Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I know the question is a bit long. I will give you a really good rate!!! Suppose asset returns are driven by two common factors,

I know the question is a bit long. I will give you a really good rate!!!

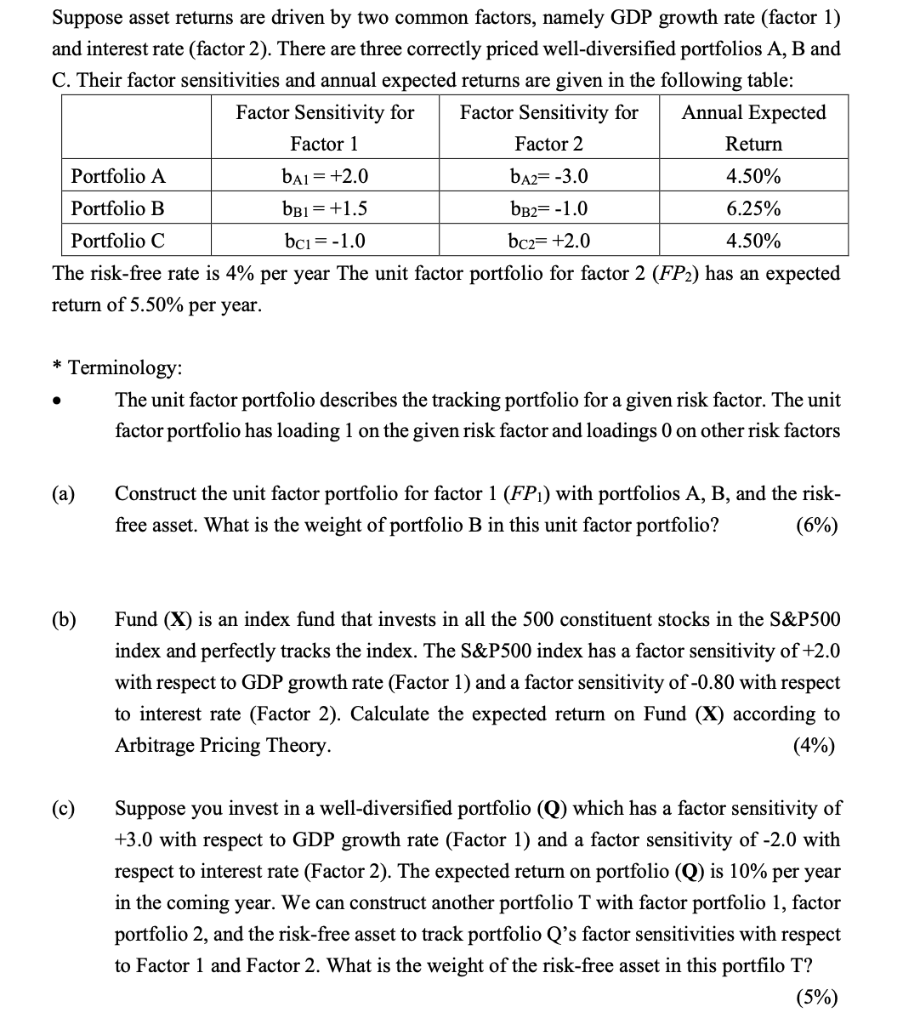

Suppose asset returns are driven by two common factors, namely GDP growth rate (factor 1) and interest rate (factor 2). There are three correctly priced well-diversified portfolios A, B and C. Their factor sensitivities and annual expected returns are given in the following table: Factor Sensitivity for Factor Sensitivity for Annual Expected Factor 1 Factor 2 Return Portfolio A bai= +2.0 b^2= -3.0 4.50% Portfolio B bb1 = +1.5 bb2=-1.0 6.25% Portfolio C bci=-1.0 bc2= +2.0 4.50% The risk-free rate is 4% per year The unit factor portfolio for factor 2 (FP2) has an expected return of 5.50% per year. * Terminology: The unit factor portfolio describes the tracking portfolio for a given risk factor. The unit factor portfolio has loading 1 on the given risk factor and loadings 0 on other risk factors (a) Construct the unit factor portfolio for factor 1 (FP1) with portfolios A, B, and the risk- free asset. What is the weight of portfolio B in this unit factor portfolio? (6%) (b) Fund (X) is an index fund that invests in all the 500 constituent stocks in the S&P500 index and perfectly tracks the index. The S&P500 index has a factor sensitivity of +2.0 with respect to GDP growth rate (Factor 1) and a factor sensitivity of -0.80 with respect to interest rate (Factor 2). Calculate the expected return on Fund (X) according to Arbitrage Pricing Theory. (4%) (c) Suppose you invest in a well-diversified portfolio (Q) which has a factor sensitivity of +3.0 with respect to GDP growth rate (Factor 1) and a factor sensitivity of -2.0 with respect to interest rate (Factor 2). The expected return on portfolio (Q) is 10% per year in the coming year. We can construct another portfolio T with factor portfolio 1, factor portfolio 2, and the risk-free asset to track portfolio Qs factor sensitivities with respect to Factor 1 and Factor 2. What is the weight of the risk-free asset in this portfilo T? (5%) Suppose asset returns are driven by two common factors, namely GDP growth rate (factor 1) and interest rate (factor 2). There are three correctly priced well-diversified portfolios A, B and C. Their factor sensitivities and annual expected returns are given in the following table: Factor Sensitivity for Factor Sensitivity for Annual Expected Factor 1 Factor 2 Return Portfolio A bai= +2.0 b^2= -3.0 4.50% Portfolio B bb1 = +1.5 bb2=-1.0 6.25% Portfolio C bci=-1.0 bc2= +2.0 4.50% The risk-free rate is 4% per year The unit factor portfolio for factor 2 (FP2) has an expected return of 5.50% per year. * Terminology: The unit factor portfolio describes the tracking portfolio for a given risk factor. The unit factor portfolio has loading 1 on the given risk factor and loadings 0 on other risk factors (a) Construct the unit factor portfolio for factor 1 (FP1) with portfolios A, B, and the risk- free asset. What is the weight of portfolio B in this unit factor portfolio? (6%) (b) Fund (X) is an index fund that invests in all the 500 constituent stocks in the S&P500 index and perfectly tracks the index. The S&P500 index has a factor sensitivity of +2.0 with respect to GDP growth rate (Factor 1) and a factor sensitivity of -0.80 with respect to interest rate (Factor 2). Calculate the expected return on Fund (X) according to Arbitrage Pricing Theory. (4%) (c) Suppose you invest in a well-diversified portfolio (Q) which has a factor sensitivity of +3.0 with respect to GDP growth rate (Factor 1) and a factor sensitivity of -2.0 with respect to interest rate (Factor 2). The expected return on portfolio (Q) is 10% per year in the coming year. We can construct another portfolio T with factor portfolio 1, factor portfolio 2, and the risk-free asset to track portfolio Qs factor sensitivities with respect to Factor 1 and Factor 2. What is the weight of the risk-free asset in this portfilo T? (5%)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Treasury And Cash Management

Authors: Robert Cooper

1st Edition

1349512699, 9781349512690