Answered step by step

Verified Expert Solution

Question

1 Approved Answer

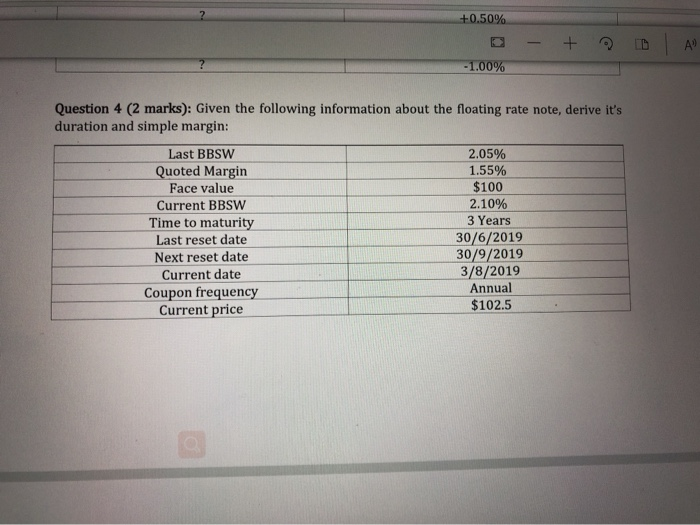

derive duration and simple margin +0.50% - B AR -1.00% Question 4 (2 marks): Given the following information about the floating rate note, derive it's

derive duration and simple margin

+0.50% - B AR -1.00% Question 4 (2 marks): Given the following information about the floating rate note, derive it's duration and simple margin: Last BBSW 2.05% Quoted Margin 1.55% Face value $100 Current BBSW 2.10% Time to maturity 3 Years Last reset date 30/6/2019 Next reset date 30/9/2019 Current date 3/8/2019 Annual Coupon frequency Current price $102.5 +0.50% - B AR -1.00% Question 4 (2 marks): Given the following information about the floating rate note, derive it's duration and simple margin: Last BBSW 2.05% Quoted Margin 1.55% Face value $100 Current BBSW 2.10% Time to maturity 3 Years Last reset date 30/6/2019 Next reset date 30/9/2019 Current date 3/8/2019 Annual Coupon frequency Current price $102.5 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations Of Finance The Logic And Practice Of Finance Management

Authors: Arthur J. Keown, John H. Martin, David F. Scott, John Petty, J. William Petty

5th Edition

0132019299, 9780132019293