Jose Flores, the sole owner and president of Consoli- dated Electric Company, reflected on his inventory man- agement problems. He was a major wholesale

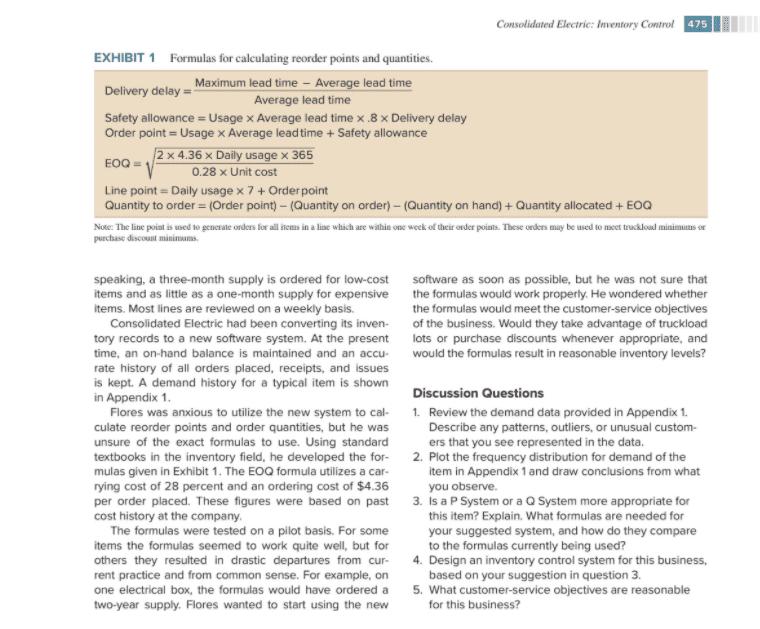

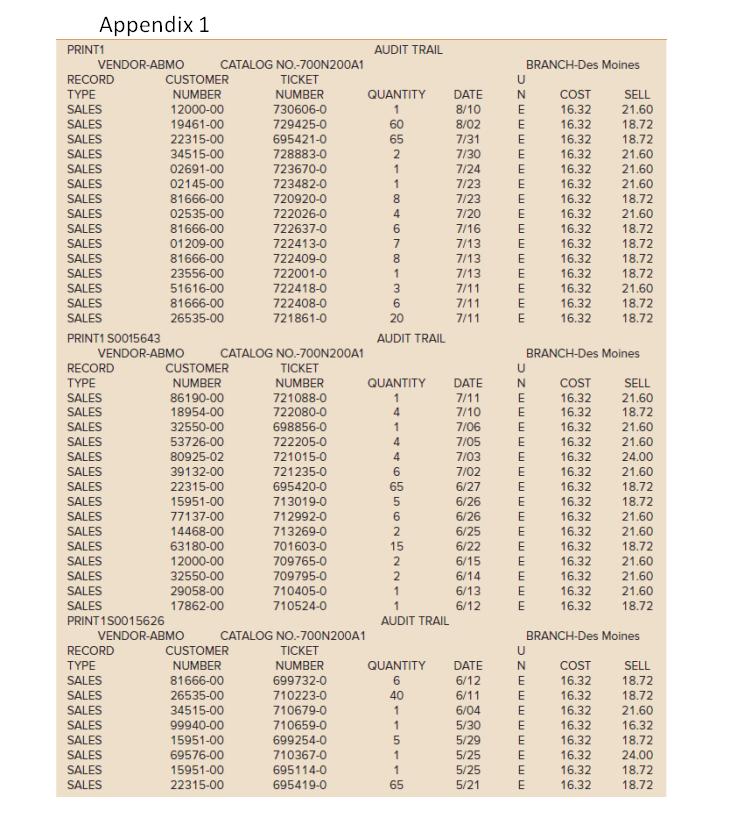

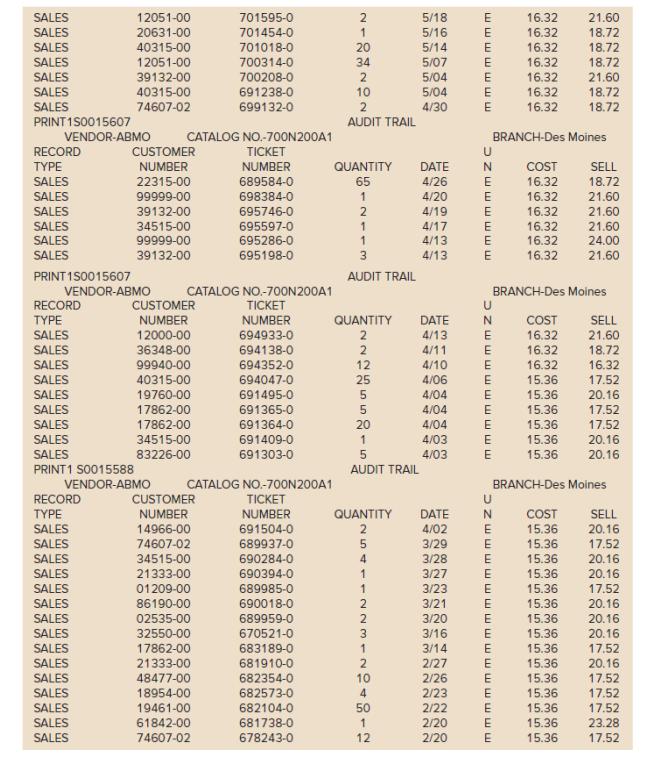

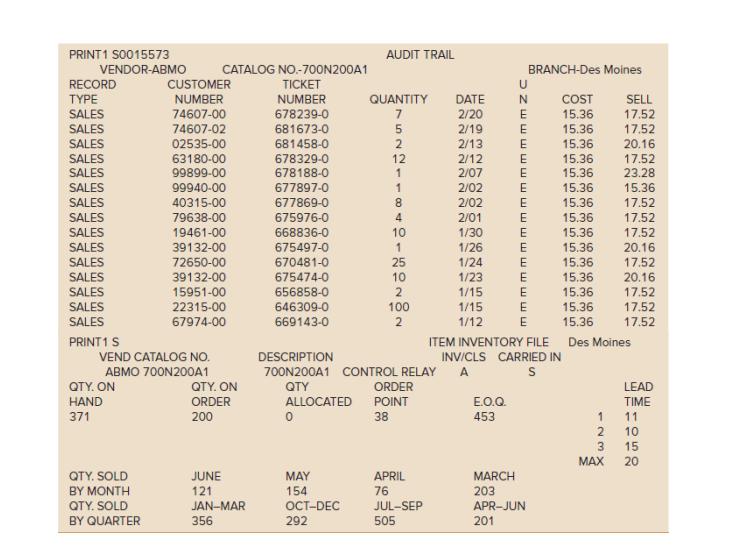

Jose Flores, the sole owner and president of Consoli- dated Electric Company, reflected on his inventory man- agement problems. He was a major wholesale supplier of equipment and supplies to electrical contractors, and his business hinged on the efficient management of inventories to meet his customers' needs. While he had built a very successful business, he was nearing retire- ment and wanted to pass along a good inventory man- agement system to his daughter who would take over management of the company. Flores started Consolidated Electric Company in the 1980s and built it into a highly profitable business. In 2016 the company had achieved $10 million in sales and earned $1 million in pretax profits. Consolidated Electric was currently the twelfth largest electrical wholesaler in the country. Consolidated Electric operates through four ware- houses in the Midwest (Des Moines, Duluth, Madison, and St. Louis). From these sites, contractors in lowe, Minnesota, Nebraska, Wisconsin, Illinois, and Missouri are supplied with a wide range of electrical equipment, including wire, electrical boxes, connectors, lighting fix- tures, and electrical controllers. The company stocks 20,000 separate line items in its inventory purchased from 200 different manufacturers. (A line item is defined as a particular item carried at a particular location.) These items range from less than 1 cent each to several hundred dollars for the largest electrical controllers. Of the 20,000 line items, a great many are carried to provide a full line of service. For example, the top 2,000 items account for 50 percent of the sales and the bottom 10,000 items for only 20 percent. The remaining 8,000 items account for 30 percent of the sales. The company has continually purged its 20,000 inven- tory items to carry only those that are demanded at least once a year. As Flores says, "We live and die by good customer service at a reasonable selling price. If we do not meet this objective, the customer will go to another wholesaler or buy directly from the manufacturer." He explained that he currently managed inventory by using an "earn and turn" concept. According to this con- cept, the earnings margin multiplied by the inventory turn ratio must equal a constant value of 2.0. For exam- ple, if a particular electrical item