Answered step by step

Verified Expert Solution

Question

1 Approved Answer

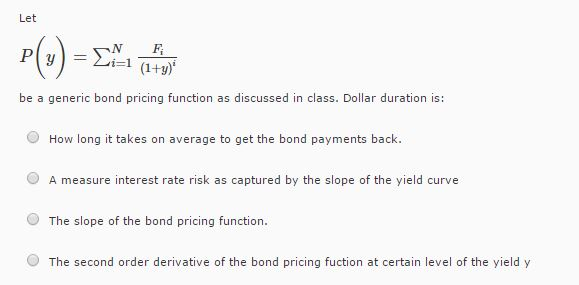

Let P(y) = sigma^N_i=1 F_i/(1+y)^i be a generic bond pricing function as discussed in class. Dollar duration is: How long it takes on average to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Investments

Authors: Charles J. Corrado

3rd Edition

0072829192, 978-0072829198