In this forum, let's apply our knowledge of product development and the diffusion process to the Sapphire brand. Analyze the factors (features, attributes, pricing) that

In this forum, let's apply our knowledge of product development and the diffusion process to the Sapphire brand.

Analyze the factors (features, attributes, pricing) that placed the Sapphire brand in a class of its own? Define the product style and compare and contrast the Sapphire style with the other brands.

What were the industry dynamics during the brand introductory phase that made this product attractive?

Since the first introduction of the Sapphire Preferred in 2009, discuss product/service extension and the underlying expansion of target segments.

Discuss the consumer adoption and diffusion process, focusing on the early adopters and the early majority.

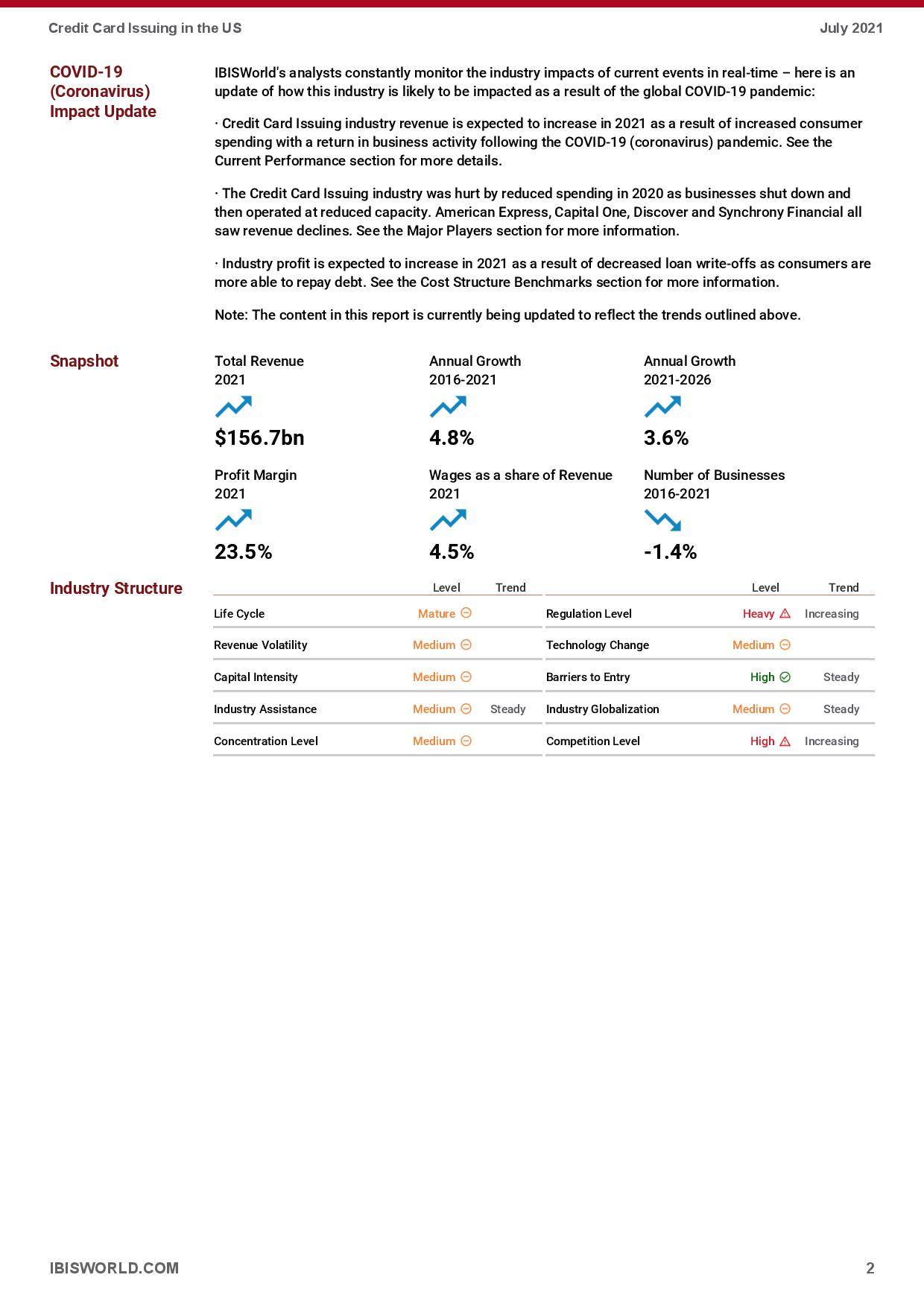

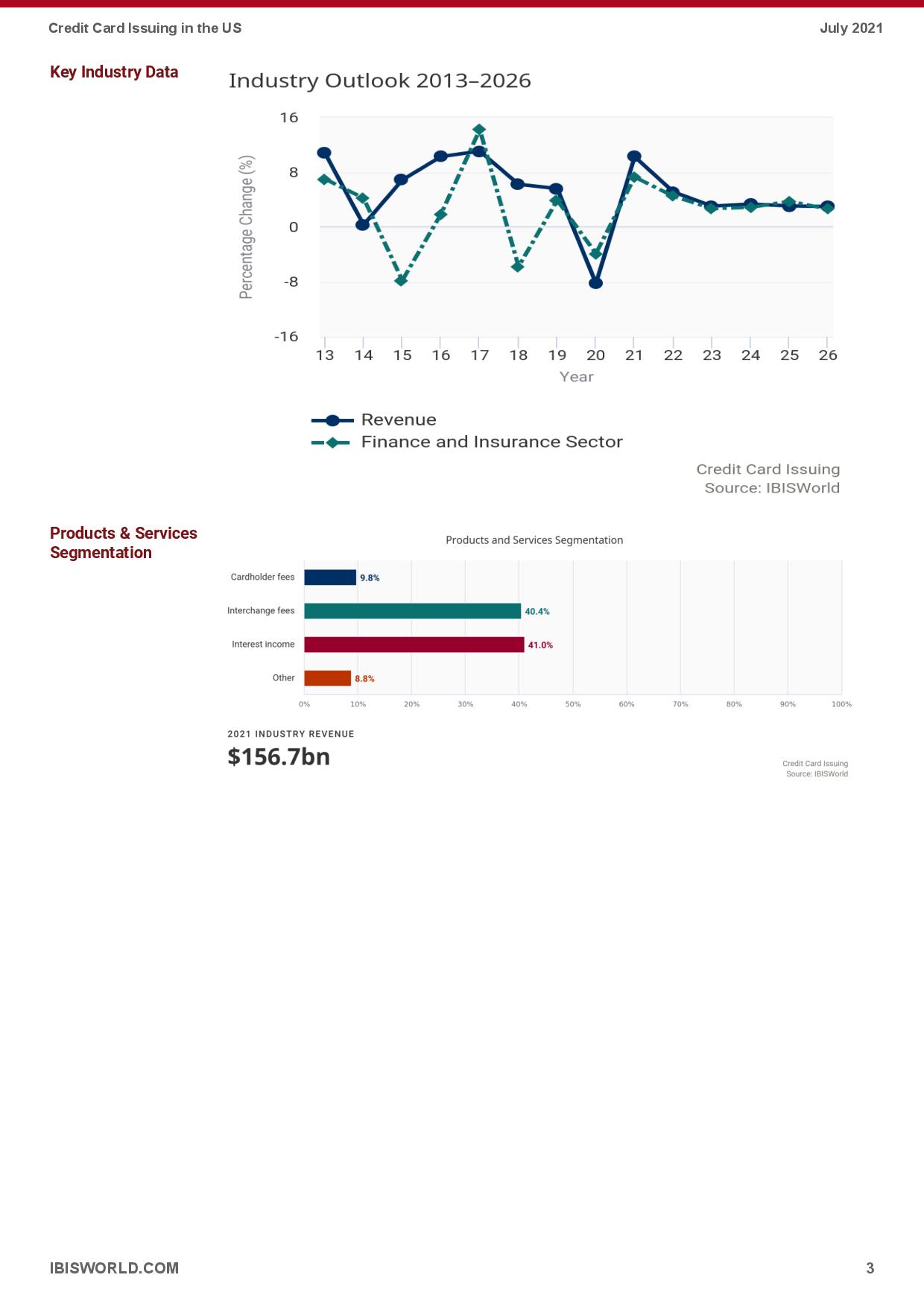

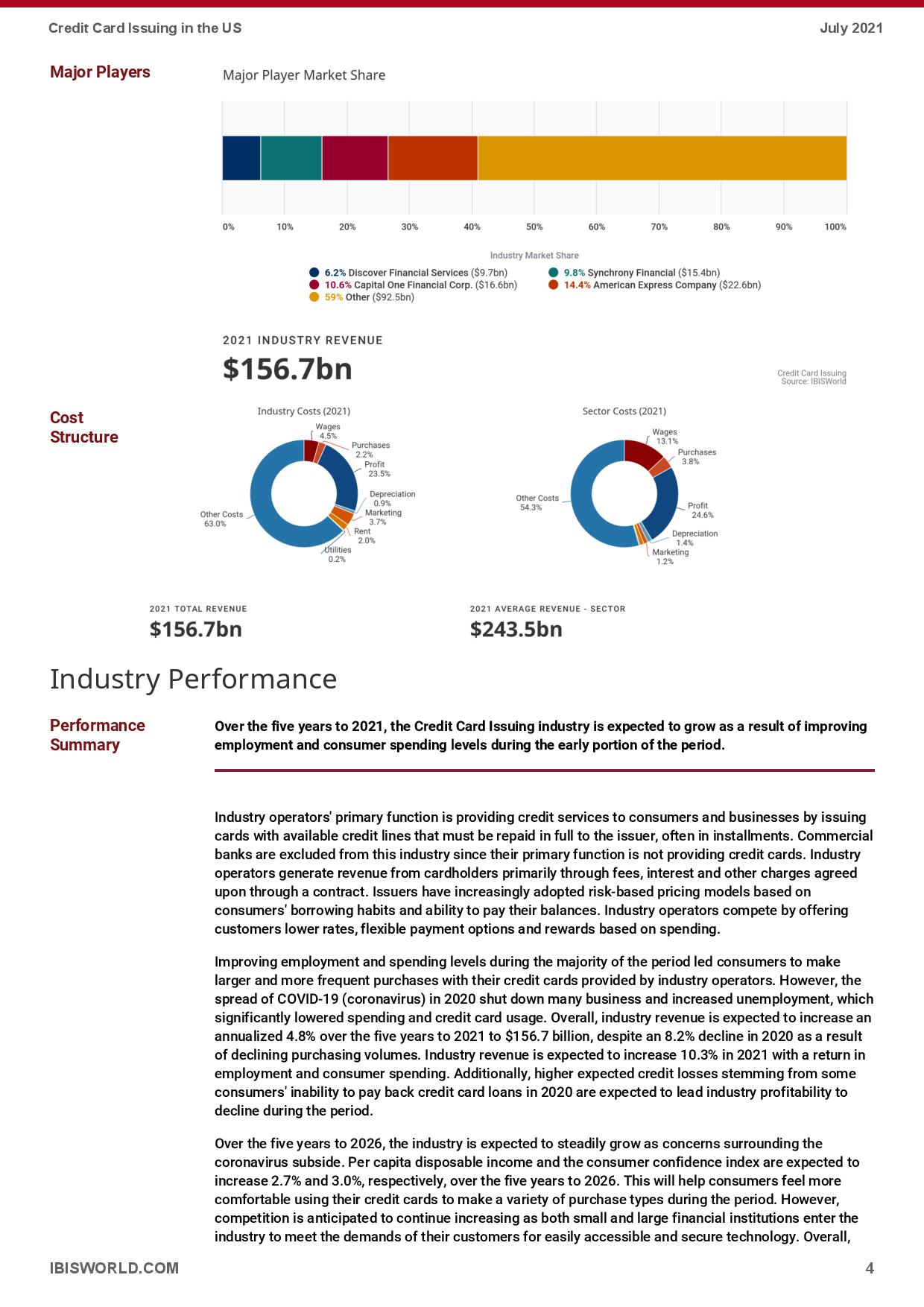

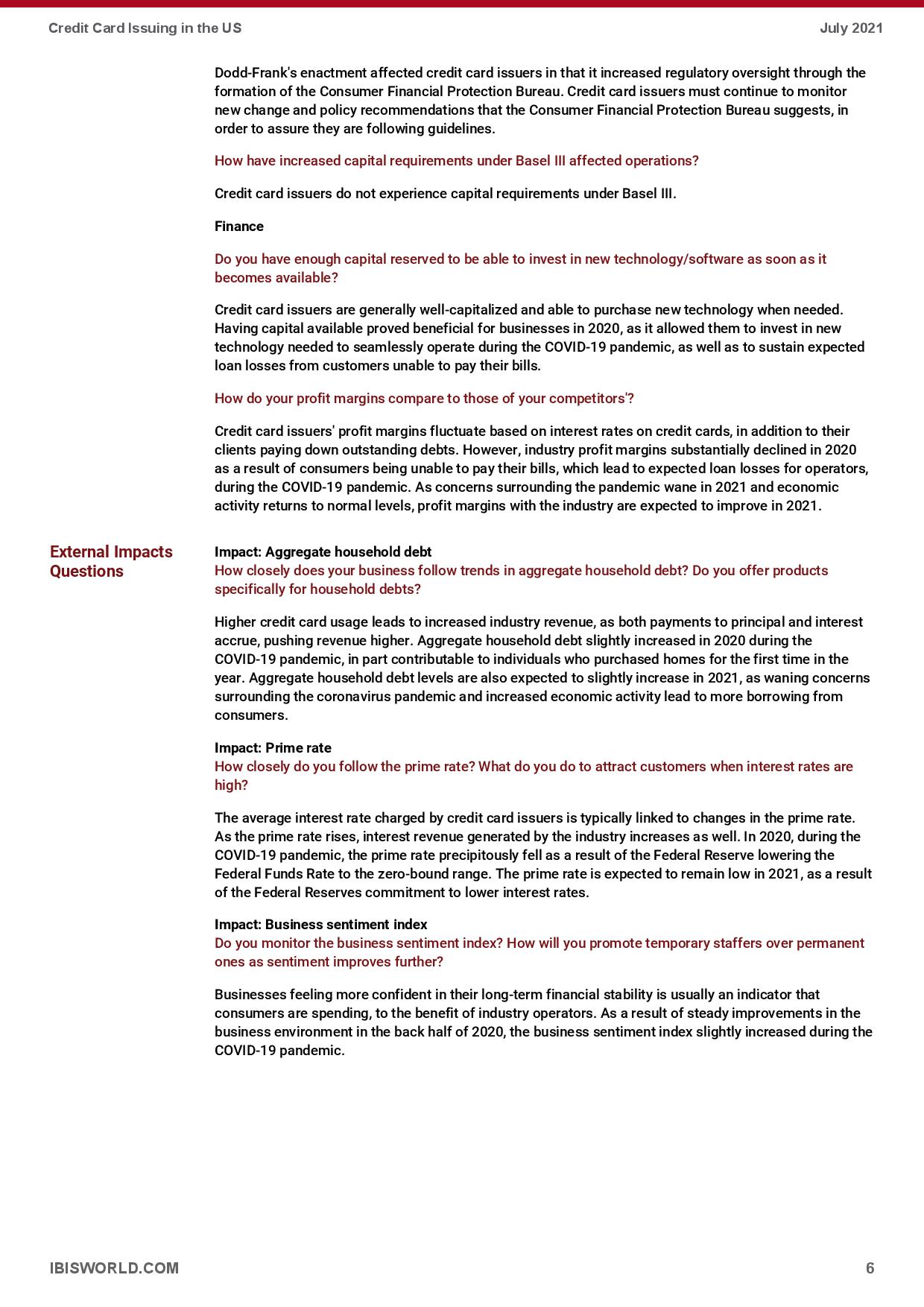

Credit Card Issuing in the US July 2021 COVlD-1 9 (Coronavirus) Impact U pdate Snapshot Industry Structure IBISWorId's analysts constantly monitor the industry impacts of current events in real-time - here is an update of how this industry is likely to be impacted as a result of the global COVID19 pandemic: - Credit Card Issuing industry revenue is expected to increase in 2021 as a result of increased consumer spending with a return in business activity following the COVlD-19 (coronavirus) pandemic. See the Current Performance section for more details. . The Credit Card Issuing industry was hurt by reduced spending in 2020 as businesses shut down and then operated at reduced capacity. American Express, Capital One, Discover and Synchrony Financial all saw revenue declines. See the Major Players section for more information. . Industry prot is expected to increase in 2021 as a result of decreased loan write-offs as consumers are more able to repay debt. See the Cost Structure Benchmarks section for more information. Note: The content in this report is currently being updated to reflect the trends outlined above. IBISWORLD.COM Total