costs $6 to purchase wholesale and is sold for $10, then the earnings margin is $4 and the earn ratio for this item is $4/$10= 40. If this item has a turn ratio of 5 times a year (sales are 5 times the average inventory carried), then the product of earn and turn is.4(5)=2.0. If another item earns more. it can turn slower, if it earns less, it must turn faster. Each year, Flores sets a target earn-turn ratio for the entire business and a value for each product line. These targets are based on the estimated costs of operations and the return-on-investment goal for the company. As stated above, the current target ratio for the business is 2.0. The purchasing agents and inventory managers at each location are measured by their ability to meet the target eam-turn ratios on their product lines. The actual ratios are reported monthly. alegdudko/123RF Although earn-turn ratios work quite well in control- ling profitability of the business and entire product lines, they do not work very well for individual inventory items. Some line items tend to be in excess supply, while others are often out of stock. The inventory is currently managed using basic soft- ware. A record for each item is kept and a worker posts transactions on the record as units are received or issued, thus keeping a running on-hand inventory balance. Peri- odically, a purchasing agent reviews the records for a particular supplier. Then, using the order point and quan- tity stored on the record, the purchasing agent places an order for all items that are below their reorder point. If the total quantities of all items required from a sup- plier do not meet the purchase discount minimums or a truckload lot, additional items near their reorder points are added to the order. This is not done when the total order size is too far from the minimums, since excessive inventories would build up. The order quantity and reorder point on each record are based on judgment and past experience. Generally EXHIBIT 1 Formulas for calculating reorder points and quantities. Delivery delay = Maximum lead time - Average lead time Average lead time Safety allowance = Usage x Average lead time x .8 x Delivery delay Order point = Usage x Average lead time + Safety allowance EOQ= Line point = Daily usage x 7 + Orderpoint Quantity to order = (Order point) - (Quantity on order) - (Quantity on hand) + Quantity allocated + EOQ 2 x 4.36 x Daily usage x 365 0.28 x Unit cost Consolidated Electric: Inventory Control 475 Note: The line point is used to generate orders for all items in a line which are within one week of their order points. These orders may be used to meet