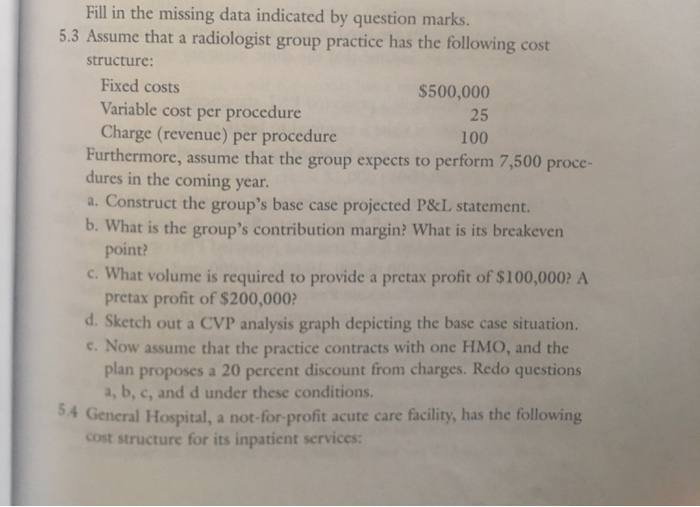

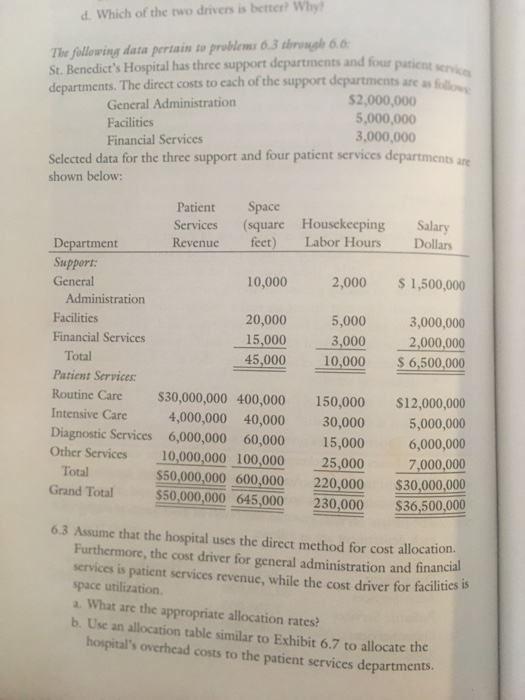

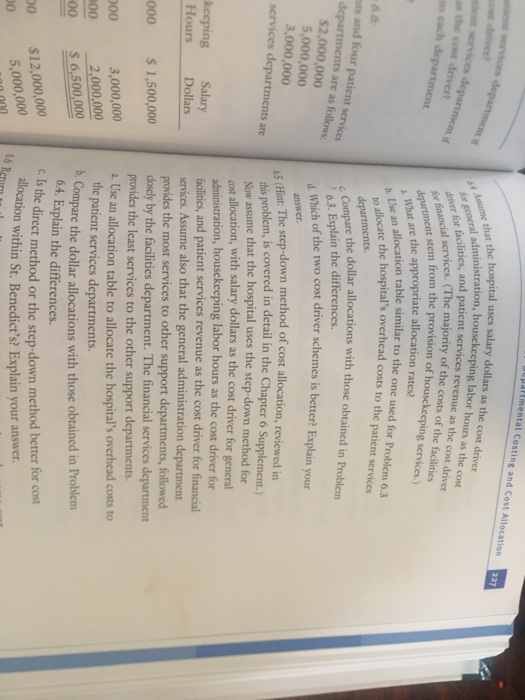

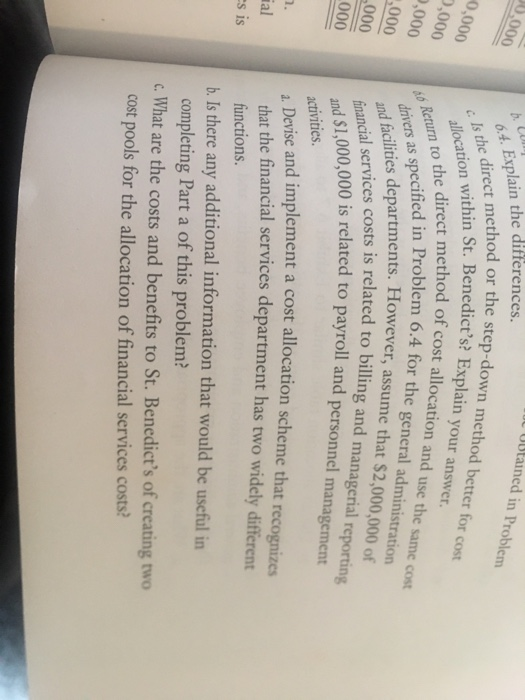

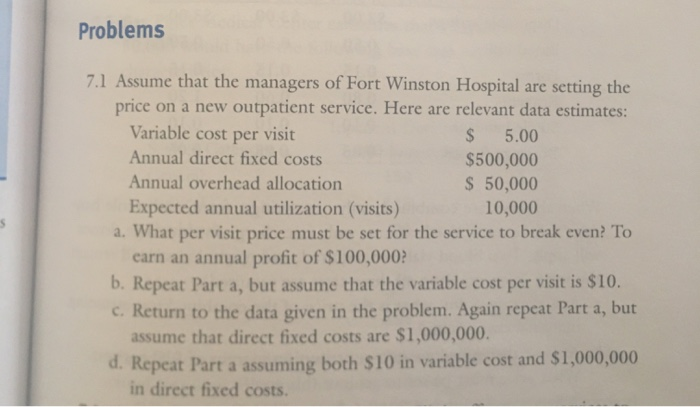

Introduction For problem 5.3 (page 191), radiology group practice, the students will be able to examine the cost structure of a firm, and then use this information to construct a profit & loss statement, graph a cost-value-profit (CVP) analysis, and compute and contribution margin (CM), breakeven point (volume and dollar). In addition, students will observe have changes in a firm's cost structure will impact the CM, breakeven point, and CVP. For problem 6.3 through 6.6 (page 226-227), students will practice allocated direct costs to revenue centers using appropriate cost drivers. This is an essential competency, since management needs to know the actual financial performance of our revenue centers. This cannot occur unless all costs have been properly allocated utilizing an appropriate allocation methodology has been applied. Finally, the students will complete problem 7.1, Fort Winston Hospital (page 257), where the students will be provided relevant data that will be necessary to establish the price for a new outpatient service. As the estimates are changes, the students will be able to ascertain the impact of the entity's projected breakeven point. Properly setting prices for goods and services is necessary to ensure a firm's revenues will be adequate to cover its' operating expenses and debt service obligations as they come due. Directions The students are expected to carefully read the assignment instructions, then thoroughly and explicitly address each question for both problems. Microsoft Excel will be used to setup and perform the mathematical computations and graphs; however, the questions and their corresponding responses should be written up in a Microsoft Word document. IMPORTANT: Make certain that there is a detailed description of how the calculations were performed. Students should create and label one tab in the Excel spreadsheet for each problem, but should prepare one Word document that contains the questions and responses for both problems. While there is no minimum number of references that need to be utilized to support the completion of this assignment, it is generally understood that outside sources, including the text will be necessary to complete the problems. The document must adhere to the APA writing style in terms of using in-text citations and the listing of sources on the references page The Microsoft Word document and Excel spreadsheet are to be uploaded to Submit Assignment Fill in the missing data indicated by question marks. 5.3 Assume that a radiologist group practice has the following cost structure: Fixed costs $500,000 Variable cost per procedure 25 Charge (revenue) per procedure 100 Furthermore, assume that the group expects to perform 7,500 proce- dures in the coming year. a. Construct the group's base case projected P&L statement. b. What is the group's contribution argin? What is its breakeven point? c. What volume is required to provide a pretax profit of $100,000? A pretax profit of $200,000? d. Sketch out a CVP analysis graph depicting the base case situation. c. Now assume that the practice contracts with one HMO, and the plan proposes a 20 percent discount from charges. Redo questions a, b, c, and d under these conditions. 