Answered step by step

Verified Expert Solution

Question

1 Approved Answer

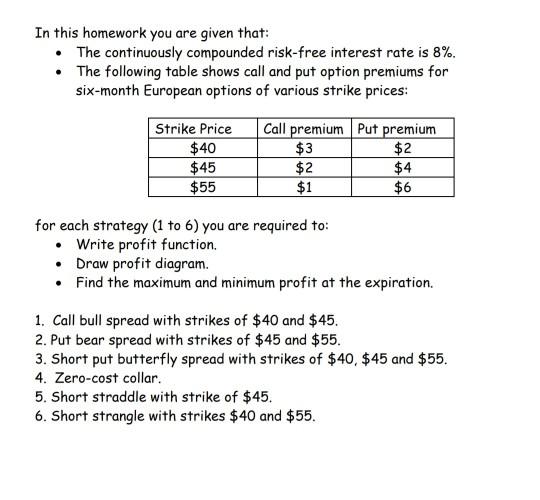

In this homework you are given that: The continuously compounded risk-free interest rate is 8%. The following table shows call and put option premiums for

In this homework you are given that: The continuously compounded risk-free interest rate is 8%. The following table shows call and put option premiums for six-month European options of various strike prices: Strike Price $40 $45 $55 Call premium Put premium $3 $2 $2 $1 $6 $4 for each strategy (1 to 6) you are required to: Write profit function. Draw profit diagram. Find the maximum and minimum profit at the expiration 1. Call bull spread with strikes of $40 and $45. 2. Put bear spread with strikes of $45 and $55. 3. Short put butterfly spread with strikes of $40, $45 and $55. 4. Zero-cost collar. 5. Short straddle with strike of $45. 6. Short strangle with strikes $40 and $55. In this homework you are given that: The continuously compounded risk-free interest rate is 8%. The following table shows call and put option premiums for six-month European options of various strike prices: Strike Price $40 $45 $55 Call premium Put premium $3 $2 $2 $1 $6 $4 for each strategy (1 to 6) you are required to: Write profit function. Draw profit diagram. Find the maximum and minimum profit at the expiration 1. Call bull spread with strikes of $40 and $45. 2. Put bear spread with strikes of $45 and $55. 3. Short put butterfly spread with strikes of $40, $45 and $55. 4. Zero-cost collar. 5. Short straddle with strike of $45. 6. Short strangle with strikes $40 and $55

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Finance

Authors: Scott Besley, Eugene F. Brigham

3rd Edition

0324232624, 9780324232622