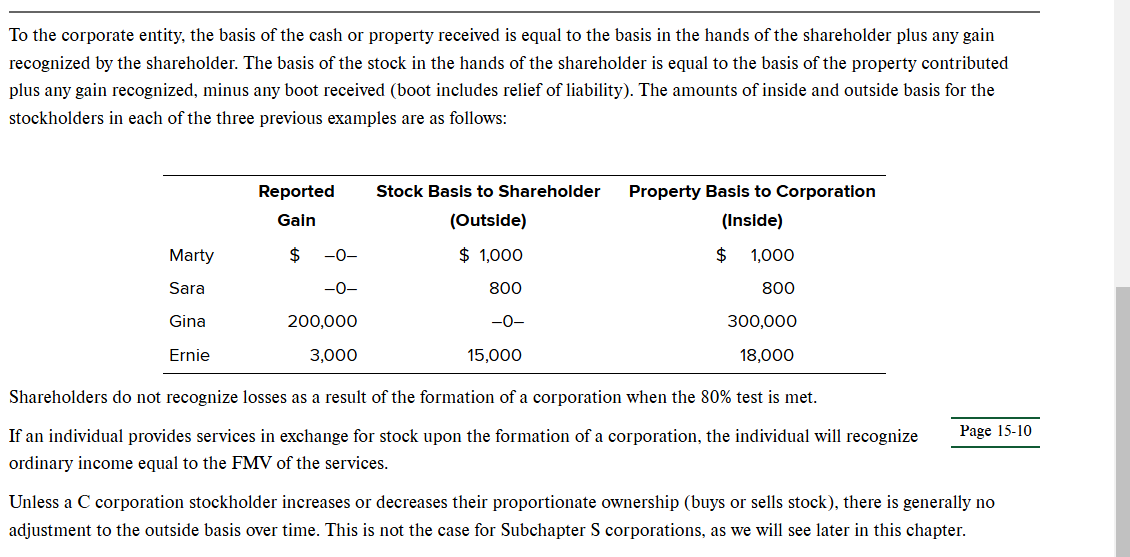

Question

Determine taxable income in each of the following instances. Assume that the corporation is a C corporation and that book income is before any income

Determine taxable income in each of the following instances. Assume that the corporation is a C corporation and that book income is before any income tax expense. Required: Book income of $61,000 including capital gains of $6,000, a charitable contribution of $1,600, and meals expenses of $8,500. Book income of $103,000 including capital losses of $7,000, a charitable contribution of $14,200, and meals expenses of $2,000. Book income of $87,000 including municipal bond interest of $2,000, a charitable contribution of $5,100, and dividends of $3,200 from a 10% owned domestic corporation. The corporation also has an $7,000 charitable contribution carryover. Book income of $140,000 including municipal bond interest of $1,700, a charitable contribution of $4,000, and dividends of $6,500 from a 70% owned domestic corporation. The corporation has a capital loss carryover of $5,000 and a capital gain of $2,000 in the current year.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Jeffrey Waybright, Robert Kemp, Sherif Elbarrad

2nd Canadian edition

133375536, 9780133845396, 133845397, 978-0133375534