Revenue Annual Growth Annual Growth 2021 2016-2021 2021-2026 $156.7bn 4.3% 3.6% Profit Margin Wages as a share of Revenue Number of Businesses 2021 2021 2016-2021 23.5% 4.5% -1 .496 Level Trend Level Trend Life Cycle Mature 9 Regulation Level Heavy A Increasing Revenue Volatility Medium 6) Technology Change Medium 6-) Capital Intensity Medium (9 Barrier-ate Entry High Q Steady Medium (-3 Steady Medium (9 Steady Industry Assistance Concentration Level Medium ("3' Industry Globalization Competition Level High A Increasing Credit Card Issuing in the US July 2021 Key Industry Data Industry Outlook 2013-2026 16 8 Percentage Change (%) -8 -16 13 14 15 16 17 18 19 20 21 22 23 24 25 26 Year - Revenue - Finance and Insurance Sector Credit Card Issuing Source: IBISWorld Products & Services Products and Services Segmentation Segmentation Cardholder fees 9.8% Interchange fees 40.4% Interest income 41.0% Other 8.8% 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 2021 INDUSTRY REVENUE $156.7bn Credit Card Issuing Source: IBISWorld IBISWORLD.COM 3Credit Card Issuing in the US July 2021 Major Players Major Player Market Share 0' I\" 20' 3070 4095 5056 0075 70% m 9070 10096 Industry Market Share . 6.2% Discover Flnanclal Services ($9.?hn) . 9.8% Synchrony Financial [$15.4bn) . 10.696 Capital One Financial Corp. ($16.6bn) . 14.4% American Express Company (322. bn) . 59\".. other ($92.5an 2021 INDUSTRY REVENUE 56 7b er . . $ 1 ' n sglcgalglssvsv'rl indust Costs 2021 Sector Costs 2021 cost W l l l l Wages 13 1% Purchases 3.896 Stru ctu re other Costs 54.336 Pmlll Othel Casts 24.696 53.0% __ Depmcwticn ' 1.1% Marketing 1.2% 2021 YOTAL REVENUE 202! AVERAGE REVENUE - SECTOR $1 56.7bn $243.5bn Industry Performance Performance Over the five years to 2021, the Credit Card Issuing industry ls expected to grow as a result of improving Summary employment and consumer spending levels during the early portion of the period. Industry operators' primary function is providing credit services to consumers and businesses by issuing cards with available credit lines that must be repaid in full to the issuer, often in installments. Commercial banks