Answered step by step

Verified Expert Solution

Question

1 Approved Answer

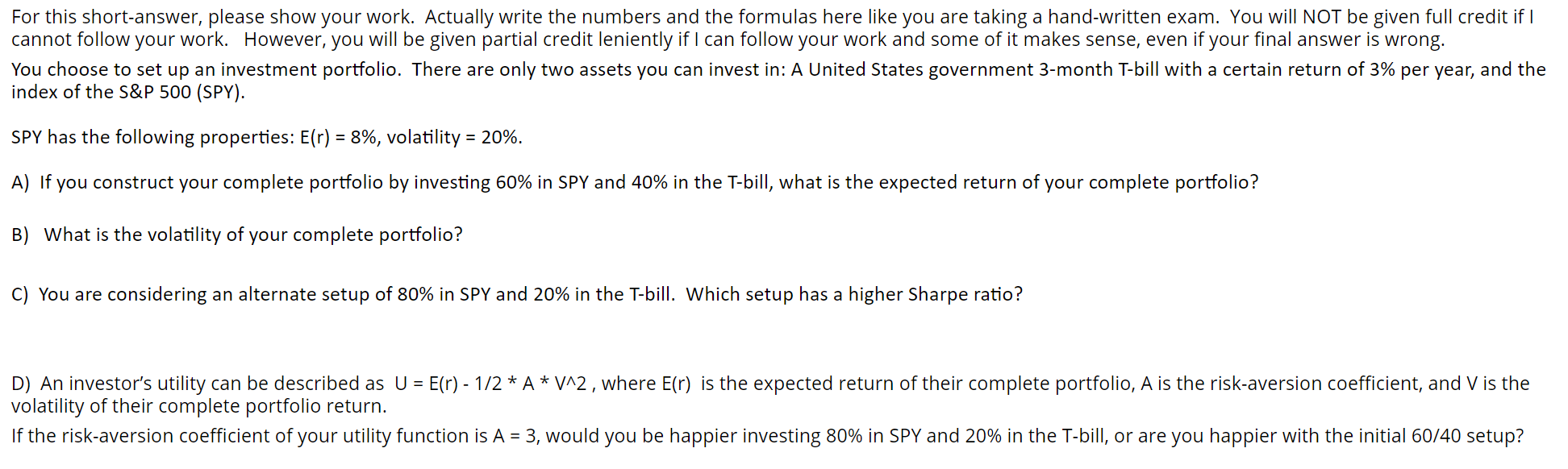

For this short-answer, please show your work. Actually write the numbers and the formulas here like you are taking a hand-written exam. You will NOT

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Capital Ideas The IMF And The Rise Of Financial Liberalization

Authors: Jeffrey M. Chwieroth

1st Edition

1789732468, 9781789732467