Answered step by step

Verified Expert Solution

Question

1 Approved Answer

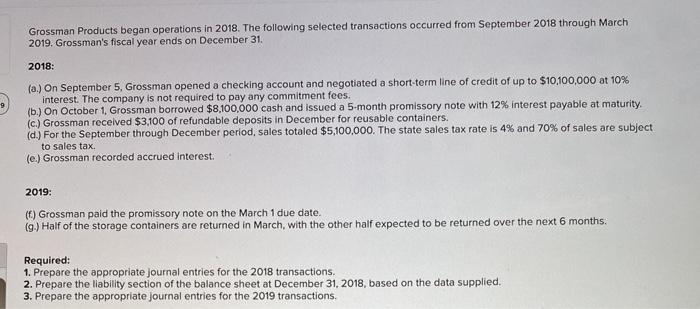

Grossman Products began operations in 2018. The following selected transactions occurred from September 2018 through March 2019. Grossman's fiscal year ends on December 31. 2018:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Role Of The Commissioner In Audit Findings Of A National Survey Of Commissioning Authorities In England Evaluating Medical Audit

Authors: Moira, Rumsey

1st Edition

1898845026, 978-1898845027