are excluded from this industry since their primary function is not providing credit cards. Industry operators generate revenue from cardholders primarily through fees, interest and other charges agreed upon through a contact. Issuers have increasingly adopted risk-based pricing models based on consumers' borrowing habits and ability to pay their balances. Industry operators compete by offering customers lower rates, flexible payment options and rewards based on spending. Improving employment and spending levels during the majority of the period led consumers to make larger and more frequent purchases with their credit cards provided by industry operators. However, the spread of COVlD-19 (coronavirus) in 2020 shut down many business and increased unemployment, which significantly lowered spending and credit card usage. Overall, industry revenue is expected to increase an annualized 4.8% over the ve years to 2021 to $156.7 billion, despite an 8.2% decline in 2020 as a result of declining purchasing volumes. Industry revenue is expected to increase 10.3% in 2021 with a return in employment and consumer spending. Additionally, higher expected credit losses stemming from some consumers' inability to pay back credit card loans in 2020 are expected to lead industry profitability to decline during the period. Over the five years to 2026, the industry is expected to steadily grow as concerns surrounding the coronavirus subside. Per capita disposable income and the consumer confidence index are expected to increase 2.7% and 3.0%, respectively, over the ve years to 2026. This will help consumers feel more comfortable using their credit cards to make a variety of purchase types during the period. However, competition is anticipated to continue increasing as both small and large financial institutions enter the industry to meet the demands of their customers for easily accessible and secure technology. Overall, IBISWORLD.COM 4 Credit Card Issuing in the US July 2021 Industry Issues industry revenue is expected to increase an annualized 3.6% to $1 86.7 billion over the ve years to 2026. Threat Ecommeroe sales are purchases that are made