truckload minimums or purchase discount minimams. speaking, a three-month supply is ordered for low-cost items and as little as a one-month supply for expensive items. Most lines are reviewed on a weekly basis. Consolidated Electric had been converting its inven- tory records to a new software system. At the present time, an on-hand balance is maintained and an accu- rate history of all orders placed, receipts, and issues is kept. A demand history for a typical item is shown in Appendix 1. Flores was anxious to utilize the new system to cal- culate reorder points and order quantities, but he was unsure of the exact formulas to use. Using standard textbooks in the inventory field, he developed the for- mulas given in Exhibit 1. The EOQ formula utilizes a car- rying cost of 28 percent and an ordering cost of $4.36 per order placed. These figures were based on past cost history at the company. The formulas were tested on a pilot basis. For some items the formulas seemed to work quite well, but for others they resulted in drastic departures from cur- rent practice and from common sense. For example, on one electrical box, the formulas would have ordered a two-year supply. Flores wanted to start using the new software as soon as possible, but he was not sure that the formulas would work properly. He wondered whether the formulas would meet the customer-service objectives of the business. Would they take advantage of truckload lots or purchase discounts whenever appropriate, and would the formulas result in reasonable inventory levels? Discussion Questions 1. Review the demand data provided in Appendix 1. Describe any patterns, outliers, or unusual custom- ers that you see represented in the data. 2. Plot the frequency distribution for demand of the item in Appendix 1 and draw conclusions from what you observe. 3. Is a P System or a Q System more appropriate for this item? Explain. What formulas are needed for your suggested system, and how do they compare to the formulas currently being used? 4. Design an inventory control system for this business, based on your suggestion in question 3. 5. What customer-service objectives are reasonable for this business? Appendix 1 PRINT1 VENDOR-ABMO RECORD TYPE SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES PRINT1 S0015643 RECORD TYPE SALES SALES SALES VENDOR-ABMO SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES PRINT 1S0015626 CATALOG NO.-700N200A1 TICKET NUMBER 730606-0 729425-0 695421-0 728883-0 723670-0 723482-0 720920-0 722026-0 722637-0 722413-0 722409-0 722001-0 722418-0 722408-0 721861-0 CUSTOMER NUMBER 12000-00 19461-00 22315-00 34515-00 02691-00 02145-00 81666-00 02535-00 81666-00 RECORD TYPE SALES SALES SALES SALES SALES SALES SALES SALES 01209-00 81666-00 23556-00 51616-00 81666-00 26535-00 CATALOG NO.