54 General Hospital, a not-for-profit acute care facility, has the following cost structure for its inpatient services: St. Benedict's Hospital has three support departments and four patients departments. The direct costs to each of the support departments are as follow d. Which of the two drivers is better? Why? The following data pertain to problems 6.3 through 6.0; General Administration $2,000,000 Facilities 5,000,000 Financial Services 3,000,000 Selected data for the three support and four patient services departments are shown below: Salary Dollars $ 1,500,000 Patient Space Services (square Housekeeping Department Revenue feet) Labor Hours Support: General 10,000 2,000 Administration Facilities 20,000 5,000 Financial Services 15,000 3,000 Total 45,000 10,000 Patient Services: Routine Care $30,000,000 400,000 150,000 Intensive Care 4,000,000 40,000 30,000 Diagnostic Services 6,000,000 60,000 15,000 Other Services 10,000,000 100,000 25,000 Total $50,000,000 600,000 220,000 Grand Total $50,000,000 645,000 230,000 3,000,000 2,000,000 $ 6,500,000 $12,000,000 5,000,000 6,000,000 7,000,000 $30,000,000 $36,500,000 6.3 Assume that the hospital uses the direct method for cost allocation. Furthermore, the cost driver for general administration and financial services is patient services revenue, while the cost driver for facilities is space utilization a. What are the appropriate allocation rates? b. Use an allocation table similar to Exhibit 6.7 to allocate the hospital's overhead costs to the patient services departments, Darlmental Costing and Cost Allocation rvices department if the cost driver department Jo allocate the hospital's overhead costs to the patient services departments 6.3. Explain the differences. and four patient services departments are as follows $2,000,000 5,000,000 3,000,000 services departments are answer keeping Hours Salary Dollars 000 65 (Hint: The step-down method of cost allocation, reviewed in this problem, is covered in detail in the Chapter 6 Supplement.) Now assume that the hospital uses the step-down method for cost allocation, with salary dollars as the cost driver for general administration, housekeeping labor hours as the cost driver for facilities, and patient services revenue as the cost driver for financial services. Assume also that the general administration department provides the most services to other support departments, followed closely by the facilities department. The financial services department provides the least services to the other support departments. 2. Use an allocation table to allocate the hospital's overhead costs to the patient services departments. b. Compare the dollar allocations with those obtained in Problem 6.4. Explain the differences. Is the direct method or the step-down method better for cost $ 1,500,000 000 000 00 3,000,000 2,000,000 $ 6,500,000 20 0 $12,000,000 5,000,000 66 Re cat services department is for general administration, housekeeping labor hours as the cost lesume that the hospital uses salary dollars as the cost driver driver for facilities, and patient services revenue as the cost driver for financial services. The majority of the costs of the facilities department stem from the provision of housekeeping services.) What are the appropriate allocation rates) b. Use an allocation table similar to the one used for Problem 6.3 c Compare the dollar allocations with those obtained in Problem d. Which of the two cost driver schemes is better? Explain your allocation within St. Benedict's? Explain your answer. 0.000 Utained in Problem b.com 0,000 2,000 2,000 1,000 ,000 000 activities. 7. ial es is a. Devise and implement a cost allocation scheme that recognizes that the financial services department has two widely different functions. b. Is there any additional information that would be useful in completing Part a of this problem? c. What are the costs and benefits to St. Benedict's of creating two cost pools for the allocation of financial services costs? 6.4. Explain the differences. allocation within St. Benedict's? Explain your answer. Is the direct method or the step-down method better for cost Return to the direct method of cost allocation and use the same cost and facilities departments. However, assume that $2,000,000 of financial services costs is related to billing and managerial reporting and $1,000,000 is related to payroll and personnel management drivers as specified in Problem 6.4 for the general administration Problems 7.1 Assume that the managers of Fort Winston Hospital are setting the price on a new outpatient service. Here are relevant data estimates: Variable cost per visit $ 5.00 Annual direct fixed costs $500,000 Annual overhead allocation $ 50,000 Expected annual utilization (visits) 10,000 a. What per visit price must be set for the service to break even? To earn an annual profit of $100,000? b. Repeat Part a, but assume that the variable cost per visit is $10. c. Return to the data given in the problem. Again repeat Part a, but assume that direct fixed costs are $1,000,000. d. Repeat Part a assuming both $10 in variable cost and $1,000,000 in direct fixed costs. Introduction For problem 5.3 (page 191), radiology group practice, the students will be able to examine the cost structure of a firm, and then use this information to construct a profit & loss statement, graph a cost-value-profit (CVP) analysis, and compute and contribution margin (CM), breakeven point (volume and dollar). In addition, students will observe have changes in a firm's cost structure will impact the CM, breakeven point, and CVP. For problem 6.3 through 6.6 (page 226-227), students will practice allocated direct costs to revenue centers using appropriate cost drivers. This is an essential competency, since management needs to know the actual financial performance of our revenue centers. This cannot occur unless all costs have been properly allocated utilizing an appropriate allocation methodology has been applied. Finally, the students will complete problem 7.1, Fort Winston Hospital (page 257), where the students will be provided relevant data that will be necessary to establish the price for a new outpatient service. As the estimates are changes, the students will be able to ascertain the impact of the entity's projected breakeven point. Properly setting prices for goods and services is necessary to ensure a firm's revenues will be adequate to cover its' operating expenses and debt service obligations as they come due. Directions The students are expected to carefully read the assignment instructions, then thoroughly and explicitly address each question for both problems. Microsoft Excel will be used to setup and perform the mathematical computations and graphs; however, the questions and their corresponding responses should be written up in a Microsoft Word document. IMPORTANT: Make certain that there is a detailed description of how the calculations were performed. Students should create and label one tab in the Excel spreadsheet for each problem, but should prepare one Word document that contains the questions and responses for both problems. While there is no minimum number of references that need to be utilized to support the completion of this assignment, it is generally understood that outside sources, including the text will be necessary to complete the problems. The document must adhere to the APA writing style in terms of using in-text citations and the listing of sources on the references page The Microsoft Word document and Excel spreadsheet are to be uploaded to Submit Assignment Fill in the missing data indicated by question marks. 5.3 Assume that a radiologist group practice has the following cost structure: Fixed costs $500,000 Variable cost per procedure 25 Charge (revenue) per procedure 100 Furthermore, assume that the group expects to perform 7,500 proce- dures in the coming year. a. Construct the group's base case projected P&L statement. b. What is the group's contribution argin? What is its breakeven point? c. What volume is required to provide a pretax profit of $100,000? A pretax profit of $200,000? d. Sketch out a CVP analysis graph depicting the base case situation. c. Now assume that the practice contracts with one HMO, and the plan proposes a 20 percent discount from charges. Redo questions a, b, c, and d under these conditions. 54 General Hospital, a not-for-profit acute care facility, has the following cost structure for its inpatient services: St. Benedict's Hospital has three support departments and four patients departments. The direct costs to each of the support departments are as follow d. Which of the two drivers is better? Why? The following data pertain to problems 6.3 through 6.0; General Administration $2,000,000 Facilities 5,000,000 Financial Services 3,000,000 Selected data for the three support and four patient services departments are shown below: Salary Dollars $ 1,500,000 Patient Space Services (square Housekeeping Department Revenue feet) Labor Hours Support: General 10,000 2,000 Administration Facilities 20,000 5,000 Financial Services 15,000 3,000 Total 45,000 10,000 Patient Services: Routine Care $30,000,000 400,000 150,000 Intensive Care 4,000,000 40,000 30,000 Diagnostic Services 6,000,000 60,000 15,000 Other Services 10,000,000 100,000 25,000 Total $50,000,000 600,000 220,000 Grand Total $50,000,000 645,000 230,000 3,000,000 2,000,000 $ 6,500,000 $12,000,000 5,000,000 6,000,000 7,000,000 $30,000,000 $36,500,000 6.3 Assume that the hospital uses the direct method for cost allocation. Furthermore, the cost driver for general administration and financial services is patient services revenue, while the cost driver for facilities is space utilization a. What are the appropriate allocation rates? b. Use an allocation table similar to Exhibit 6.7 to allocate the hospital's overhead costs to the patient services departments, Darlmental Costing and Cost Allocation rvices department if the cost driver department Jo allocate the hospital's overhead costs to the patient services departments 6.3. Explain the differences. and four patient services departments are as follows $2,000,000 5,000,000 3,000,000 services departments are answer keeping Hours Salary Dollars 000 65 (Hint: The step-down method of cost allocation, reviewed in this problem, is covered in detail in the Chapter 6 Supplement.) Now assume that the hospital uses the step-down method for cost allocation, with salary dollars as the cost driver for general administration, housekeeping labor hours as the cost driver for facilities, and patient services revenue as the cost driver for financial services. Assume also that the general administration department provides the most services to other support departments, followed closely by the facilities department. The financial services department provides the least services to the other support departments. 2. Use an allocation table to allocate the hospital's overhead costs to the patient services departments. b. Compare the dollar allocations with those obtained in Problem 6.4. Explain the differences. Is the direct method or the step-down method better for cost $ 1,500,000 000 000 00 3,000,000 2,000,000 $ 6,500,000 20 0 $12,000,000 5,000,000 66 Re cat services department is for general administration, housekeeping labor hours as the cost lesume that the hospital uses salary dollars as the cost driver driver for facilities, and patient services revenue as the cost driver for financial services. The majority of the costs of the facilities department stem from the provision of housekeeping services.) What are the appropriate allocation rates) b. Use an allocation table similar to the one used for Problem 6.3 c Compare the dollar allocations with those obtained in Problem d. Which of the two cost driver schemes is better? Explain your allocation within St. Benedict's? Explain your answer. 0.000 Utained in Problem b.com 0,000 2,000 2,000 1,000 ,000 000 activities. 7. ial es is a. Devise and implement a cost allocation scheme that recognizes that the financial services department has two widely different functions. b. Is there any additional information that would be useful in completing Part a of this problem? c. What are the costs and benefits to St. Benedict's of creating two cost pools for the allocation of financial services costs? 6.4. Explain the differences. allocation within St. Benedict's? Explain your answer. Is the direct method or the step-down method better for cost Return to the direct method of cost allocation and use the same cost and facilities departments. However, assume that $2,000,000 of financial services costs is related to billing and managerial reporting and $1,000,000 is related to payroll and personnel management drivers as specified in Problem 6.4 for the general administration Problems 7.1 Assume that the managers of Fort Winston Hospital are setting the price on a new outpatient service. Here are relevant data estimates: Variable cost per visit $ 5.00 Annual direct fixed costs $500,000 Annual overhead allocation $ 50,000 Expected annual utilization (visits) 10,000 a. What per visit price must be set for the service to break even? To earn an annual profit of $100,000? b. Repeat Part a, but assume that the variable cost per visit is $10. c. Return to the data given in the problem. Again repeat Part a, but assume that direct fixed costs are $1,000,000. d. Repeat Part a assuming both $10 in variable cost and $1,000,000 in direct fixed costs