by consumers and businesses over the internet. Most e- commerce transactions require a debit or credit card to make a payment needed to complete a transaction. As a result, growth in ecommerce sales tends to lead to increased demand for industry operators' services. In 2020, e-commerce sales are expected to increase, but at a much smaller rate than any previous years over the five years to 2021, posing a potential threat to the industry. Opportunity Lower unemployment rates result in a diminished risk of delinquency on outstanding credit card balances. A decline in the unemployment rate often results in greater spending through credit cards, lifting the amount of revolving credit. The national unemployment rate is expected to decrease in 2021, presenting a potential opportunity for the industry. Call Preparation Questions Role Specific Questions IBISWORLD.COM Sales & Marketing How do you emphasize the value of your company's services? Credit card companies try to emphasize the value of their services through their rewards programs and interest rates on their credit cards. Additionally, having a variety of financing options available to customers proved to be valuable during the COVlD-19 pandemic as more customers looked to extend payments due to decreasing employment levels. What media channels are you using to attract consumers and investors, if any? Credit card issuers use traditional media channels such as TV, print and the internet to attract consumers and businesses. Specifically, having a robust online marketing strategy as proved to be key to the success of many credit card companies, as more business has been conducted online during the COVlD-19 pandemic in 2020 and 2021. Strategy 8: Operations Are your operations spread across the country or are your establishments more concentrated in a certain geographic location? Credit card issuers are starting to consolidate their operations and limit the geographic reach of their operations to safeguard client information. This has proved beneficial during the COVlD-19 pandemic as it is easier to manage the social distancing requirements in one single location. Issuing