-700N200A1 TICKET NUMBER 721088-0 722080-0 698856-0 722205-0 721015-0 721235-0 695420-0 CUSTOMER NUMBER 86190-00 18954-00 32550-00 53726-00 80925-02 39132-00 22315-00 15951-00 77137-00 14468-00 63180-00 12000-00 32550-00 29058-00 17862-00 VENDOR-ABMO CATALOG NO.-700N200A1 CUSTOMER NUMBER 81666-00 26535-00 34515-00 99940-00 713019-0 712992-0 713269-0 15951-00 69576-00 15951-00 22315-00 701603-0 709765-0 709795-0 710405-0 710524-0 TICKET NUMBER 699732-0 710223-0 710679-0 710659-0 699254-0 710367-0 695114-0 695419-0 AUDIT TRAIL QUANTITY DATE 8/10 1 60 65 2 1 1 8 4 6 7 8 1 3 6 20 AUDIT TRAIL QUANTITY 1 4 1 4 4 6 65 5 6 2 15 2~~-- 1 1 AUDIT TRAIL 8/02 7/31 7/30 7/24 7/23 7/23 7/20 7/16 7/13 7/13 7/13 7/11 7/11 7/11 U N mmmmmmmmmmmmmmmz 6/26 6/26 6/25 6/22 6/15 6/14 6/13 6/12 QUANTITY DATE 6 6/12 6/11 40 1 1 6/04 5/30 5/29 5 1 5/25 5/25 1 65 5/21 BRANCH-Des Moines COST SELL 16.32 21.60 16.32 18.72 16.32 E E E 18.72 E 16.32 21.60 16.32 21.60 21.60 18.72 E E E E E E E E E E E U DATE N mmmmmmmmmmmmmmmz C 7/11 7/10 7/06 7/05 7/03 7/02 E E E E 6/27 E E E BRANCH-Des Moines E E E E E E UNEEwwwwww 18.72 18.72 16.32 21.60 E 16.32 21.60 16.32 18.72 16.32 21.60 16.32 21.60 16.32 21.60 16.32 18.72 E E E 16.32 16.32 E 16.32 16.32 16.32 16.32 16.32 E 16.32 16.32 16.32 E BRANCH-Des Moines 21.60 18.72 18.72 18.72 18.72 21.60 18.72 18.72 COST SELL 16.32 21.60 16.32 18.72 16.32 21.60 16.32 21.60 16.32 24.00 16.32 21.60 16.32 16.32 COST 16.32 16.32 16.32 16.32 16.32 16.32 16.32 16.32 SELL 18.72 18.72 21.60 16.32 18.72 24.00 18.72 18.72 SALES SALES SALES SALES SALES SALES SALES PRINT1S0015607 RECORD TYPE SALES SALES VENDOR-ABMO SALES SALES SALES SALES PRINT 1S0015607 RECORD TYPE SALES SALES SALES SALES SALES SALES 12051-00 20631-00 40315-00 12051-00 39132-00 40315-00 74607-02 VENDOR-ABMO SALES SALES SALES PRINT1 S0015588 RECORD TYPE SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES CUSTOMER NUMBER 22315-00 99999-00 39132-00 34515-00 99999-00 39132-00 CATALOG NO.-700N200A1 TICKET NUMBER 689584-0 CUSTOMER NUMBER 12000-00 36348-00 99940-00 VENDOR-ABMO 40315-00 19760-00 17862-00 17862-00 34515-00 83226-00 701595-0 701454-0 701018-0 CATALOG NO.-700N200A1 TICKET NUMBER 694933-0 CUSTOMER NUMBER 14966-00 74607-02 34515-00 700314-0 700208-0 691238-0 699132-0 21333-00 01209-00 86190-00 02535-00 32550-00 17862-00 21333-00 48477-00 18954-00 19461-00 61842-00 74607-02 698384-0 695746-0 695597-0 695286-0 695198-0 CATALOG NO.