Answered step by step

Verified Expert Solution

Question

1 Approved Answer

How do i solve for this and what excel formula should i use You are finally able to invest in the stock market. You know

How do i solve for this and what excel formula should i use

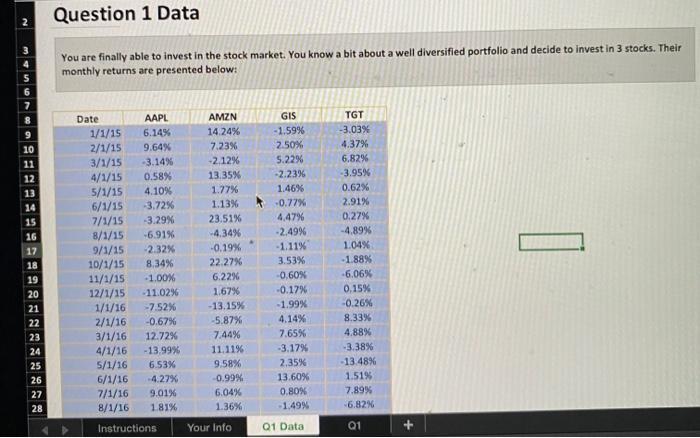

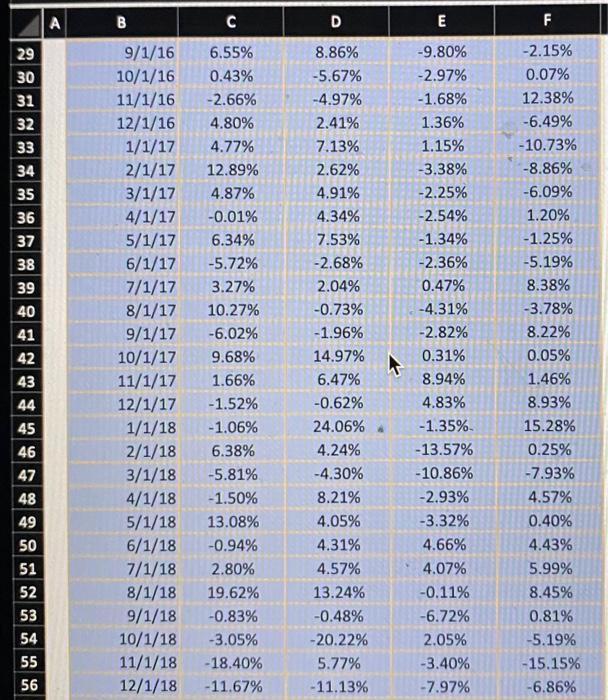

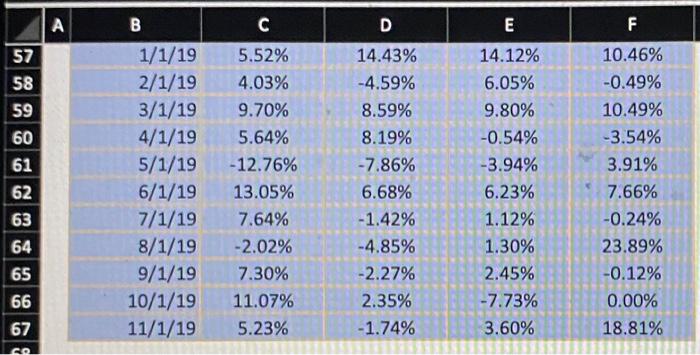

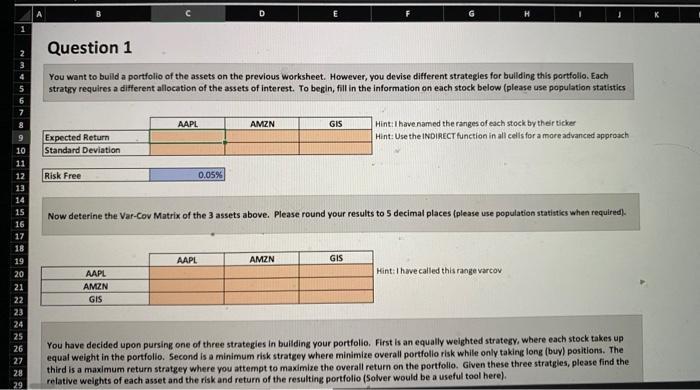

You are finally able to invest in the stock market. You know a bit about a well diversified portfolio and decide to invest in 3 stocks. Their monthly returns are presented below: You want to build a portfolio of the assets on the previous worksheet. However, you devise different strategles for bullding this portfolio. Each stratiy requires a different allocation of the assets of interest. To begin, fill in the information on each stock below (please use population statistics Hint:I have named the ranges of each stoci by their ticker Hint: Use the NDIRECT function in alk celisfor a more advanced approach \begin{tabular}{|l|l|} \hline Risk Free & 0.05% \\ \hline \end{tabular} Now deterine the Var-Cov Matrix of the 3 assets above. Please round your results to 5 decimal places (please use population statistics when required). Hint: I have called this range varcov You have decided upon pursing one of three strategies in building your portfolio. First is an equally weighted strategy, where each stock takes up equal weight in the portfolio. Second is a minimum risk stratgey where minimize overall portfollo risk while only taking long (buy) positions. The third is a maximum return stratgey where you attempt to maximire the overall return on the portfollo. Given these three stratgies, please find the relative weights of each asset and the risk and return of the resulting portfolio (Solver would be a useful tool here). You are finally able to invest in the stock market. You know a bit about a well diversified portfolio and decide to invest in 3 stocks. Their monthly returns are presented below: You want to build a portfolio of the assets on the previous worksheet. However, you devise different strategles for bullding this portfolio. Each stratiy requires a different allocation of the assets of interest. To begin, fill in the information on each stock below (please use population statistics Hint:I have named the ranges of each stoci by their ticker Hint: Use the NDIRECT function in alk celisfor a more advanced approach \begin{tabular}{|l|l|} \hline Risk Free & 0.05% \\ \hline \end{tabular} Now deterine the Var-Cov Matrix of the 3 assets above. Please round your results to 5 decimal places (please use population statistics when required). Hint: I have called this range varcov You have decided upon pursing one of three strategies in building your portfolio. First is an equally weighted strategy, where each stock takes up equal weight in the portfolio. Second is a minimum risk stratgey where minimize overall portfollo risk while only taking long (buy) positions. The third is a maximum return stratgey where you attempt to maximire the overall return on the portfollo. Given these three stratgies, please find the relative weights of each asset and the risk and return of the resulting portfolio (Solver would be a useful tool here)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investing From Scratch A Handbook For The Young Investor

Authors: James Lowell

1st Edition

014303684X, 978-0143036845