credit cards to clients more broadly across the country has proved to be beneficial during the COVlD-19 pandemic in 2020 and 2021 , as different geographical parts of the country and world have been better able to manage the pandemic, which has led to improved economic activity. Technology How do you ensure that you stay up to date with software and technology trends?l Credit card issuers have needed to improve their technology to comply with a variety of regulations levied against them. Additionally, stay up-to-date on a variety of technologies for web design and payment processing allows operators to maintain a competitive advantage compared to its competitors. This has been particularly important in 2020 and 2021, as more services have been provided online during the COVlD-19 pandemic. How have you taken advantage of rising internet and mobile internet penetration into the financial services industry? Credit card issuers have benefited from a higher percentage of services being conducted online since they are primarily completed by using credit cards. This trend has continued considerably in 2020 and 2021 as e-commerce sales have rapidly rose during the COVlD-19 pandemic. Compliance How do you expect the proposed changes to Dodd-Frank to affect your business? Credit Card Issuing in the US July 2021 Dodd-Frank's enactment affected credit card issuers in that it increased regulatory oversight through the formation of the Consumer Financial Protection Bureau. Credit card issuers must continue to monitor new change and policy recommendations that the Consumer Financial Protection Bureau suggests, in order to assure they are following guidelines. How have increased capital requirements under Basel Ill affected operations? Credit card issuers do not experience capital requirements under Basel Ill. Finance Do you have enough capital reserved to be able to invest in new technology/software as soon as it becomes available? Credit card issuers are generally well-capitalized and able to purchase new technology when needed. Having capital available proved beneficial for businesses in 2020, as it allowed them to invest in new technology