-700N200A1 TICKET NUMBER 691504-0 689937-0 690284-0 690394-0 689985-0 690018-0 689959-0 670521-0 683189-0 681910-0 682354-0 682573-0 682104-0 681738-0 678243-0 694138-0 694352-0 694047-0 691495-0 691365-0 691364-0 691409-0 691303-0 2 1 22222 20 34 10 AUDIT TRAIL QUANTITY DATE 65 4/26 1 4/20 4/19 4/17 4/13 4/13 2 1 1 3 AUDIT TRAIL QUANTITY 2 5 4 QUANTITY 2 2 12 25 5 5 20 1 5 AUDIT TRAIL 1 1 -NNMIND48I2 3 1 10 50 5/18 5/16 5/14 5/07 5/04 5/04 4/30 1 12 4/04 4/04 4/03 4/03 DATE 4/02 3/29 16.32 16.32 E 16.32 E E E E 3/20 3/16 3/14 2/27 2/26 2/23 2/22 2/20 2/20 mmmmmmm E E N E E E E E E BRANCH-Des Moines mmmmmmmmmzc U BRANCH-Des Moines DATE N COST 4/13 16.32 4/11 16.32 4/10 E 16.32 4/06 E 15.36 4/04 15.36 15.36 15.36 E E E E E E E N E E 3/28 E 21.60 18.72 18.72 16.32 18.72 16.32 21.60 18.72 18.72 3/27 E 3/23 E 3/21 16.32 16.32 E E E E E E E E E COST 16.32 16.32 16.32 16.32 16.32 16.32 SELL 18.72 21.60 21.60 BRANCH-Des Moines COST 15.36 15.36 15.36 15.36 21.60 24.00 21.60 SELL 21.60 18.72 16.32 17.52 20.16 17.52 17.52 15.36 20.16 15.36 20.16 SELL 20.16 17.52 20.16 20.16 17.52 20.16 20.16 20.16 17.52 20.16 15.36 15.36 15.36 15.36 15.36 15.36 15.36 17.52 15.36 17.52 15.36 17.52 15.36 23.28 15.36 17.52 PRINT1 S0015573 VENDOR-ABMO RECORD TYPE SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES SALES PRINT1 S QTY. ON HAND 371 QTY. SOLD BY MONTH QTY. SOLD BY QUARTER CATALOG NO.-700N200A1 TICKET NUMBER CUSTOMER NUMBER 74607-00 74607-02 02535-00 63180-00 99899-00 VEND CATALOG NO. ABMO 700N200A1 99940-00 40315-00 79638-00 19461-00 39132-00 72650-00 39132-00 15951-00 22315-00 67974-00 QTY. ON ORDER 200 JUNE 121 JAN-MAR 356 678239-0 681673-0 681458-0 678329-0 678188-0 677897-0 677869-0 675976-0 668836-0 675497-0 670481-0 675474-0 656858-0 646309-0 669143-0 0 AUDIT TRAIL MAY 154 OCT-DEC 292 QUANTITY DATE 7 2/20 2/19 2/13 2/12 2/07 SENTIETO-ONEN 5 2 12 1 1 8 4 10 1 25 10 2 100 2 DESCRIPTION 700N200A1 CONTROL RELAY A QTY ALLOCATED ORDER POINT 38 2/02 APRIL 76 JUL-SEP 505 2/02 15.36 E 15.36 2/01 15.36 E 1/30 E 15.36 1/26 E 15.36 1/24 E 15.36 1/23 E 15.36 1/15 E 15.36 1/15 E 15.36 1/12 E 15.36 ITEM INVENTORY FILE Des Moines INV/CLS CARRIED IN S E.O.Q. 453 BRANCH-Des Moines COST SELL 15.36 17.52 15.36 17.52 15.36 20.16 15.36 15.36 U N E E E E E E MARCH 203 APR-JUN 201 17.52 23.28 15.36 17.52 17.52 17.52 20.16 1 2 3 MAX 17.52 20.16 17.52 17.52 17.52 LEAD TIME 11 10 15 20

Step by Step Solution

3.54 Rating (171 Votes )

There are 3 Steps involved in it

Step: 1

1...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Scott B. Smart, Lawrence J. Gitman, Michael D. Joehnk

12th edition

978-0133075403, 133075354, 9780133423938, 133075400, 013342393X, 978-0133075359