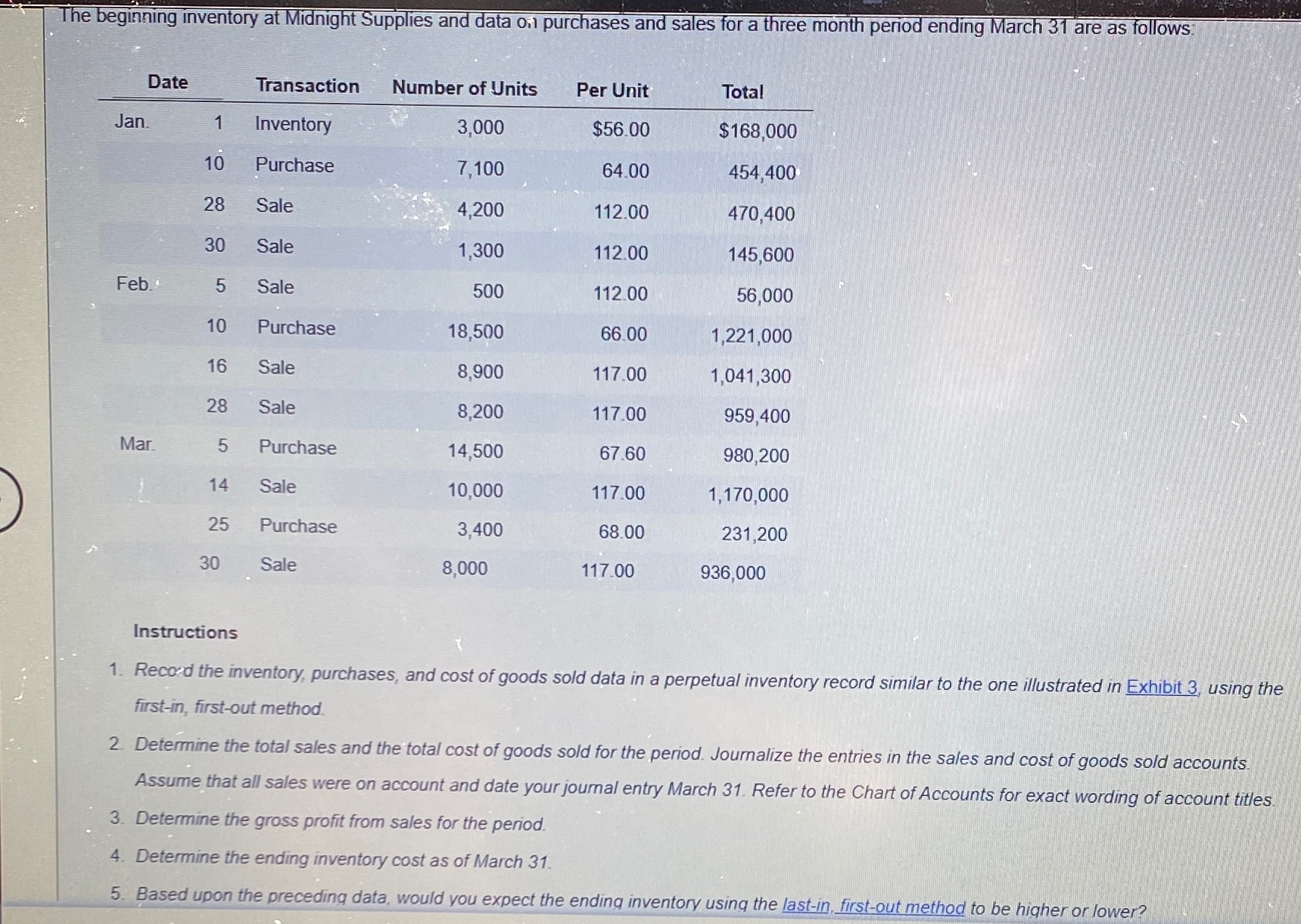

Question

Help needed on FIFO, journal, and final questions. The final questions are: 1. Determine the gross profit from sales for the period $_____________. 2. Determine

Help needed on FIFO, journal, and final questions. The final questions are: 1. "Determine the gross profit from sales for the period $_____________." 2. "Determine the ending inventory cost as of March 31 $_____________."

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Cost Accounting

Authors: William N. Lanen, Shannon Anderson, Michael W Maher

6th edition

1259969479, 1259565408, 978-1259969478