needed to seamlessly operate during the CDVlD-19 pandemic, as well as to sustain expected loan losses from customers unable to pay their bills. How do your prot margins compare to those of your competitors? Credit card issuers' prot margins fluctuate based on interest rates on credit cards, in addition to their clients paying down outstanding debts. However, industry profit margins substantially declined in 2020 as a result of consumers being unable to pay their bills, which lead to expected loan losses for operators, during the COVID1 9 pandemic. As concerns surrounding the pandemic wane in 2021 and economic activity returns to normal levels, profit margins with the industry are expected to improve in 2021. External Impacts Impact: Aggregate household debt Questions How closely does your business follow trends in aggregate household debt? Do you offer products specifically for household debts? Higher credit card usage leads to increased industry revenue, as both payments to principal and interest accrue, pushing revenue higher. Aggregate household debt slightly increased in 2020 during the COVlD-19 pandemic, in part contributable to individuals who purchased homes for the first time in the year. Aggregate household debt levels are also expected to slightly increase in 2021, as waning concerns surrounding the coronavirus pandemic and increased economic activity lead to more borrowing from consumers. Impact: Prime rate How closely do you follow the prime rate? What do you do to attract customers when interest rates are high? The average interest rate charged by credit Ill'd issuers is typically linked to changes in the prime rate. As the prime rate rises, interest revenue generated by the industry increases as well. In 2020, during the COVlD-19 pandemic, the prime rate precipitously fell as a result of the Federal Reserve lowering the Federal Funds Rate to the zero-bound range. The prime rate is expected to remain low in 2021, as a result of the Federal Reserves commitment to lower interest rates. Impact: Business sentiment Index Do you monitor the business sentiment index? How will you promote temporary staffers over