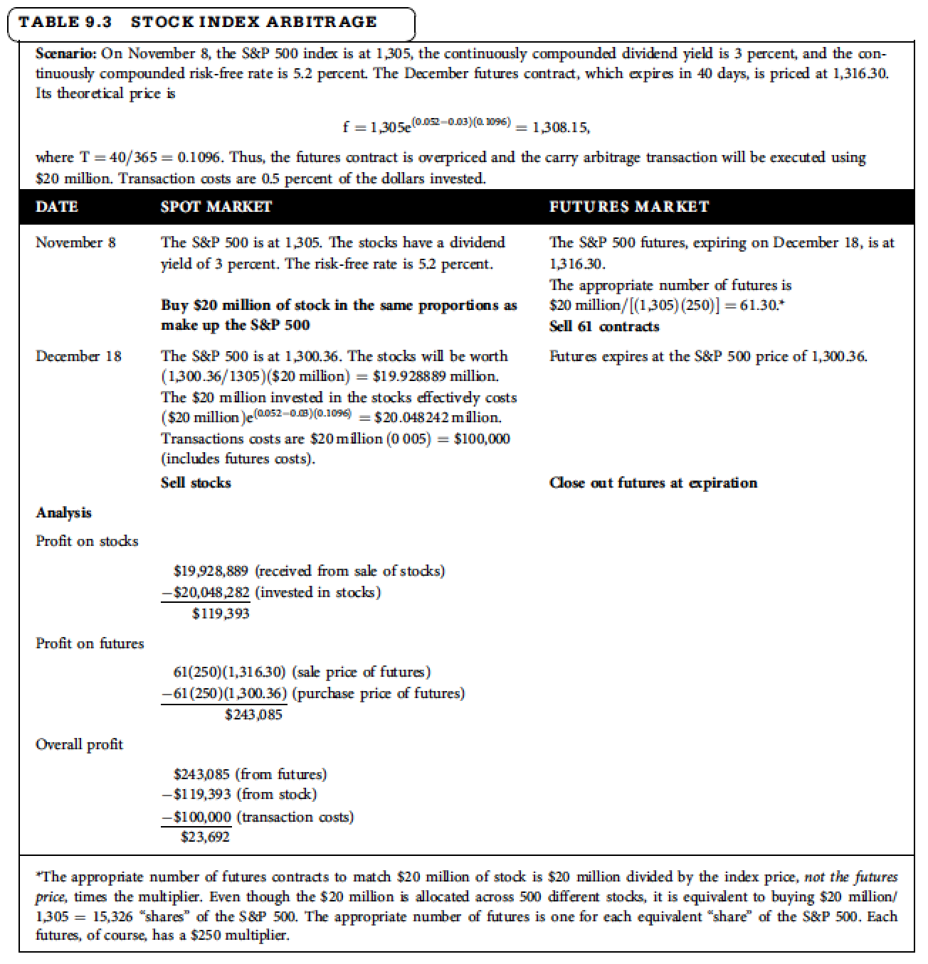

TABLE 9.3 STOCK INDEX ARBITRAGE Scenario: On November 8, the S&P 500 index is at 1,305, the continuously compounded dividend yield is 3 percent, and the con- tinuously compounded risk-free rate is 5.2 percent. The December futures contract, which expires in 40 days, is priced at 1,316.30. Its theoretical price is f=1,305 (0.02-0.03)( 1096) = 1,308.15, where T = 40/365 = 0.1096. Thus, the futures contract is overpriced and the carry arbitrage transaction will be executed using $20 million. Transaction costs are 0.5 percent of the dollars invested. DATE SPOT MARKET FUTURES MARKET November 8 The S&P 500 is at 1,305. The stocks have a dividend yield of 3 percent. The risk-free rate is 5.2 percent. The S&P 500 futures, expiring on December 18, is at 1,316.30. The appropriate number of futures is $20 million/(1,305) (250)] = 61.30.* Sell 6l contracts Futures expires at the S&P 500 price of 1,300.36. December 18 Buy $20 million of stock in the same proportions as make up the S&P 500 The S&P 500 is at 1,300.36. The stocks will be worth (1,300.36/1305)($20 million) = $19.928889 million, The $20 million invested in the stocks effectively costs ($20 million )e(0.05-0.63)(0.1096) = $20.048242 million. Transactions costs are $20 million (0 005) = $100,000 (includes futures costs). Sell stocks Close out futures at expiration Analysis Profit on stocks $19,928,889 (received from sale of stocks) - $20,048,282 (invested in stocks) $119,393 Profit on futures 61(250)(1,316.30) (sale price of futures) -61(250)(1,300.36) (purchase price of futures) $243,085 Overall profit $243,085 (from futures) -$1 19,393 (from stock) -$100,000 (transaction costs) $23,692 *The appropriate number of futures contracts to match $20 milion of stock is $20 million divided by the index price, not the futures price, times the multiplier. Even though the $20 million is allocated across 500 different stocks, it is equivalent to buying $20 million/ 1,305 = 15,326 shares of the S&P 500. The appropriate number of futures is one for each equivalent "share of the S&P 500. Each futures, of course, has a $250 multiplier. TABLE 9.3 STOCK INDEX ARBITRAGE Scenario: On November 8, the S&P 500 index is at 1,305, the continuously compounded dividend yield is 3 percent, and the con- tinuously compounded risk-free rate is 5.2 percent. The December futures contract, which expires in 40 days, is priced at 1,316.30. Its theoretical price is f=1,305 (0.02-0.03)( 1096) = 1,308.15, where T = 40/365 = 0.1096. Thus, the futures contract is overpriced and the carry arbitrage transaction will be executed using $20 million. Transaction costs are 0.5 percent of the dollars invested. DATE SPOT MARKET FUTURES MARKET November 8 The S&P 500 is at 1,305. The stocks have a dividend yield of 3 percent. The risk-free rate is 5.2 percent. The S&P 500 futures, expiring on December 18, is at 1,316.30. The appropriate number of futures is $20 million/(1,305) (250)] = 61.30.* Sell 6l contracts Futures expires at the S&P 500 price of 1,300.36. December 18 Buy $20 million of stock in the same proportions as make up the S&P 500 The S&P 500 is at 1,300.36. The stocks will be worth (1,300.36/1305)($20 million) = $19.928889 million, The $20 million invested in the stocks effectively costs ($20 million )e(0.05-0.63)(0.1096) = $20.048242 million. Transactions costs are $20 million (0 005) = $100,000 (includes futures costs). Sell stocks Close out futures at expiration Analysis Profit on stocks $19,928,889 (received from sale of stocks) - $20,048,282 (invested in stocks) $119,393 Profit on futures 61(250)(1,316.30) (sale price of futures) -61(250)(1,300.36) (purchase price of futures) $243,085 Overall profit $243,085 (from futures) -$1 19,393 (from stock) -$100,000 (transaction costs) $23,692 *The appropriate number of futures contracts to match $20 milion of stock is $20 million divided by the index price, not the futures price, times the multiplier. Even though the $20 million is allocated across 500 different stocks, it is equivalent to buying $20 million/ 1,305 = 15,326 shares of the S&P 500. The appropriate number of futures is one for each equivalent "share of the S&P 500. Each futures, of course, has a $250 multiplier