Answered step by step

Verified Expert Solution

Question

1 Approved Answer

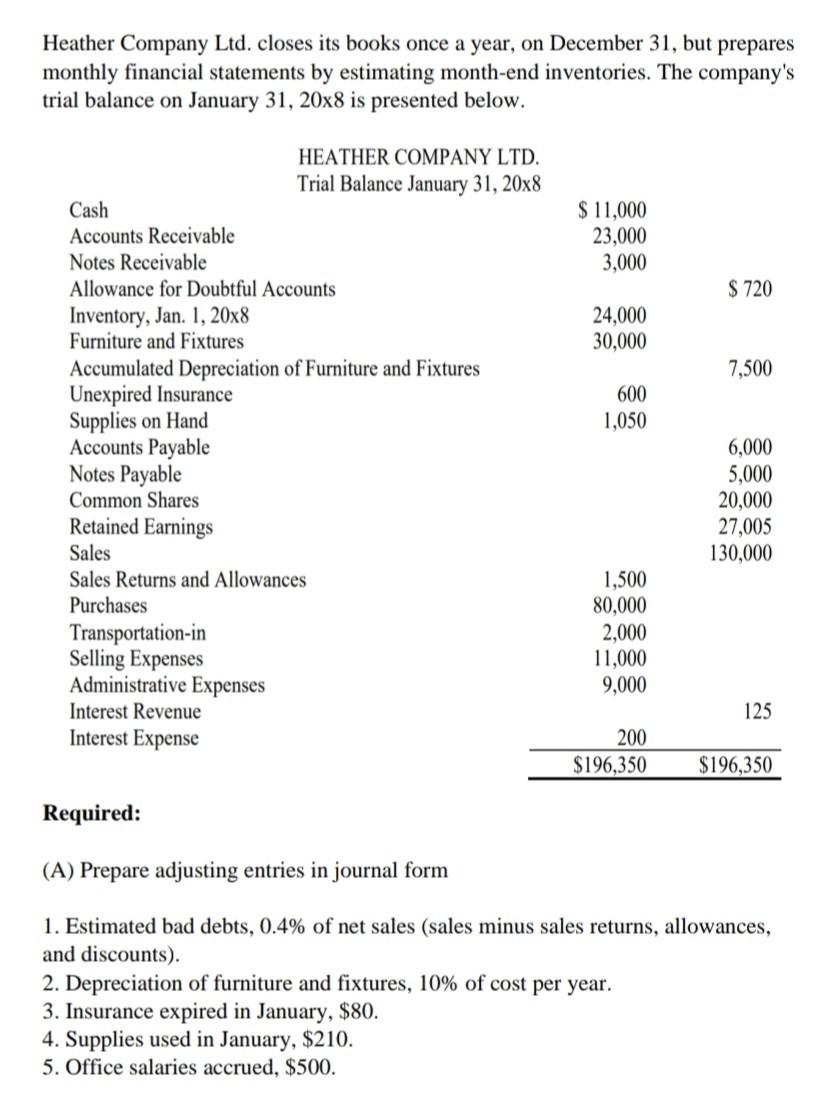

Heather Company Ltd. closes its books once a year, on December 31, but prepares monthly financial statements by estimating month-end inventories. The company's trial balance

Heather Company Ltd. closes its books once a year, on December 31, but prepares monthly financial statements by estimating month-end inventories. The company's trial balance on January \\( 31,20 \\times 8 \\) is presented below. Required: (A) Prepare adjusting entries in journal form 1. Estimated bad debts, \0.4 of net sales (sales minus sales returns, allowances, and discounts). 2. Depreciation of furniture and fixtures, \10 of cost per year. 3. Insurance expired in January, \\( \\$ 80 \\). 4. Supplies used in January, \\$210. 5. Office salaries accrued, \\( \\$ 500 \\). 6. Interest accrued on notes payable, \\( \\$ 200 \\). 7. Interest received but unearned on notes receivable, \\( \\$ 75 \\). 8. Estimate the January 31 inventory and record the adjusting entry. The average gross profit earned by the company is \30 of net sales. The gross profit rate equals net sales minus cost of goods sold divided by net sales. Prepare the following: 1. Open all t-accounts and complete your posting of journal entries into taccounts. 2. Prepare adjusted trial balance 3. Prepare Statement of Financial Position 4. Prepare Income Statement, and 5. Prepare Statement of Changes in Shareholders' Equity. Dividends of \\( \\$ 3,000 \\) were declared and paid on the common shares during the month

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ESG And Financial Performance The Effects Of Audit Quality And National Culture In The Nigerian And Kenyan Context

Authors: Ursule Yvanna Otek Ntsama

1st Edition

3346838838, 978-3346838834