permanent ones as sentiment improves further? Businesses feeling more confident in their long-term financial stability is usually an indicator that consumers are spending, to the benet of industry operators. As a result of steady improvements in the business environment in the back half of 2020, the business sentiment index slightly increased during the COVlD-19 pandemic. IBISWORLD.COM 8 Credit Card Issuing in the us July 2021 Internal Issues Issue: Access to the latest available and most efficient technology and techniques Questions Is your technical expertise to a world standard? How do you achieve and maintain good product quality? How do you keep costs low when doing so? Operators must be able to adopt the latest information technology (especially in delivery systems) that is cost-effective to provide customers with the best possible service. It is particularly important that operators have the ability to bill customers digitally without necessarily needing a paper receipt of bills, along with online bill paying and finance management platforms. Issue: Market research and understanding How do you maintain customer satisfaction? Are changes in demand revealed by major buyers? Do you monitor trends in consumer buying behavior? Understanding the needs of consumers and providing them with a product that meets their needs is crucial to the success of a credit card issuing company. Specic ways that credit card companies maintain customer satisfaction is via reward payments, toptier payment processing platforms and technology, and high-quality customer service. Issue: Having an extensive distribution/collection network What kind of transportation do you rely on to deliver your products? Have you had any problems with distribution or transportation in the past? It is important to establish a network of customers (credit card banks) to distribute the products (credit cards) to customers through a well-developed branch, online and mail network. Being able to rely on delivering products and services mainly online has been vital during the COVlD-19 pandemic. IBISWORLD.COM 7

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance