Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need help summerizing each section: Facts(Summerize the important facts of this section, not everything just the important facts), Issue, holding, and reasoning(summerize the explantion

I need help summerizing each section: Facts(Summerize the important facts of this section, not everything just the important facts), Issue, holding, and reasoning(summerize the explantion on why the case was held, what the court thinks)

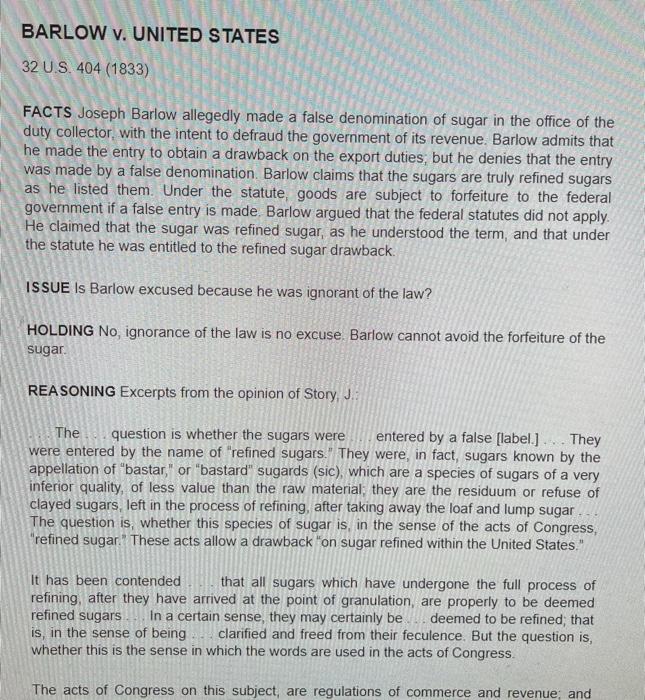

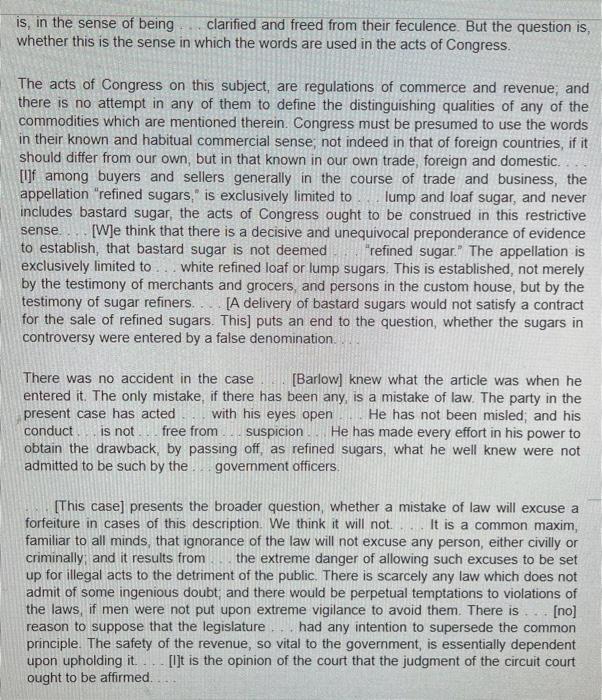

BARLOW v. UNITED STATES 32 U.S. 404 (1833) FACTS Joseph Barlow allegedly made a false denomination of sugar in the office of the duty collector, with the intent to defraud the government of its revenue. Barlow admits that he made the entry to obtain a drawback on the export duties, but he denies that the entry was made by a false denomination. Barlow claims that the sugars are truly refined sugars as he listed them. Under the statute, goods are subject to forfeiture to the federal government if a false entry is made. Barlow argued that the federal statutes did not apply. He claimed that the sugar was refined sugar, as he understood the term, and that under the statute he was entitled to the refined sugar drawback ISSUE Is Barlow excused because he was ignorant of the law? HOLDING No, ignorance of the law is no excuse Barlow cannot avoid the forfeiture of the sugar. REASONING Excerpts from the opinion of Story, J.: The question is whether the sugars were entered by a false (label.]. They were entered by the name of "refined sugars." They were, in fact, sugars known by the appellation of "bastar," or "bastard" sugards (sic), which are a species of sugars of a very inferior quality, of less value than the raw material, they are the residuum or refuse of clayed sugars, left in the process of refining, after taking away the loaf and lump sugar The question is, whether this species of sugar is, in the sense of the acts of Congress, "refined sugar." These acts allow a drawback "on sugar refined within the United States." It has been contended that all sugars which have undergone the full process of refining, after they have arrived at the point of granulation, are properly to be deemed refined sugars In a certain sense, they may certainly be deemed to be refined, that is, in the sense of being clarified and freed from their feculence. But the question is, whether this is the sense in which the words are used in the acts of Congress The acts of Congress on this subject, are regulations of commerce and revenue; and is, in the sense of being clarified and freed from their feculence. But the question is, whether this is the sense in which the words are used in the acts of Congress. The acts of Congress on this subject, are regulations of commerce and revenue; and there is no attempt in any of them to define the distinguishing qualities of any of the commodities which are mentioned therein. Congress must be presumed to use the words in their known and habitual commercial sense, not indeed in that of foreign countries, if it should differ from our own, but in that known in our own trade, foreign and domestic. [Of among buyers and sellers generally in the course of trade and business, the appellation "refined sugars," is exclusively limited to lump and loaf sugar, and never includes bastard sugar, the acts of Congress ought to be construed in this restrictive sense [W]e think that there is a decisive and unequivocal preponderance of evidence to establish, that bastard sugar is not deemed "refined sugar." The appellation is exclusively limited to white refined loaf or lump sugars. This is established, not merely by the testimony of merchants and grocers and persons in the custom house, but by the testimony of sugar refiners. [A delivery of bastard sugars would not satisfy a contract for the sale of refined sugars. This) puts an end to the question, whether the sugars in controversy were entered by a false denomination. There was no accident in the case [Barlow] knew what the article was when he entered it. The only mistake, if there has been any, is a mistake of law. The party in the present case has acted with his eyes open He has not been misled; and his conduct is not free from suspicion He has made every effort in his power to obtain the drawback, by passing off, as refined sugars, what he well knew were not admitted to be such by the government officers [This case] presents the broader question, whether a mistake of law will excuse a forfeiture in cases of this description. We think it will not. It is a common maxim, familiar to all minds that ignorance of the law will not excuse any person, either civilly or criminally, and it results from the extreme danger of allowing such excuses to be set up for illegal acts to the detriment of the public. There is scarcely any law which does not admit of some ingenious doubt; and there would be perpetual temptations to violations of the laws, if men were not put upon extreme vigilance to avoid them. There is [no] reason to suppose that the legislature had any intention to supersede the common principle. The safety of the revenue, so vital to the government, is essentially dependent upon upholding it. [I]t is the opinion of the court that the judgment of the circuit court ought to be affirmed Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit And Assurance Principles And Practices In Singapore

Authors: Dr Ernest Kan

5th Edition

9814838136, 978-9814838139