Answered step by step

Verified Expert Solution

Question

1 Approved Answer

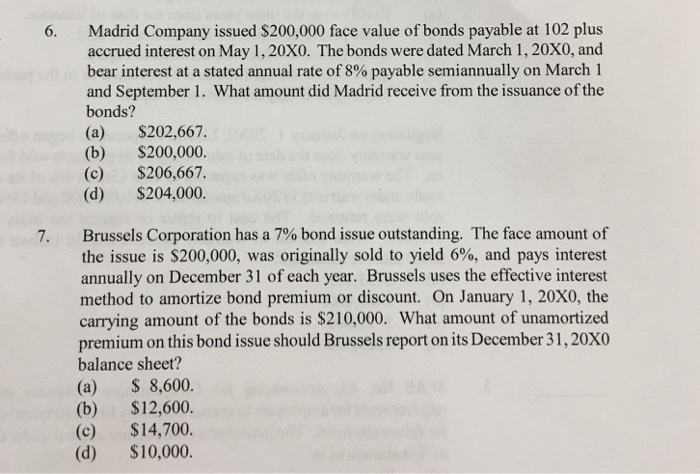

Madrid Company issued $200,000 face value of bonds payable at 102 plus accrued interest on May 1,20X0. The bonds were dated March 1, 20X0, and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Oakton Community College Tools For Business Decision Making

Authors: Paul D. Kimmel ,Jerry J. Weygandt ,Donald E. Kieso

6th Edition

1118113632, 978-1118113639