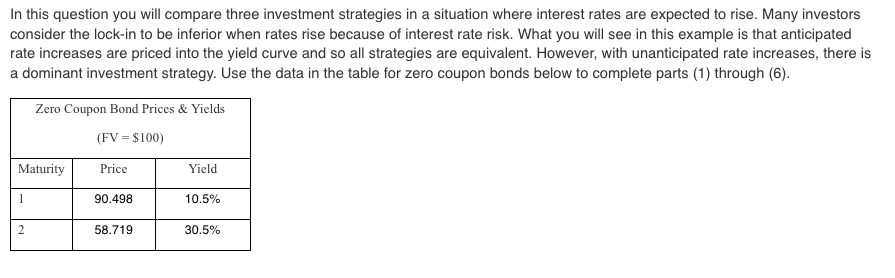

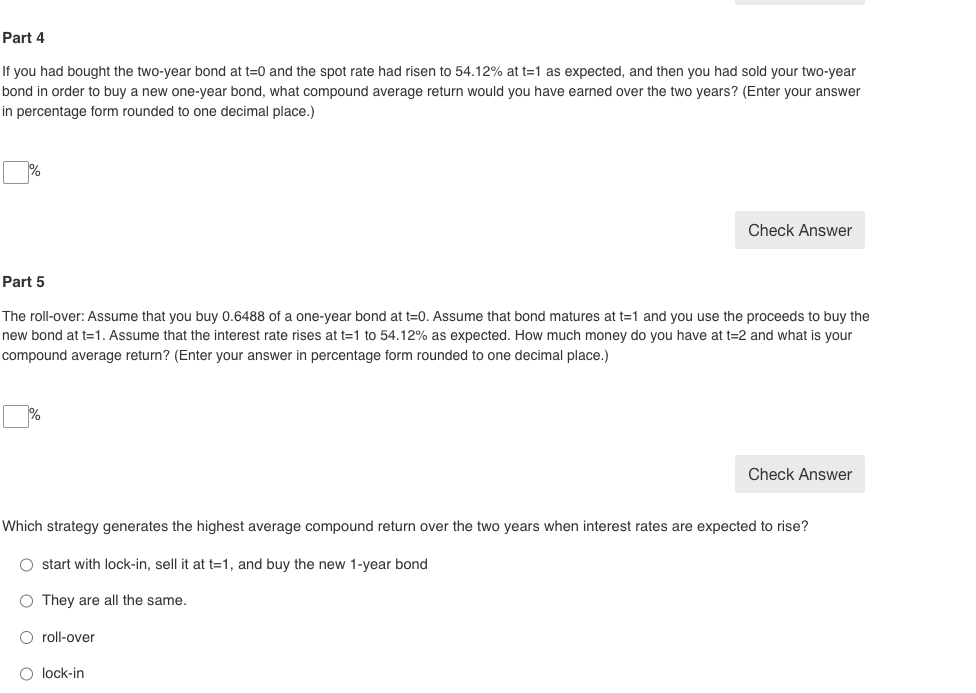

In this question you will compare three investment strategies in a situation where interest rates are expected to rise. Many investors consider the lock-in to be inferior when rates rise because of interest rate risk. What you will see in this example is that anticipated rate increases are priced into the yield curve and so all strategies are equivalent. However, with unanticipated rate increases, there is a dominant investment strategy. Use the data in the table for zero coupon bonds below to complete parts (1) through (6). f you had bought the two-year bond at t=0 and the spot rate had risen to 54.12% at t=1 as expected, and then you had sold your two-year ond in order to buy a new one-year bond, what compound average return would you have earned over the two years? (Enter your answer n percentage form rounded to one decimal place.) % The roll-over: Assume that you buy 0.6488 of a one-year bond at t=0. Assume that bond matures at t=1 and you use the proceeds to buy the new bond at t=1. Assume that the interest rate rises at t=1 to 54.12% as expected. How much money do you have at t=2 and what is your compound average return? (Enter your answer in percentage form rounded to one decimal place.) Which strategy generates the highest average compound return over the two years when interest rates are expected to rise? start with lock-in, sell it at t=1, and buy the new 1-year bond They are all the same. roll-over lock-in In this question you will compare three investment strategies in a situation where interest rates are expected to rise. Many investors consider the lock-in to be inferior when rates rise because of interest rate risk. What you will see in this example is that anticipated rate increases are priced into the yield curve and so all strategies are equivalent. However, with unanticipated rate increases, there is a dominant investment strategy. Use the data in the table for zero coupon bonds below to complete parts (1) through (6). f you had bought the two-year bond at t=0 and the spot rate had risen to 54.12% at t=1 as expected, and then you had sold your two-year ond in order to buy a new one-year bond, what compound average return would you have earned over the two years? (Enter your answer n percentage form rounded to one decimal place.) % The roll-over: Assume that you buy 0.6488 of a one-year bond at t=0. Assume that bond matures at t=1 and you use the proceeds to buy the new bond at t=1. Assume that the interest rate rises at t=1 to 54.12% as expected. How much money do you have at t=2 and what is your compound average return? (Enter your answer in percentage form rounded to one decimal place.) Which strategy generates the highest average compound return over the two years when interest rates are expected to rise? start with lock-in, sell it at t=1, and buy the new 1-year bond They are all the same. roll-over lock-in