Answered step by step

Verified Expert Solution

Question

1 Approved Answer

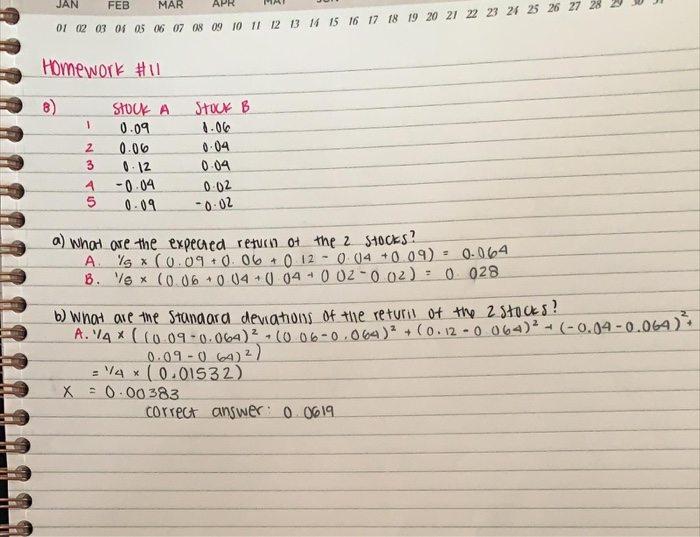

did i do this right? 29 30 JAN FEB MAR APR MAI 2 03 05 05 06 07 08 09 10 11 12 13 14

did i do this right?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Futures and Options Markets

Authors: John C. Hull

8th edition

978-1292155036, 1292155035, 132993341, 978-0132993340