Answered step by step

Verified Expert Solution

Question

1 Approved Answer

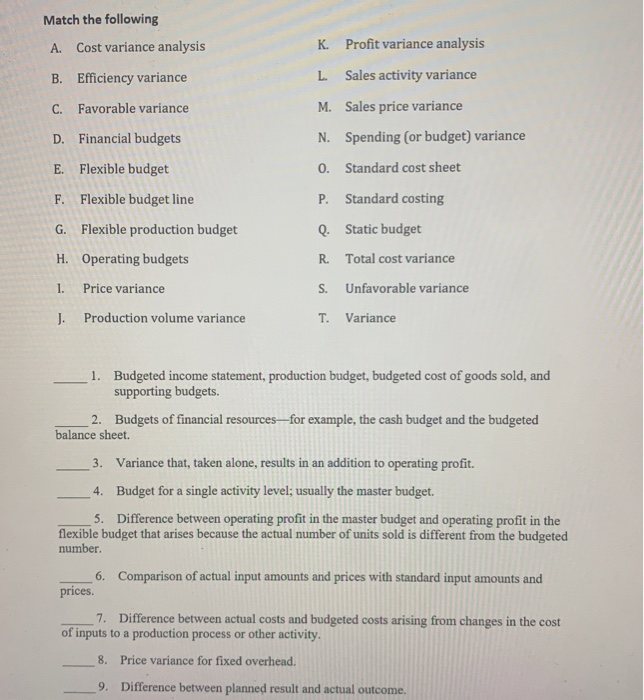

Match the following A. Cost variance analysis k K. Profit variance analysis B. Efficiency variance L. Sala Sales activity variance ahce C. Favorable variance ariance

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

M Glichkeiten Und Grenzen Der F Rderung Verantwortlichen Handelns Von Wirtschaftspr Fern In Moralisch Relevanten Situationen Eine Theoretische Und And Accounting Studies

Authors: Catharina Schmiele

2012 Edition

383493335X, 978-3834933355