Answered step by step

Verified Expert Solution

Question

1 Approved Answer

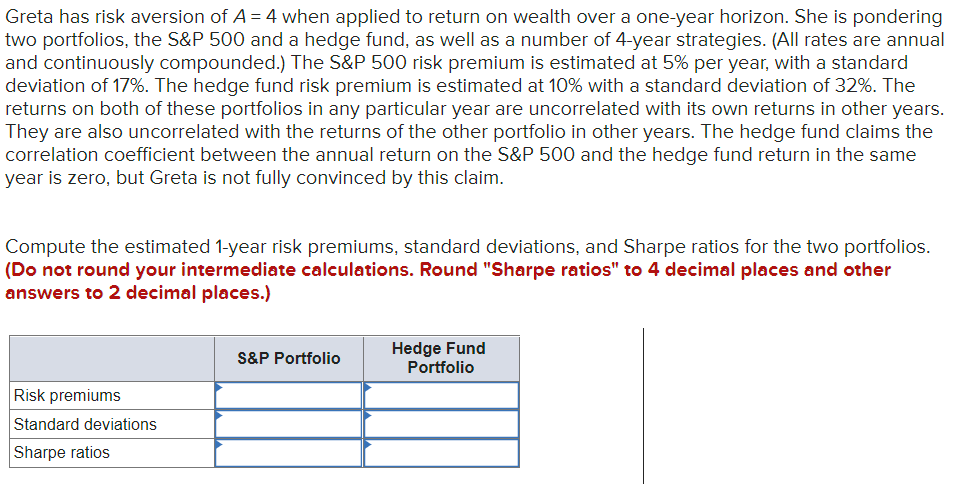

Greta has risk aversion of A=4 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Credit Derivatives Handbook Global Perspectives Innovations And Market Drivers

Authors: Greg Gregoriou, Paul Ali

1st Edition

0071549528, 978-0071549523