Answered step by step

Verified Expert Solution

Question

1 Approved Answer

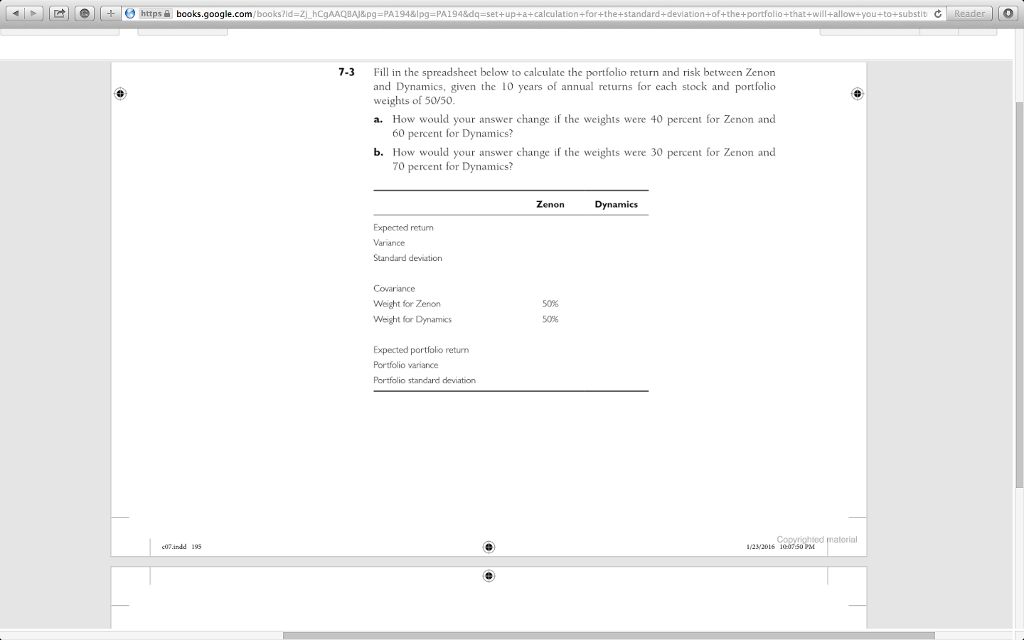

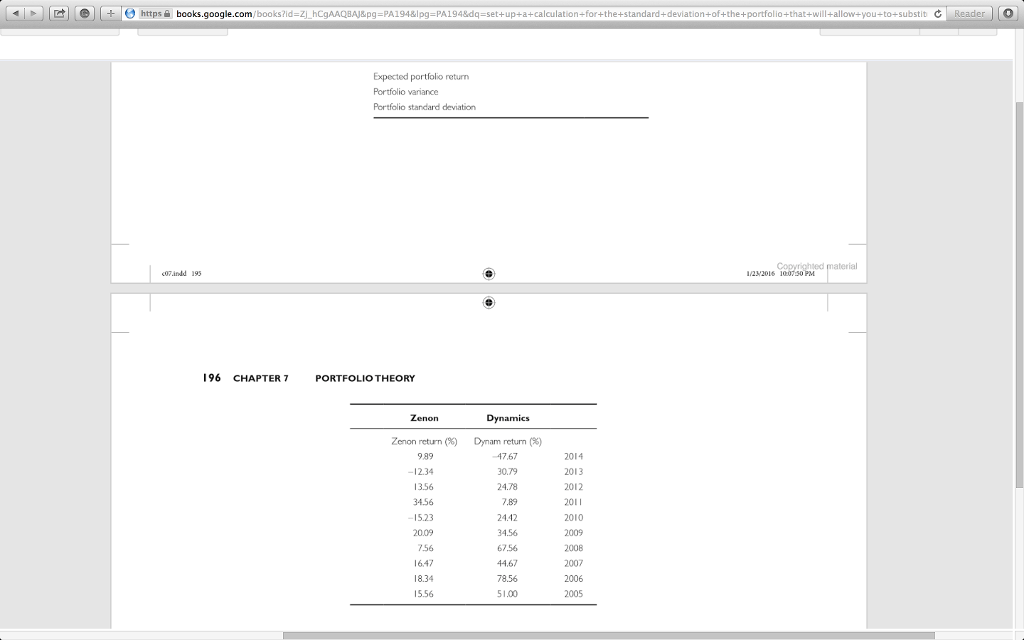

O https books.google.com z hcgAAQBAJ&pg PA194&lpg PA194&dq up at calculation for the +standard deviation--of+the+portfolio+that+w allow you to substit C Reade O 7-3 Fill in the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Adventure Finance

Authors: Aunnie Patton Power

1st Edition

3030724271, 978-3030724276