Answered step by step

Verified Expert Solution

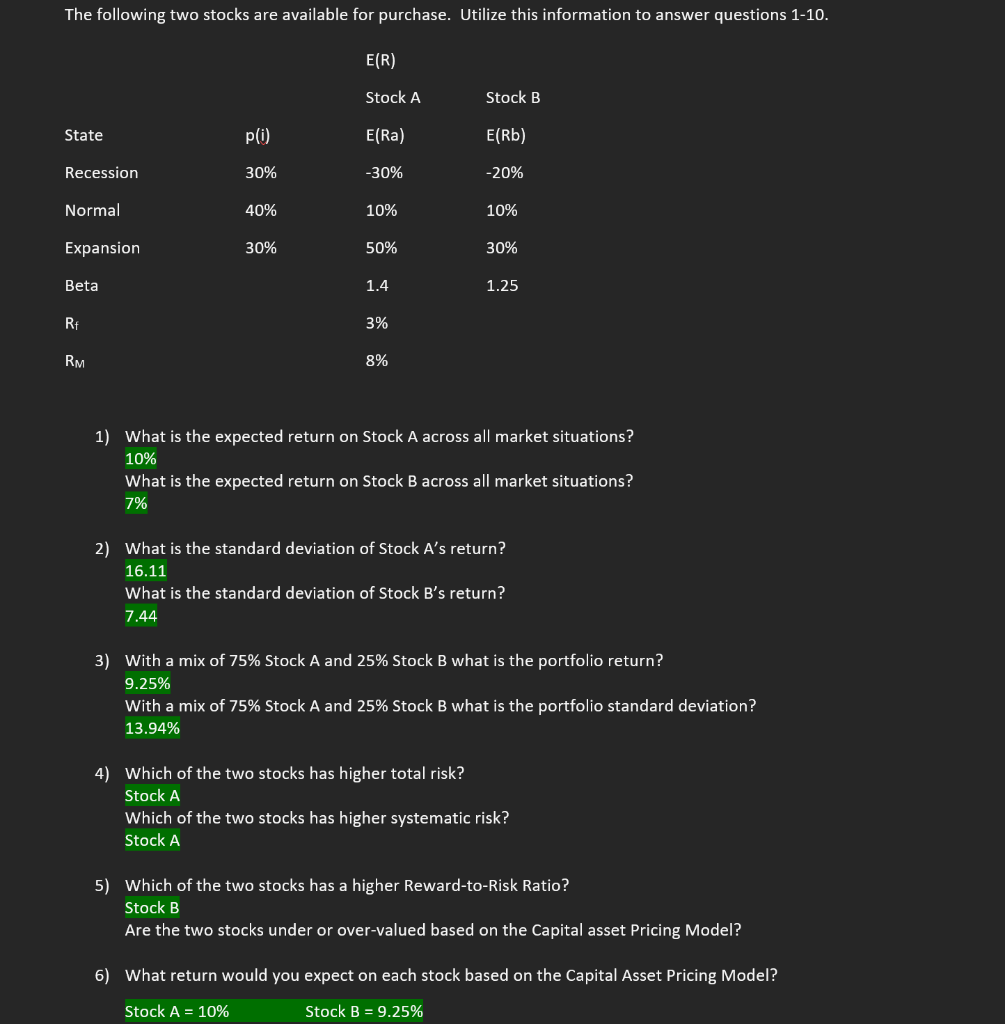

Question

1 Approved Answer

I just need the second part to question 5 answered. And can you check my work to see if I answered the rest of the

I just need the second part to question 5 answered. And can you check my work to see if I answered the rest of the questions correctly, please? Thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Analysis For Management

Authors: Barry Render, Ralph M. Stair, Michael E. Hanna, Trevor S. Hale

14th Edition

0137943601, 9780137943609