Answered step by step

Verified Expert Solution

Question

1 Approved Answer

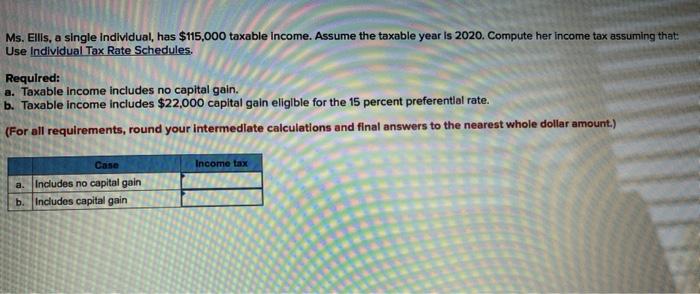

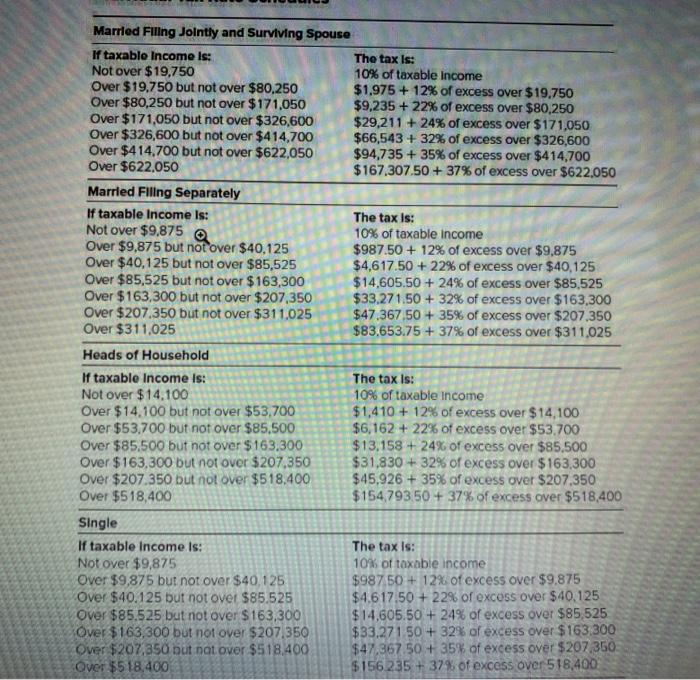

Ms. Ellis, a single individual, has $115,000 taxable income. Assume the taxable year is 2020. Compute her income tax assuming that: Use Individual Tax Rate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Do It Yourself Home Energy Audits 140 Simple Solutions To Lower Energy Costs, Increase Your Home's Efficiency, And Save The Environmen

Authors: David Findley

1st Edition

0071636390, 978-0071636391