Answered step by step

Verified Expert Solution

Question

1 Approved Answer

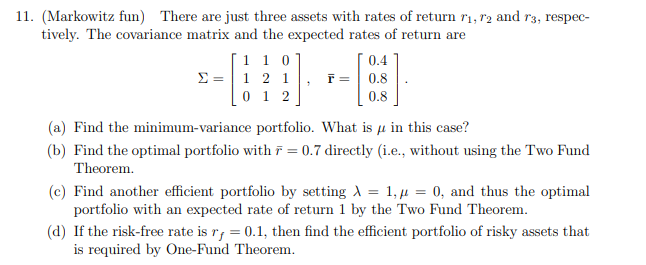

( Markowitz fun ) There are just three assets with rates of return r 1 , r 2 and r 3 , respec - tively.

Markowitz fun There are just three assets with rates of return and respec

tively. The covariance matrix and the expected rates of return are

a Find the minimumvariance portfolio. What is in this case?

b Find the optimal portfolio with directly ie without using the Two Fund

Theorem.

c Find another efficient portfolio by setting and thus the optimal

portfolio with an expected rate of return by the Two Fund Theorem.

d If the riskfree rate is then find the efficient portfolio of risky assets that

is required by OneFund Theorem.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started