Answered step by step

Verified Expert Solution

Question

1 Approved Answer

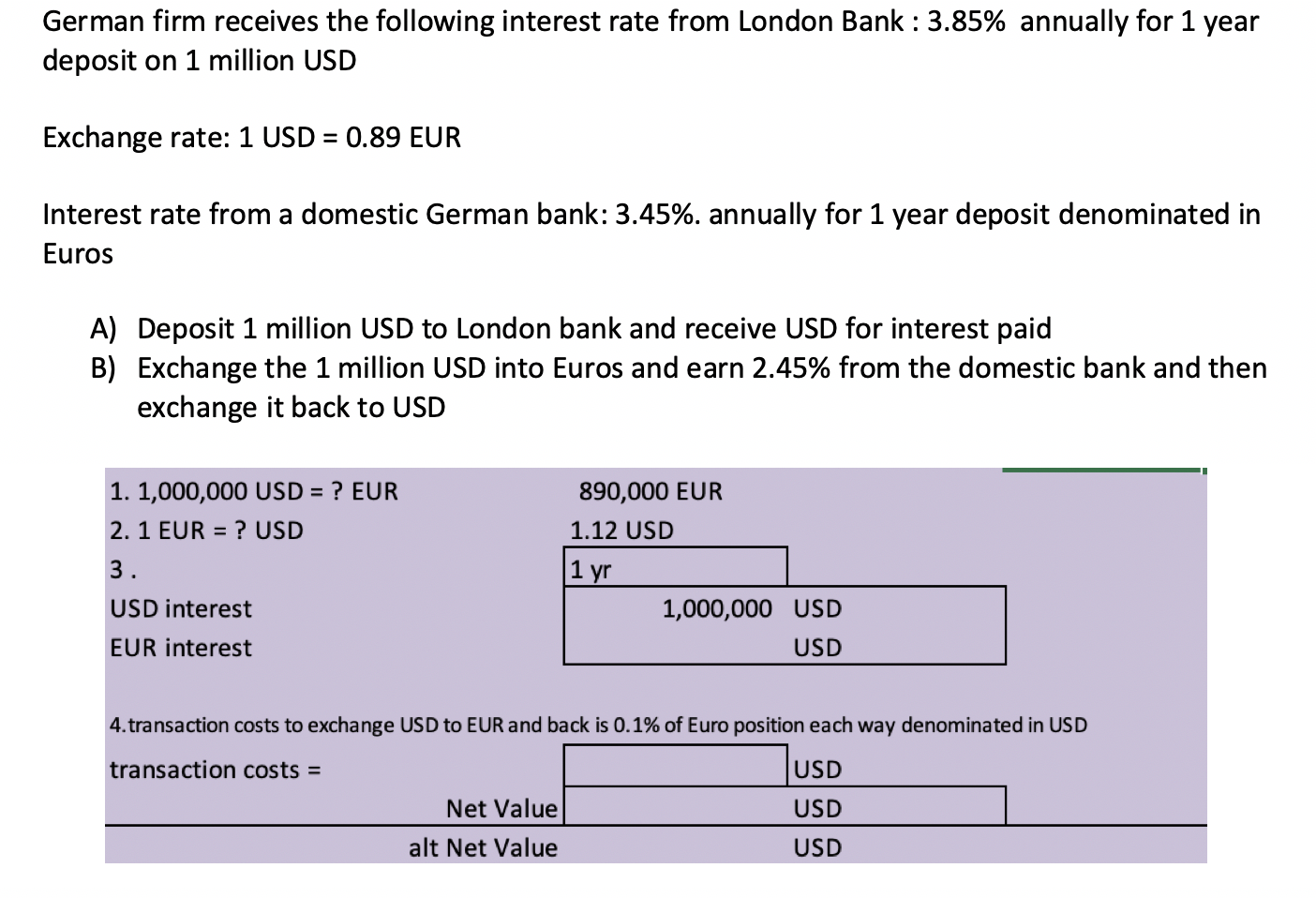

German firm receives the following interest rate from London Bank: 3.85% annually for 1 year deposit on 1 million USD Exchange rate: 1 USD =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Econometric Modelling Of Financial Time Series

Authors: Terence C. Mills, Raphael N. Markellos

3rd Edition

052171009X, 1107714125, 9780521710091, 9781107714120